CSGP: What Are Investors Looking At?

CSGP shares are up on yesterday’s EPS report, but…

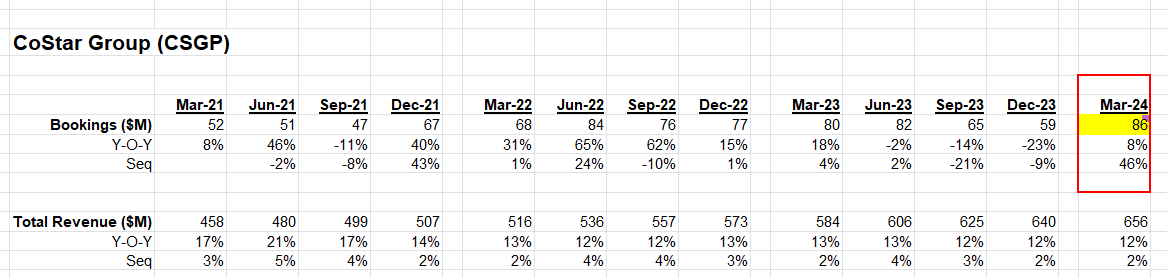

Organic Bookings down: CSGP monetized Homes.com in the quarter. If you strip out Homes.com bookings of $39 million, organic bookings would only be $47 million, down -41% year-over-year and down -20% sequentially. Business is slowing folks!

More Sales & Marketing investment required to generate bookings. CSGP spent $2.83 on Sales & Marketing to generate $1 of bookings in the March 2023 quarter versus $4.26 in the March 2024 quarter (I included the full bookings figure of $86 million for the March 2024 quarter Sales & Marketing/Bookings ratio calculation).

Cash flow is not great, shares are expensive. CSGP is stretching Payables. If you were to strip out the $77 million Payables benefit in the March 2024 quarter, CSGP would have generated Operating Cash of approximately $60 million versus the $140 million reported figure. Let’s give CSGP the benefit and use the $140 million figure, which implies an OCF run rate of $560 million, which values CSGP’s equity at 66x cash flow. Cash flow will probably finish the year at around $500 million, which implies an equity multiple on cash flow of 74x. Anything but cheap.