BofA's Unrealized Losses Taper

The Fed’s dovish turn reduced Bank of America’s unrealized losses in the December quarter compared to the quarter-ended Sept. 30th 2023. Nothing like Banking CEOs having the Fed crutch to lean on. Bank of America CEO Brian Moynihan ought to be fired for allowing the bank to take such an oversized position in mortgage-backed securities when the Fed Funds rate was at the zero bound. Without the Fed’s BTFP bailout and Powell’s dovish turn in December, BofA would have suffered existential problems.

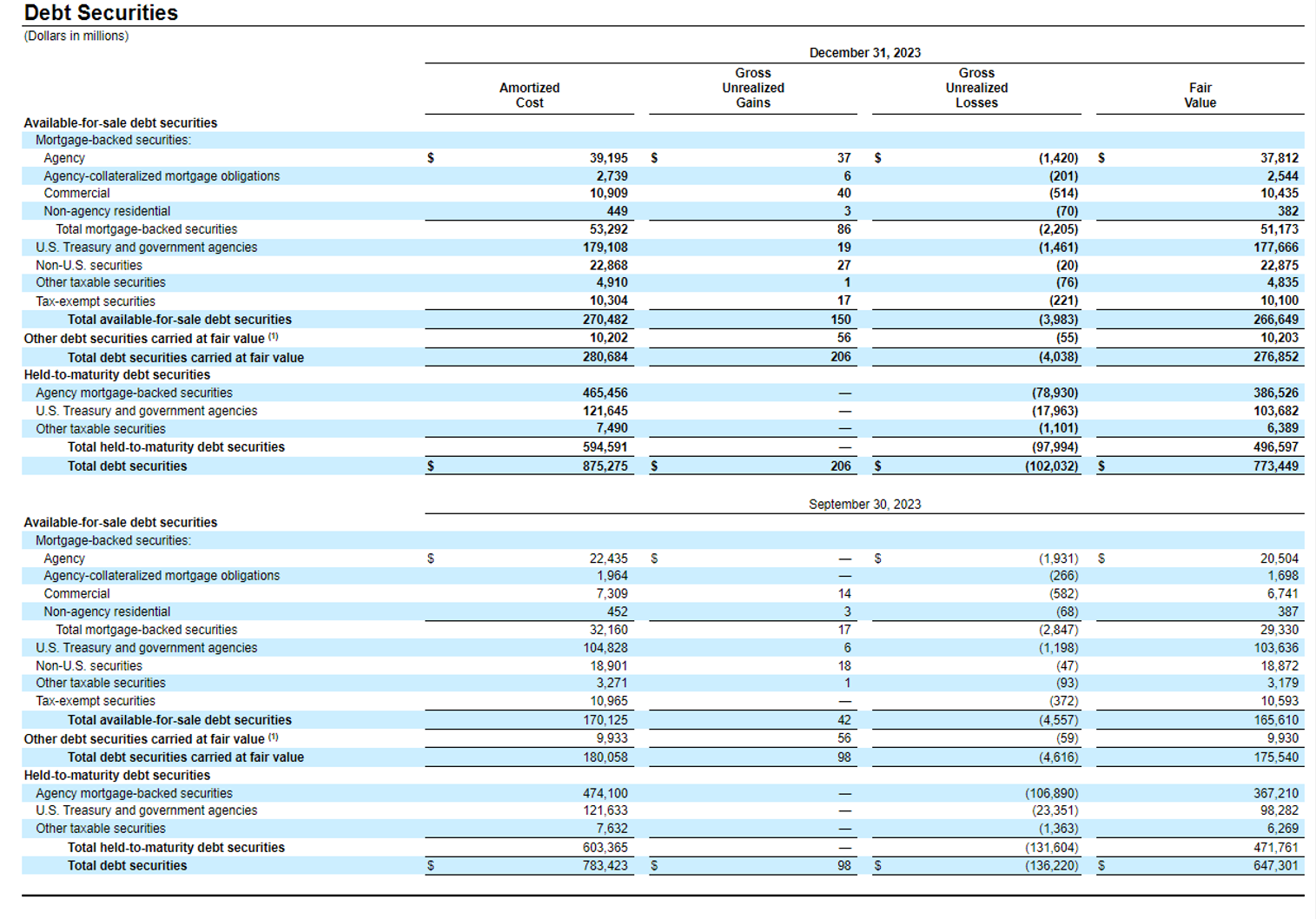

In recent weeks we called out Bank of America (BAC) for gorging on cheap debt and suffering large unrealized losses as a result ($107 billion in Gross Unrealized Losses on mortgage-backed securities as of Sept. 30th 2023 and $136 billion in total Debt security Gross Unrealized Losses).

When banks carry large losses such as these - even when unrealized - those banks typically become more conservative and pull back on lending. Well, the Fed bailed out the banks when it enabled banks to mark-up the value of their assets to par value when borrowing from the Fed’s BTFP bank bailout program.

