Fed Discount Window Weekly Update

This week’s Primary Credit activity at the Fed’s Discount Window:

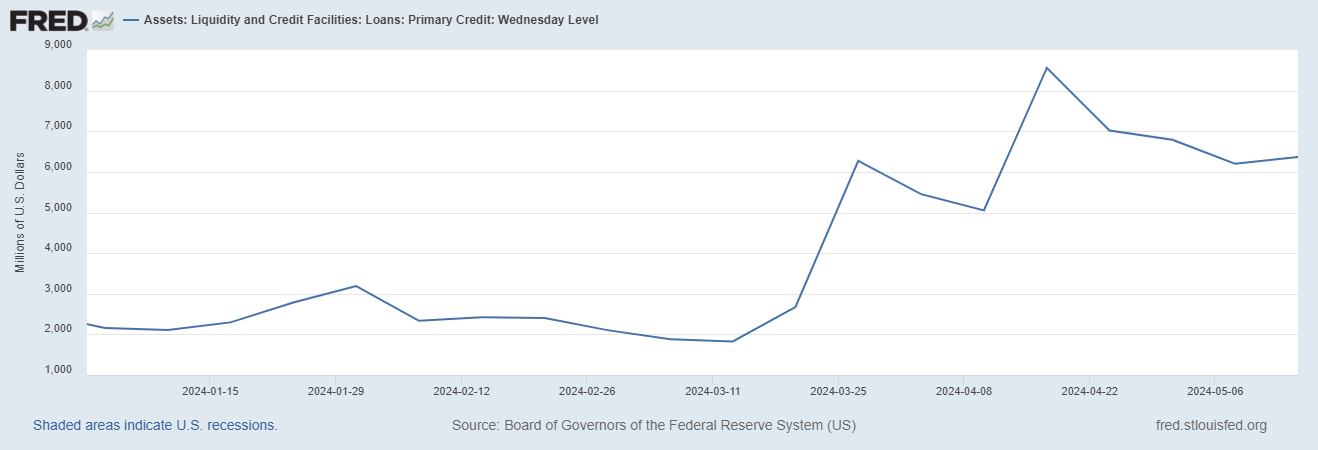

This week’s primary credit balance was $6.4 billion, up slightly from $6.2 billion the week prior.

Bank unrealized losses will remain elevated so long as rates remain elevated and/or until those underwater investments move from the “unrealized” category to the “realized” category.

I expect more small and regional bank failures, but it is clear that the Fed and the FDIC won’t allow any of the Big 4 to fail. BTFP 2.0 will be rushed to market before a large bank failure occurs. Welcome to the nanny state where CEOs and corporations are routinely bailed out.

How much longer will the Fed keep rates elevated? The Fed has eased since Powell’s comments on December 13th. I believe if unemployment gets into the 4’s and/or if we see CRE failures spill into the banking sector the Fed will cave and send rates back close to zero. The U.S. has $35 Trillion in Treasury Debt outstanding. Powell will be removed before rates are allowed to remain elevated over the long-term. Fiscal spending matters most to those in Washington, not price inflation. Only a market-driven spike in the 10-year Treasury yield can force the Federal Government to dramatically slow spending. That day is not here, yet.

Eventually, the Fed will move its CPI target to 3% or abandon the thought of a target.

The Fed is an enabler of bad fiscal policy and puts forth bad monetary policy. The Fed isn’t your friend, nor is Treasury, nor is Congress, nor is the Executive Branch. Unfortunately, all of those branches of Government are the spicket that controls the flow of liquidity into markets. These days (since 2020), that spicket dominates markets, much more so than fundamentals. What free market capitalist system? Show it to me.

Federal Reserve Balance Sheet: Factors Affecting Reserve Balances - H.4.1: https://www.federalreserve.gov/releases/h41/current/