A Climbing 10-Year Treasury Yield Will Eventually Crack The Market

It will take years to wash away the fiscal and monetary excess of 2020-2022 – a period of unprecedented growth in the money supply. This period was the cherry on top of a decade-plus of Quantitative Easing which got investors hooked on cheap debt and the Fed put. Investor psychology won’t change overnight. Investors are hooked on cheap debt and sky high valuations. The bubble mentality started to deflate in 2022 in anticipation of the Fed taking the punch bowl away, which it eventually did in May 2022. However, this process of resetting valuations has been slow. Is there something on the horizon that may drive markets lower for an extended period of time? The short answer is “Yes”. That something is the 10-year Treasury yield working its way higher. I don’t see the 10-year yield magically halting at 5%. The 10-year yield will continue to climb well beyond 5%. It is easy to imagine a scenario where the Fed holds its Fed Funds rate above 5%, yet feels the need to exercise Quantitative Easing at the long-end of the curve in an effort to control the 10-year yield which underpins most U.S. economic activity. Before we get there, let’s review how we got into this inflationary, debt-funded mess.

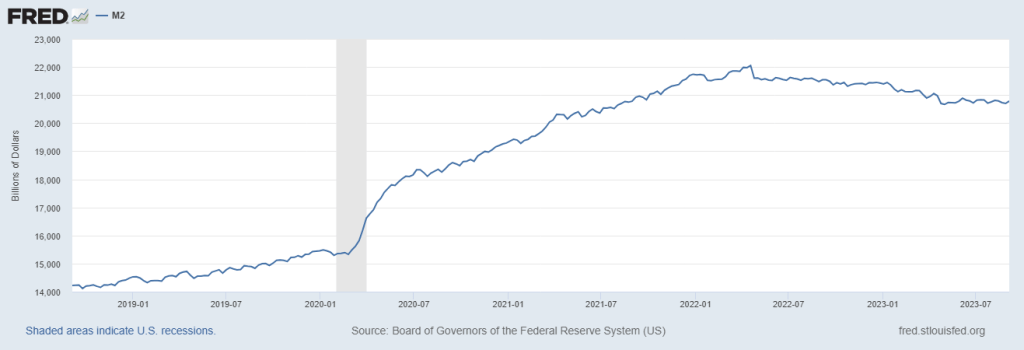

The short answer as to how we created this mess is extraordinary levels of money printing. The COVID-driven excess of 2020-2022 took the money supply as measured by M2 from $15.3 Trillion in January 2020 to $22.1 Trillion in April 2022 – a 44% increase (first chart below).

{kind=link}

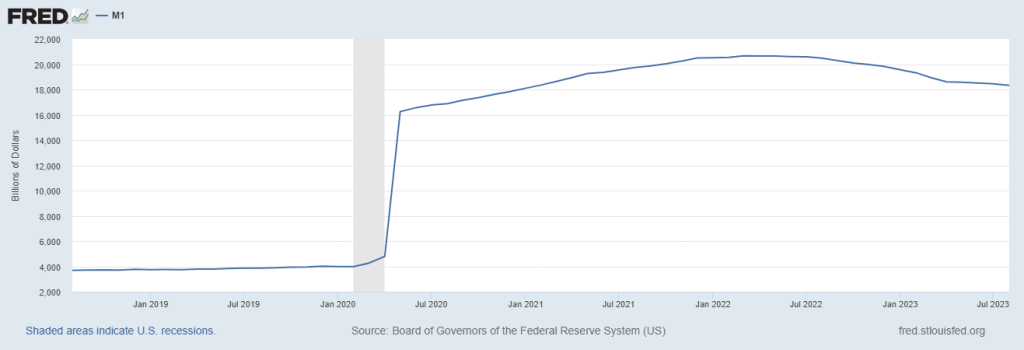

M1 – a more narrow money supply measure – grew more sharply. M1 consists primarily of currency and deposits. It grew from $4.0 Trillion in January 2020 to $20.7 Trillion at the peak in April 2022 – a 418% increase. Nothing justifies that sort of an increase. Not even war.

{kind=link}

The punchline is I do not know when the market will crack. Yet, it is a climbing 10-year yield that will do it in my view. The 10-year is going to break something. As we have written previously (most recently this week), the fact that the United States is insolvent warrants a much higher 10-year yield. Also, I don’t subscribe to the theory that past is prologue. Simply because the average spread between the 10-year yield and the Fed Funds rate has averaged 1.49% does not mean this will be the case on a go-forward basis. That spread could and should widen given that the United States’ fiscal situation is likely to deteriorate the further in the future we look out.

When something breaks, the Fed will step in to justify its existance (we would be better off without Central Bank control, simply look to the Great Depression and the Great Recession). The equity market will find a bottom after the Fed steps in. The equity market may crack off of the Q4 earnings reports despite misguided bullish talk about 2024 from delusional CEOs such as Snap’s Evan Spiegel. I don’t see how a 5%, 6%, or 7% 10-year Treasury yield is good for the Ad market or the Equity market.