Our view is that Fed Chair Powell took his dovish turn in December to talk down yields in order to reinflate bond values. Powell’s market manipulation worked if you are a Banking CEO with underwater debt securities on your balance sheet. For example, Bank of America’s corresponding Gross Unrealized Losses for the period ended December 30th 2023 were $79 billion and $102 billion respectively. 26% and 25% loss reductions respectively as compared to the September quarter.

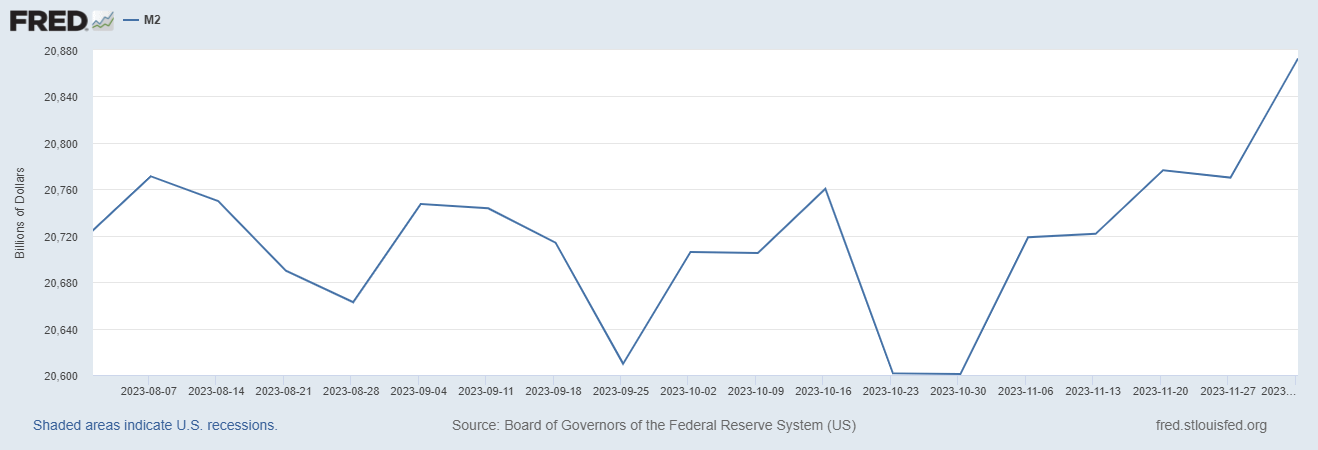

The Fed’s Centralized Planning worked in favor of Bank of America at the expense of private capital. In addition, the money supply was unnecessarily inflated (liquidity has ticked up since Oct. 30th 2023, see the below M2 chart).

Further, we now have a generation of Banking CEOs who believe they can do no wrong (At least the large banks believe they are too big to fail). To be fair, this moral hazard began with the 2008 bank bailouts and was taken to extreme levels given the fiscal and monetary responses to the unwise Covid lockdowns.

Expect more liquidity, more easing, and more soft, dovish hands from the Fed as it reinflates the U.S.’s debt-fueled economy at the expense of Americans, at the expense of the purchasing power of the U.S. Dollar.