Fed Funds Back To 0% To Ease The $35 Trillion Debt Burden

The Fed will not admit it, but the United States’ $35 trillion debt burden is a significant reason why the Fed is lowering its Fed Funds Rate.

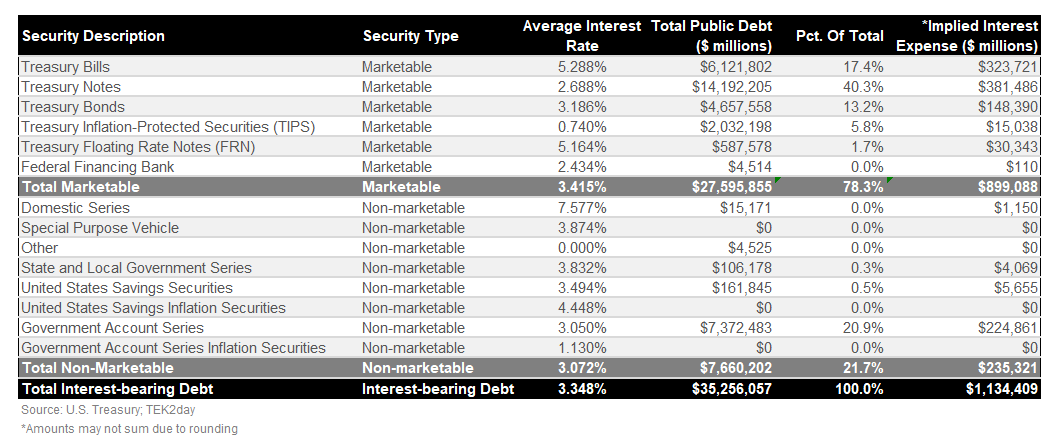

The Fed can control the front-end of the yield curve (and therefore interest expense payable) by manipulating its Fed Funds rate. T-Bills are at the short-end of the curve at an average interest rate of 5.3%, which translates to $324 billion of interest expense (total U.S. interest expense is approximately $1.1 trillion). The Fed can reduce the interest expense burden on T-Bills by lowering Fed Funds. As T-Bills expire and are replaced with new issues, those issues will carry a yield below the current 5.3% blended average.

Treasury can’t afford to have annual interest expense in excess of $1 trillion when the Federal Government is running fiscal deficits of $2-3 trillion each year.

The Federal Government could radically reduce its spending, but Congress and the Executive Branch will not curb spending. Instead, Congress will continue to run massive fiscal deficits and look to the Fed to ease the interest expense burden by lowering its Fed Funds rate and potentially re-engaging in Quantitative Easing (QE).

When would the Fed engage in QE? The Fed would engage in QE to exercise yield curve control on the portion of the yield curve outside of the front-end. Let’s say for example that 10-year Treasury yields remain stubbornly high as the Fed lowers its Fed Funds rate. If that is the case, I would expect the Fed to engage in a new round of QE. That is to say the Fed will actively buy 10-year Treasuries in the open market which will drive 10-year prices higher and yields lower. Treasury Notes (1-10 year maturity) carry a blended average interest rate of 2.7% with implied interest expense of $381 billion.

The Fed has every incentive to take Fed Funds back to zero percent given the United States’ $35 trillion debt burden.