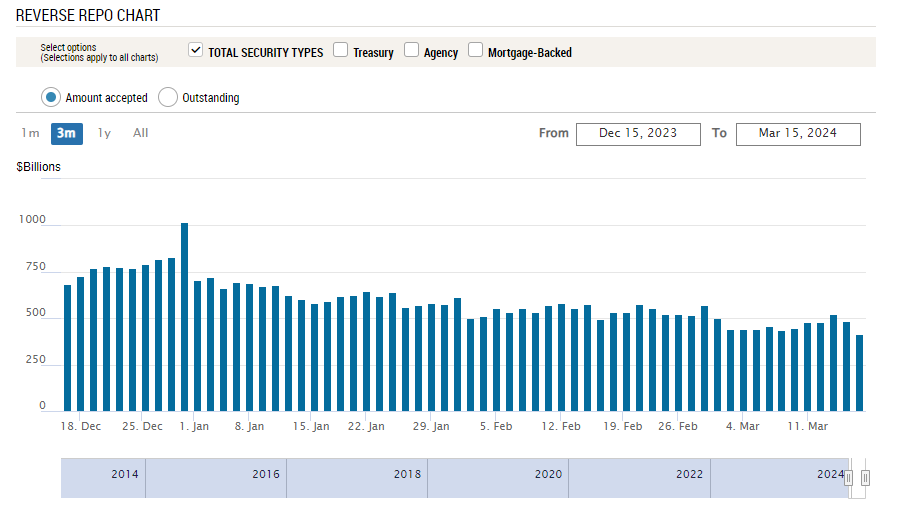

Excess Liquidity Continues To Drain from the System

Using the overnight reverse repo market as a proxy for excess liquidity, excess liquidity continues to be removed from the system. I believe that the Fed will end its QT program sometime between now and when reverse repo levels fall to zero. Reverse repo levels are currently the lowest they have been since June 2021.

I don’t believe that this Fed is willing to do what is necessary to get Core CPI back down to 2% and that 3% will magically become the Fed’s new target sometime this year.

The 10-year Treasury yield continues to remain at around 4.3%, which is problematic for the big banks as elevated yields cause large unrealized losses on the investment securities the large banks purchased when rates were at zero. This will cause many banks to become cautious in their lending practices (as it did in March 2023) once BTFP borrowings are extended as loans leaving banks with less cash on hand with which to face a prospective rush of withdrawals. Depositors may move bank deposits to money market instruments given the elevated interest rate environment.

Between the high debt levels ($34.4 Trillion), and associated interest service expense combined with bank weakness, the Fed has no choice but to take rates back down to around 1% sometime this year or next.