Fiscal Policy Should Matter To Investors & Everyone Who Has A Vote

My experience is that equity investors pay little attention to fiscal policy and that fixed income investors similarly pay little attention (the latter cohort prefers to focus on monetary policy and corporate cash flows). This will change as fiscal policy dominates the Fed’s monetary policy and drives the U.S. economy, almost always for worse.

It should have been clear after the 2008-2009 bailouts that fiscal policy drives both monetary policy and the broader economy. If the Great Recession did not make it clear, the more recent period beginning with the 2020 fiscal response to COVID ought to have made it abundantly clear that fiscal policy drives both the U.S. economy and monetary policy.

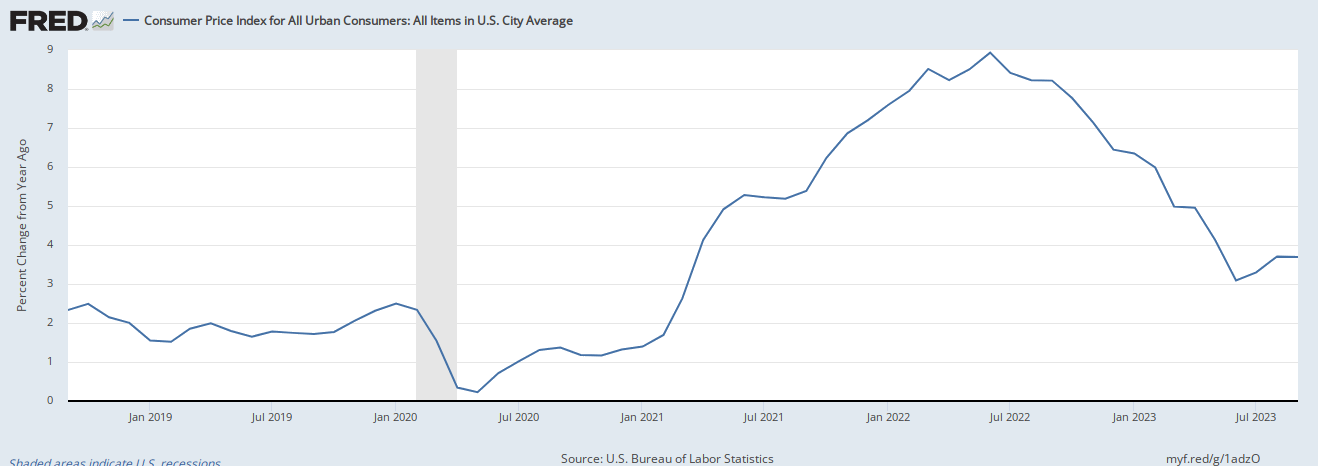

The reckless spending levels by the Trump and Biden Administrations are the reason why we have had two-plus years of massive inflation and sharp growth in the Treasury Debt.

{kind=link}

Click HERE to view expanded CPI chart.

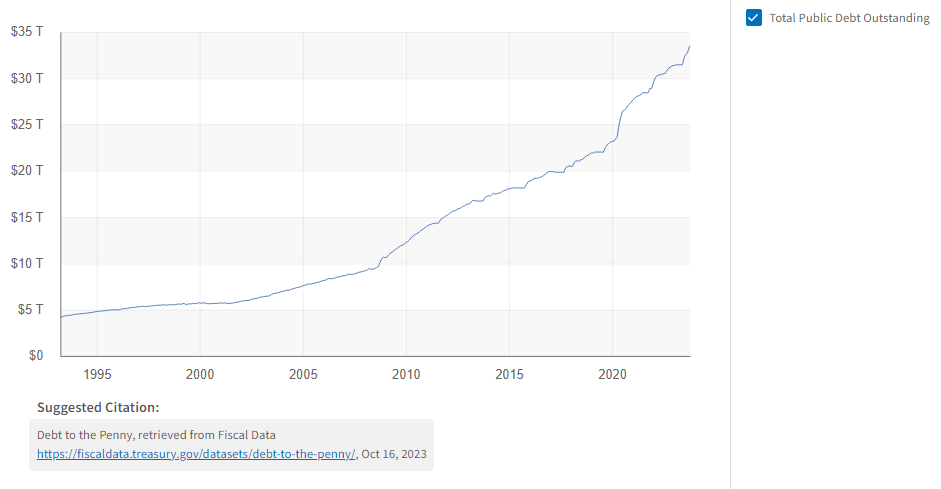

Treasury Debt is piling up ($33.5 Trillion as of October 12th) and will continue to pile up. Treasury Debt will reach $40 Trillion by 2026 at this rate.

Is it any wonder that the 10-year Treasury yield is bumping up against 5%? If I were to buy the 10-year, I would want to be compensated a heck of a lot more than 5% knowing that the United States is technically insolvent.

Let’s get real, the U.S. Treasury must issue new debt in order to raise cash to pay down its outstanding debt. That is not an enviable position. The U.S. Government does not have the cash on hand to pay its bills. The fiscal deficit is $1.52 Trillion through the end of August (the fiscal year ends September 30th). My guess is that when the final figures for fiscal 2023 are tallied, the 2023 fiscal deficit will approach $2 trillion.

To date, the 2023 fiscal deficit is 61% higher than the same period a year ago ($946 billion deficit in the year-ago period). The fiscal deficit is only likely to grow once this new Congressional Budget deal gets done later this year. The Continuing Resolution that was passed earlier this month expires November 18th. I promise you this next budget deal will be enormous. I can promise you it will generate another multi-trillion Dollar fiscal deficit which will require that we print money to fill the budget hole, thereby growing the Treasury Debt well beyond $33.5 Trillion.

Treasury Debt and Fiscal Deficits are far outpacing GDP growth and Government Tax Receipts. Therefore, the U.S. Government is technically insolvent.

Given the above, who in their right mind would want to own 10 year, 20 year or 30 year Treasuries? How is a 4.7% yield anything close to appropriate for the 10-year Treasury yield knowing that the Treasury Department will have to issue new debt just to pay down the old?

Who will buy the Treasury’s paper? The answer is that the Fed will buy some of it. I don’t see how we won’t find ourselves back in a Quantitative Easing (QE) environment. QE was a slippery slope when the U.S. went down that path in 2009. At that time the Fed positioned QE as a one-off. QE was anything but a one-off as Americans had to suffer the consequences of that awful policy through 2022 which of course contributed to the Dollar’s reduced purchasing power (i.e. inflation), over that period. As the saying goes: “There is nothing more permanent than a temporary Government program”.

There is a simple solution of course to this fiscal mess. Those in Congress could simply spend less. However, they will not. They will continue to borrow from future generations in pursuit of short-term self interests. Both Congress and the Oval Office are bought and paid for, controlled by Corporate Interests in servitude of their own.