Cross Company Transcript Analysis

We are a little late in running these transcripts through Kilby for analysis. Here’s the cross-company analysis of the Q1 2026 earnings calls for Alphabet (GOOGL), Meta (META), and Microsoft (MSFT), where we identify common threads and more…

Common Threads Across All Three

1. AI CapEx Arms Race — Accelerating, Not Plateauing

All three raised or reaffirmed massive capital expenditure plans and signaled that 2027 will step up further:

Alphabet raised 2026 CapEx guidance to $180–190B (from $175–185B) and said 2027 CapEx will “significantly increase” beyond 2026 (Alphabet transcript, p. 13). Q1 CapEx was $35.7B, overwhelmingly in technical infrastructure.

Meta raised 2026 CapEx guidance to $125–145B (from $115–135B), driven by higher component costs, especially memory pricing (Meta transcript, p. 8). Susan Li noted they have “continued to underestimate our compute needs” (Meta transcript, p. 11).

Microsoft spent $31.9B in Q3 alone, roughly two-thirds on short-lived assets like GPUs/CPUs (MSFT transcript, Amy Hood section). Satya framed getting CapEx deployed in time for usage growth as the critical constraint.

The common signal: all three are compute-constrained right now, demand exceeds supply, and they are all racing to build out capacity before the other gets there first. Nobody is pulling back.

2. Agentic AI Is the Shared Strategic Vision

Every company positioned agents — not chatbots, not copilots — as the next product paradigm:

Alphabet launched the Gemini Enterprise Agent Platform, introduced “Antigravity” internal agentic workflows, shipped agentic commerce (restaurant booking, UCP-based checkout in AI Mode), and is pushing agentic coding (Alphabet transcript, pp. 3–5). Pichai called agentic workflows in consumer Search “a huge opportunity ahead” (p. 14).

Meta framed its entire product roadmap around “personal agents” and “business agents.” Zuckerberg: the goal is to “deliver agents that can understand your goals and then work day and night to help you achieve them” (Meta transcript, p. 2). Business AIs on WhatsApp grew from 1M to 10M weekly conversations in one quarter (p. 7).

Microsoft described Copilot evolving from chat to Edit Mode to Cowork (delegated agent tasks). Nadella framed the progression as Chat → Agents → Delegated Cowork, and said Copilot usage is now at “the same level as Outlook” (MSFT transcript, chunk_048).

The common bet: agents as the consumption vehicle for next-gen AI compute. All three see this as the bridge from chatbot novelty to durable, monetizable workflows.

3. AI Is Reinventing the Advertising Stack

All three are deploying LLMs into their ad systems to improve targeting, creative, and conversion:

Alphabet deployed Gemini across its entire ads infrastructure, launched AI Max (out of beta), and noted 30%+ of Search ad spend now uses AI-enabled campaigns. Ads relevance improved ~10% in Maps via Gemini (Alphabet transcript, pp. 7–8).

Meta introduced the Adaptive Ranking Model (LLM-scale, trillion-parameter inference for ad serving), drove 6%+ conversion rate improvements via Lattice/GEM enhancements, and reported 8M+ advertisers using gen AI creative tools (Meta transcript, pp. 6–7).

Microsoft highlighted LinkedIn as the leading B2B advertising channel and is deploying AI across Bing and Edge to drive commercial intent (MSFT transcript, chunk_014).

The implication: AI ad improvements are delivering measurable ROI, which is what funds the CapEx cycle. This is the flywheel — better models → better ads → more revenue → more CapEx.

4. Depreciation and Infrastructure Costs Are the Shared P&L Headwind

All three flagged rising depreciation and data center operating costs as pressures that partially offset operating leverage:

Alphabet CFO Ashkenazi: “the significant increase in our investments in technical infrastructure will continue to put pressure on the P&L in the form of higher depreciation expense and related data center operations costs, such as energy” (p. 13).

Meta CFO Li noted total expenses up 35% YoY, driven mainly by infrastructure costs (higher depreciation, data center ops, third-party cloud spend) and AI talent compensation (p. 4).

Microsoft CFO Hood guided Q4 COGS growth of 22–23%, with infrastructure build being the primary driver.

Despite these headwinds, all three expanded or maintained operating margins — suggesting top-line growth is outrunning the cost base for now.

