Core CPI Remains Elevated. The Inflation Engine Will Start Up Again in 2024.

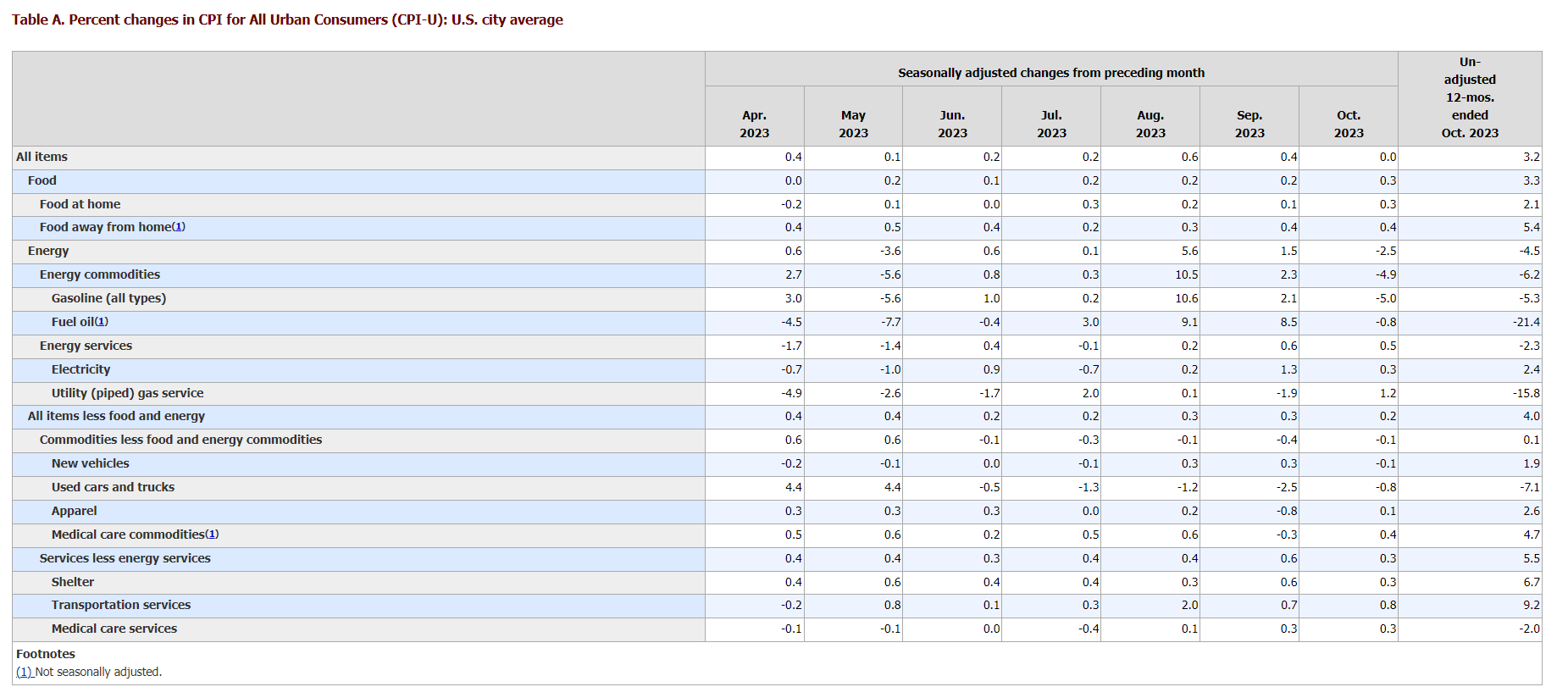

Core CPI was at 4.0% for the month of October, within our expected range. Shelter continued to climb as we predicted and therefore drove Core CPI higher. The fact that oil has drifted downward is what has headline CPI at 3.2%, despite the fact that food prices continued to climb.

The month-to-month numbers were 0.2% for Core CPI and 0.0% for headline CPI. Food was up 0.3% for the month and frankly is the category that will drive the U.S. into recession. Food prices are up far more than the story told by CPI and the fact that food price increases are moderating after two-plus years of steep price increases will do little to soften the economic blow.

I’m glad the market likes the numbers, but getting down to 2% CPI on the year-over-year headline number will prove difficult without a recession.

Let’s game theory this out. We do expect a recession. Yet, how long will Treasury and the Fed allow a recession to persist, especially in an election year? Where will another round of fiscal stimulus, low interest rates and QE take CPI? The Fed unfortunately has backed itself into a corner after having conditioned the market to easy money from 2009-2022. Further, I don’t see a way to pay back Treasury’s $34 Trillion debt bomb without inflating the debt away. Thus, this inflation reprieve will prove only temporary.