Gold Prices Will Move Higher as The Dollar's Purchasing Power Erodes

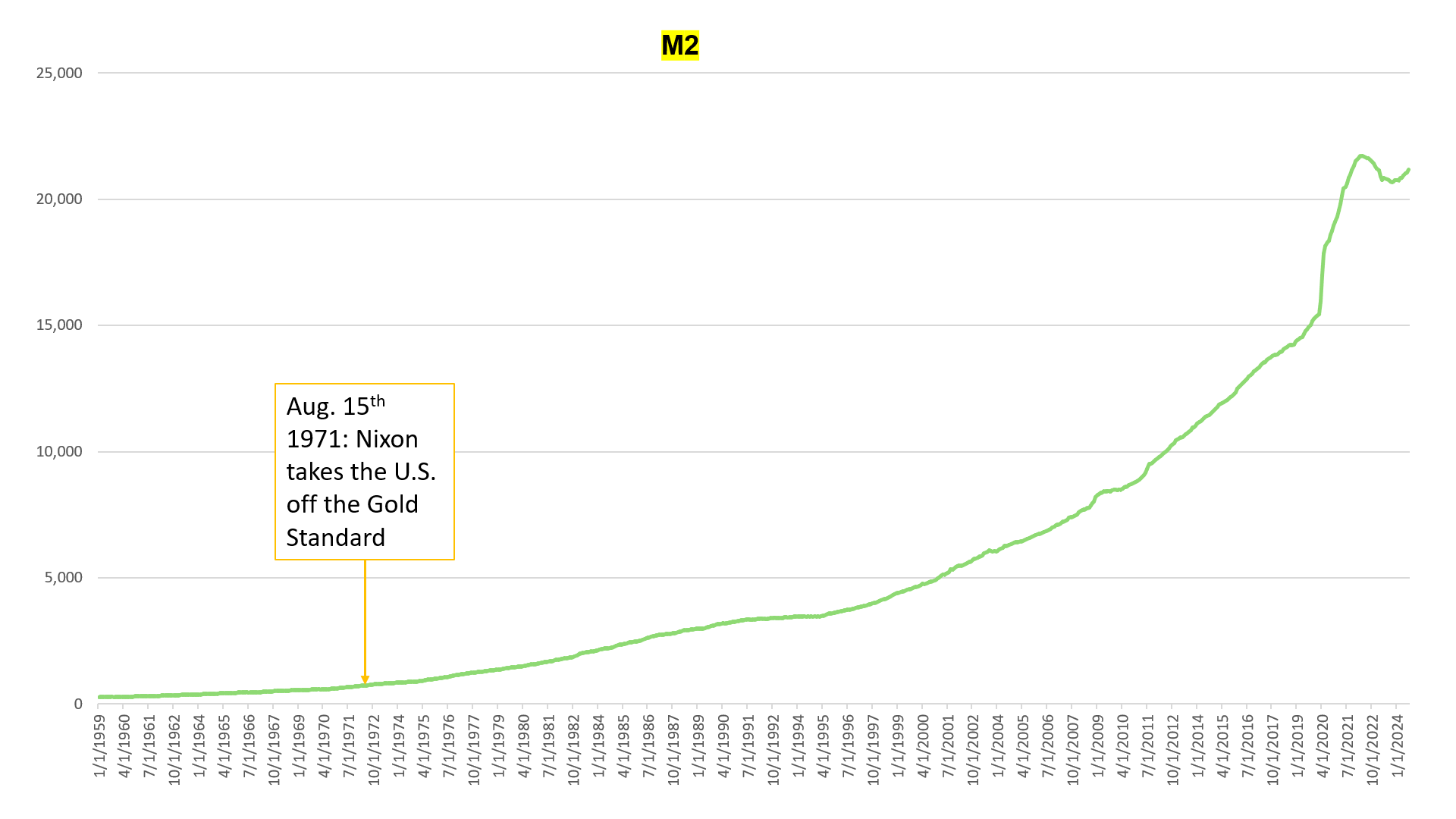

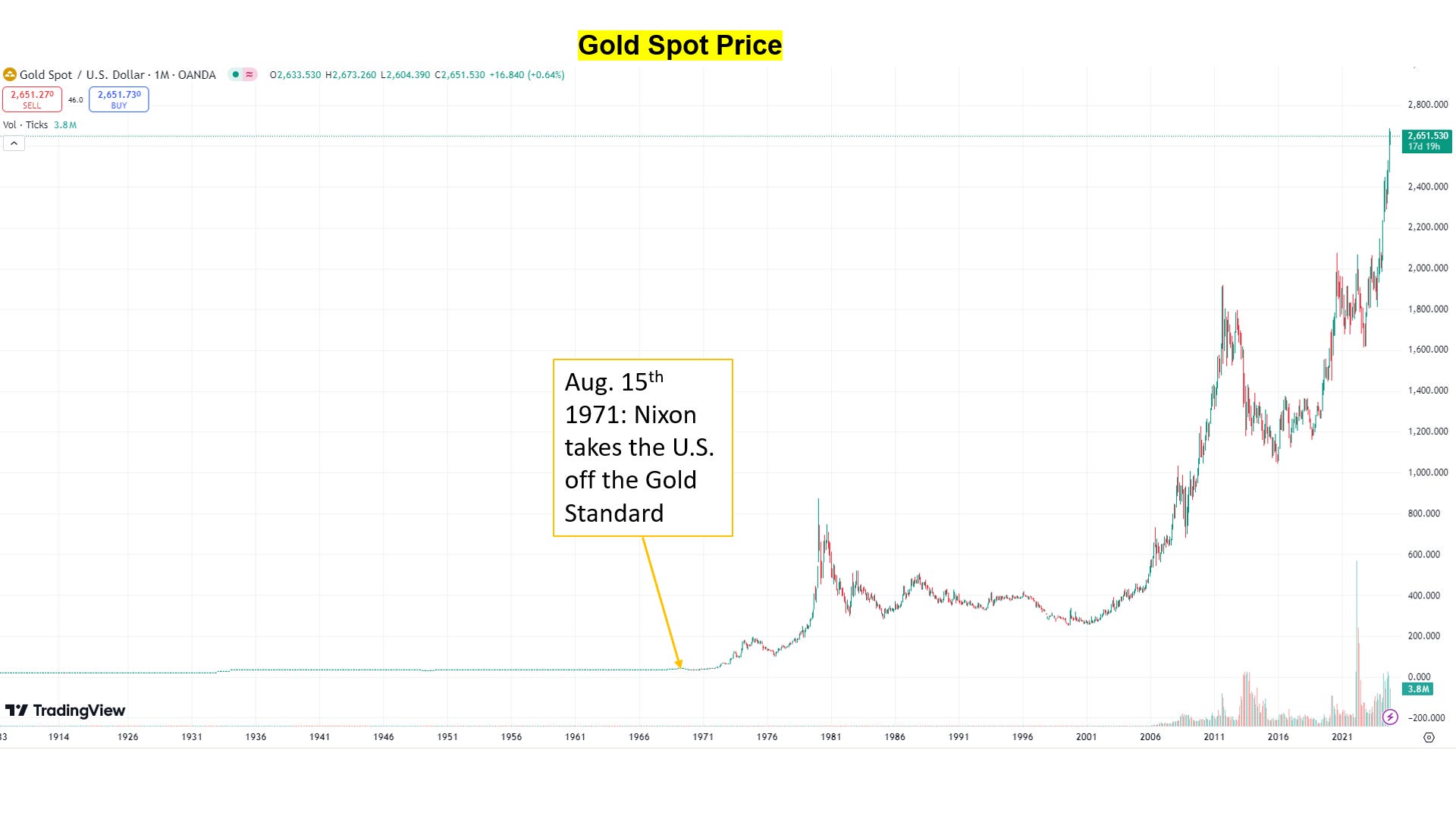

Once then President Nixon took the U.S. Dollar off the Gold Standard on August 15th 1971, the Federal Government was unshackled from the discipline of not being able to inflate its fiat currency (the Dollar), beyond its gold reserves. Since that time, the Dollar’s purchasing power has been crushed, losing 98% of its value versus Gold. The Dollar’s purchasing power will continue to erode so long as Government continues to grow the money supply faster than productivity growth. Deficit spending = M2 growth = Gold price appreciation.

Since that date, the money supply as measured by M2 has grown 30x and the price of gold has grown 64x. Put another way, M2 has suffered 96% dilution since August 1971 and the Dollar has lost 98% of its value versus gold over the same period.

The price of a Chevy pickup was $3,500 in 1971 and is $40,000 today (I am being generous with today’s price), which is to say that the Dollar has lost 91% of its value in this example.

Chocolate bars cost 10 cents in the 1970s and a comparable chocolate bar - if you can call it chocolate, (I am not sure what crap constitutes a chocolate bar today) - costs $1.50, meaning the Dollar took a 93% hit in the chocolate example.

The average home price in 1971 was $28,300, today it is $280,000 (a 90% hit to the Dollar).

It does not have to be this way. Policy decisions made by Washington D.C. and Central Bankers have led to the Dollar’s steep erosion.

Who pays the price? Holders of U.S. Dollars pay the price in the form of the Dollar’s eroded purchasing power.

Gold seems to be a safe bet so long as the fiscal and monetary policy of the past 50-plus years remains the status quo.

Treasury investors are challenging the status quo. Treasury investors are demanding a higher yield to own 10-year Treasuries. Yields could move much higher if the United States kicks off another massive printing cycle and if countries such as China and Japan continue to shun U.S. Treasuries, thereby forcing the Fed and private investors to pick up the slack. A 7-10% yield on the 10-year within the next 10 years is not unthinkable. This would grind fiscal spending to a halt. It is easy to imagine equity valuations compressing by 60-80% were this scenario to occur.

In the meantime, taxes will go higher in 2025/26 under Trump or Harris. Higher tax rates - whether on people, companies, or both - will force valuation multiples lower.