AT&T: Caught Between A Rock and A Hard Place

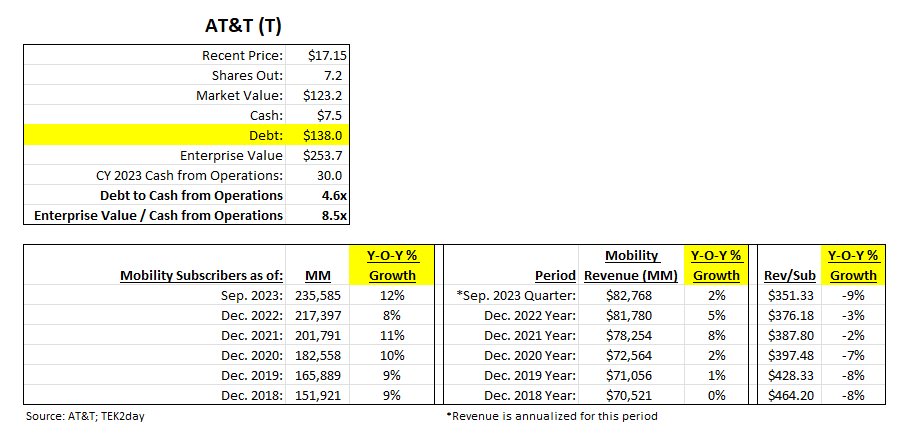

AT&T’s Debt to Cash flow ratio is 4.6x, which is not great given that AT&T operates in a capital intensive, slow growth industry with deteriorating unit economics.

AT&T’s Mobility business is the company’s bread and butter as it accounts for 68% of Total Revenue. The issue here is that Mobility subscriber growth is narrowly outpacing Mobility revenue per subscriber declines.

If Mobility revenues were to decline or if Mobility subscriber growth were to be cut in half, the risk of AT&T defaulting on its debt would immediately double in my view.