Bank Liquidity Is Rising, But at What Cost?

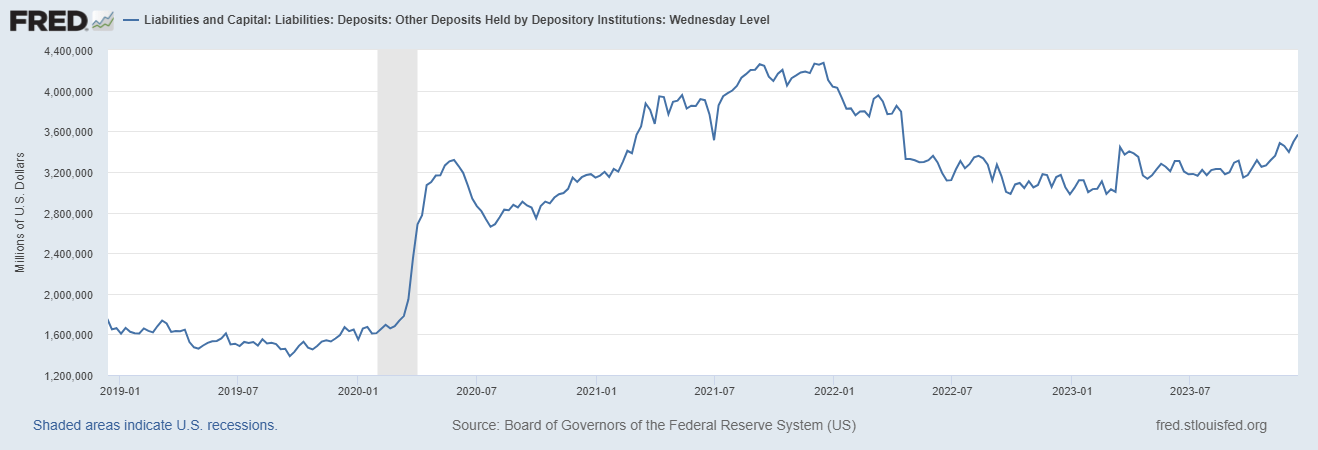

Banks have more liquidity today than they have had since April 13th 2022 as measured by Other Deposits and Liabilities (ODL). ODL is essentially M2 less retail money market funds and paper currency. ODL matters because it is the primary funding source of bank credit. While more liquidity is a positive for economic growth and financial markets, it comes with a cost.

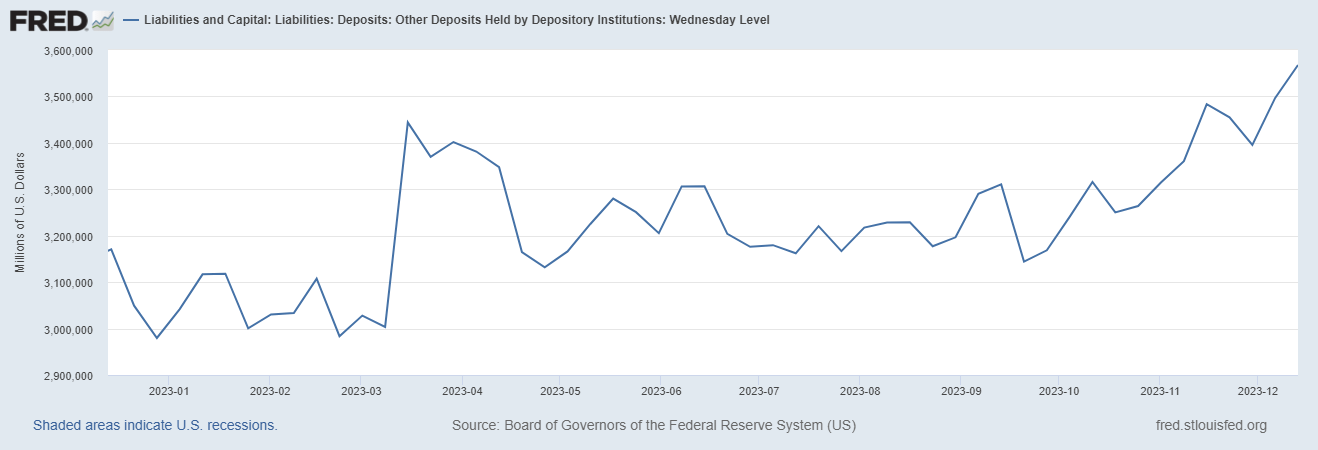

ODL peaked on December 15th 2021 and more or less flatlined from August of 2022 until November 1st 2023 when a modest uptrend began.

While more liquidity is a positive for economic growth and financial markets, it could also kickstart inflation.

Further, would ODL continue to grow if the Fed removed its Bank Term Funding Program (BTFP) bailout? I doubt it.

The spike in ODL back in March 2023 (below chart) is a function of the Fed having backstopped the banking industry with its BTFP.

The BTFP is set to expire in mid-March 2024. We fully expect the Fed to renew this program, which effectively enables banks to mismanage their business.

The U.S. economy has become too dependent on monetary and fiscal stimulus. Absent the BTFP and countless other artificial stimulus programs the U.S. economy appears to lack the internal strength to drive sustainable organic growth. This of course is a problem as artificial stimulus comes with an enormous price – Dollar devaluation.