Fed Discount Window Weekly Update

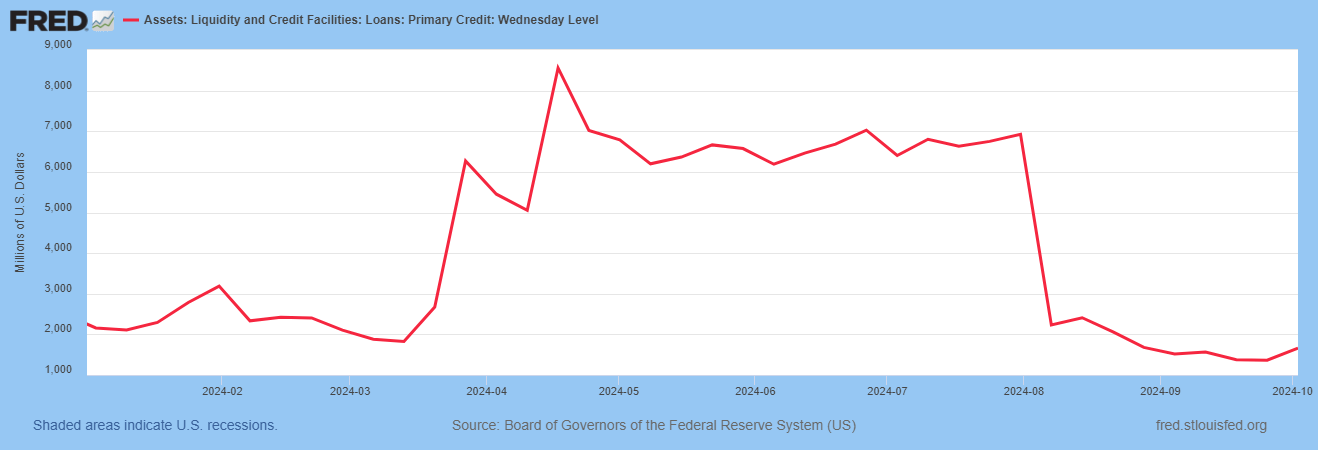

This week’s Primary Credit activity at the Fed’s Discount Window:

This week’s primary credit balance was $1.7 billion, up from $1.4 billion a week ago. I do not expect the primary credit measure to spike higher unless the Fed truly maintains elevated rates for an extended period of time. I do not believe that the U.S. economy is as healthy as the financial houses would have us believe. I do believe the Fed will lower rates. I do believe that prices will remain elevated as economic activity further slows in real terms. We have a name for this phenomenon. I wrote a book about it.

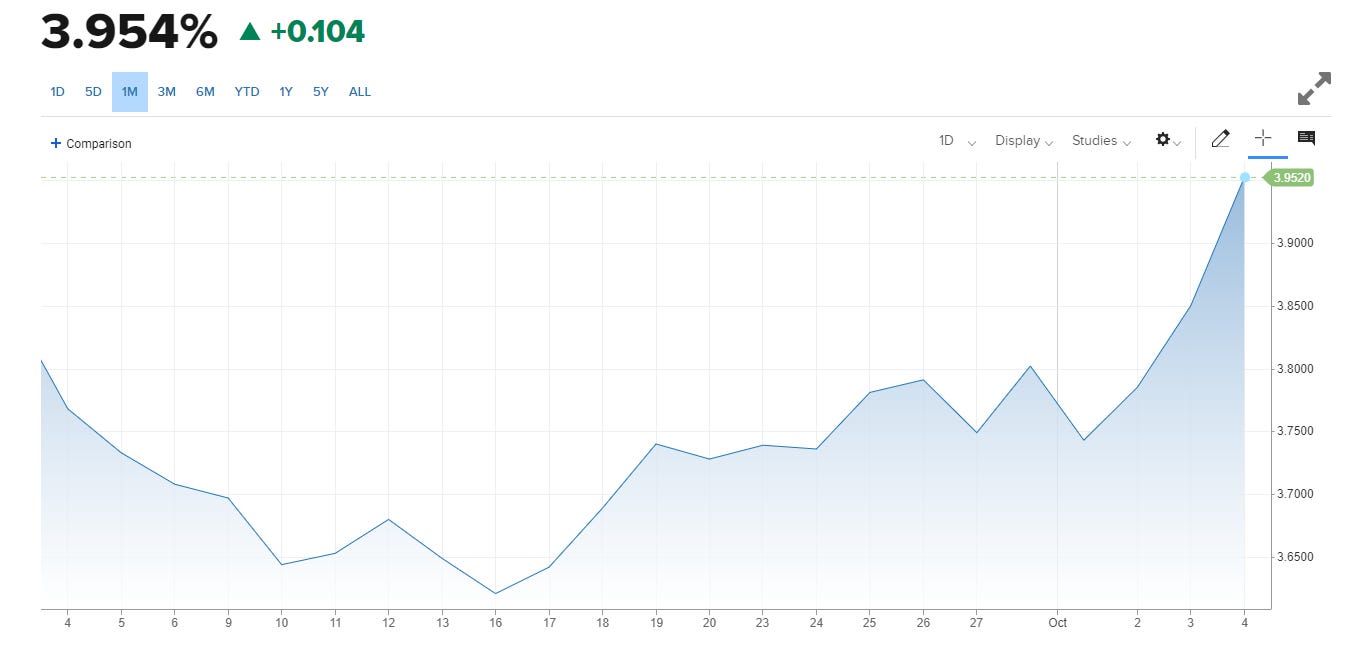

In the meantime, the Treasury market is correcting for the Fed’s inflationary behavior. A hot CPI print on October 10th could easily push the 10-year Treasury yield north of 4%. The question is, will we see a 5% 10-year Treasury yield in Q1 2025? It is possible, especially if fiscal and monetary policies remain inflationary.