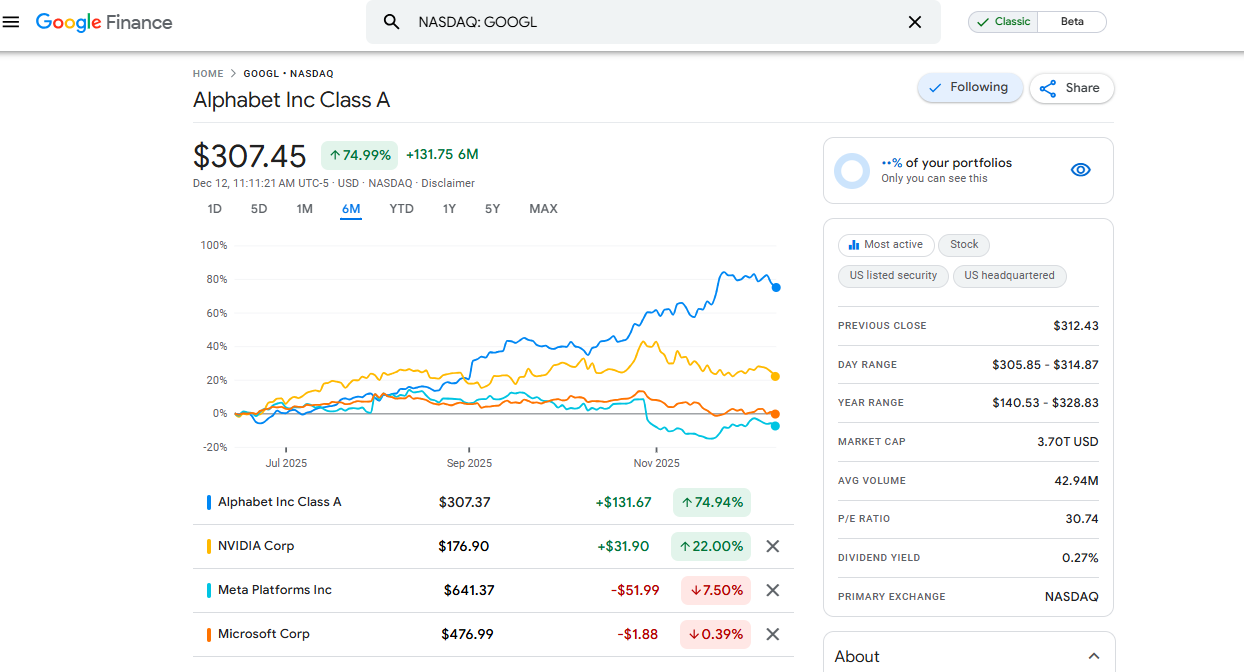

Do META and MSFT Reflect Adequate Downside Risk?

Interesting chart directionally. GOOGL, NVDA, META and MSFT have behaved as one would expect. MSFT and META both still feel expensive in that neither seems to reflect downside risk.

Microsoft (MSFT): Microsoft offers GPUs in the cloud at scale. OK. So does GOOGL, AMZN, and ORCL. MSFT lacks Gen AI intellectual property. Partnering with OpenAI does not justify the run MSFT shares have had over the past three years. OpenAI is clearly pushing for an IPO before the masses figure out it does not stand a chance long-term. LLMs are a scale game and OpenAI lacks scale. I’m referring to size of balance sheet. OpenAI will not be able to maintain the pace of capital investment so long as Google and xAI continue to push the AI infrastructure investment pedal to the metal.

Meta Platforms (META): Zuckerberg is bored with the core business and is therefore chasing shiny new objects. I give META a zero percent chance of building the world’s finest frontier LLM. META needs to acquire Anthropic or OpenAI in order to challenge Google Gemini. MSFT won’t allow an OpenAI sale to META. That means META needs to acquire Anthropic. The funny thing is, I was a fan of Zuckerberg building a fleet of opensource LLMs and SLMs. I guess that strategy did not stroke his ego.