5. Custom Silicon and Supply Chain Diversification

All three are investing in their own chips to reduce reliance on NVIDIA and control the cost curve:

Alphabet introduced 8th-gen TPUs (TPU 8t for training, TPU 8i for inference) and will begin selling TPUs to third-party customers in their own data centers (p. 2, 6).

Meta is rolling out 1GW+ of custom silicon developed with Broadcom, plus AMD chips, alongside NVIDIA systems. Zuckerberg called compute efficiency a “strategic advantage over time” (p. 2).

Microsoft noted ~2/3 of CapEx going to GPUs/CPUs, and the Copilot infrastructure is optimized to route between model sizes based on task complexity — the software-level analog of silicon diversification.

This is worth watching from a NVDA perspective — all three hyperscalers are clearly hedging their NVIDIA dependency.

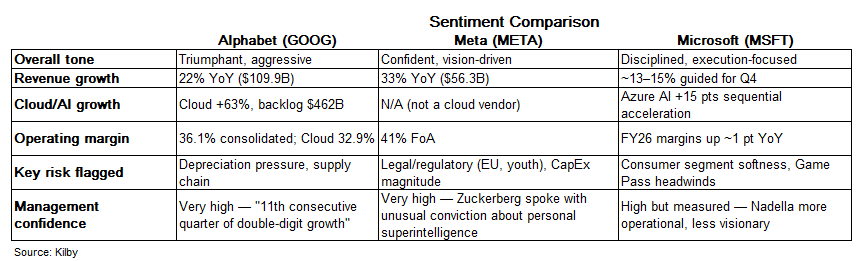

Meta’s tone was the most distinctive. Zuckerberg spent significant time on philosophy — AI empowering individuals vs. replacing them, personal superintelligence for billions, not just productivity tools for developers. This reads as a deliberate differentiation from the rest of the industry’s enterprise/coding framing.

Alphabet was the most data-rich: specific metrics everywhere (16B tokens/minute, 800% AI solution growth, 500M+ open model downloads, $462B backlog). Pichai was clearly in victory-lap mode.

Microsoft was the most operationally precise. Hood provided granular guidance and margin commentary. Nadella focused on structural positioning in knowledge work and coding TAMs rather than grand vision.

---

Macro Elements

FX tailwinds were explicitly called out by all three. Alphabet saw a 3-point tailwind in Q1, guiding to ~1 point in Q2. Meta noted ~2% FX tailwind in Q2 guidance. This means constant-currency growth rates are materially lower than reported, and the tailwind is fading.

Supply chain inflation is real. Meta explicitly cited memory pricing as the primary driver of their CapEx raise. Alphabet acknowledged a “complicated supply chain environment” (p. 23). This filters through to NVDA, AVGO, AMAT, and AMD — all of which sit in your watchlist.

Macro advertising resilience — Meta cited “better macro conditions versus Q1 of last year” as a contributor to 12% price-per-ad growth (p. 4). Alphabet’s Retail, Finance, and Health verticals led Search growth. Neither company flagged demand softness in the advertising market, though Meta’s Q2 guide ($58–61B) embeds “a range of macro outcomes” per Susan Li.

Labor force restructuring — Meta announced it plans to reduce headcount in May. Alphabet ended Q1 with lower headcount growth but is hiring in AI/Cloud. Microsoft announced a voluntary retirement program (~$900M in one-time costs). All three are optimizing headcount while pouring capital into infrastructure — the operating leverage playbook of replacing human labor cost with token cost.

No tariff or trade disruption signals appeared prominently in any of the three calls, which is notable given the current environment. This could reflect the relative insulation of digital advertising and cloud from physical trade flows, or it could mean management is choosing not to emphasize it.

---

Net Assessment for the Portfolio

The three transcripts tell a consistent story: the AI infrastructure cycle is accelerating, not decelerating. Demand is outrunning supply. Agents are the next product layer. Ad monetization is working. Margins are holding despite massive cost increases.

The risk to watch: if advertising demand softens in H2 2026 while infrastructure costs keep climbing, the margin story breaks. Right now, all three are growing revenue fast enough to absorb the depreciation hit. That’s the key variable to monitor across the next two quarters.