Google's 32x FCF Multiple Needs A Haircut

Google’s valuation does not reflect the company’s modest free cash flow growth, nor the competitive risk from less expensive open source models.

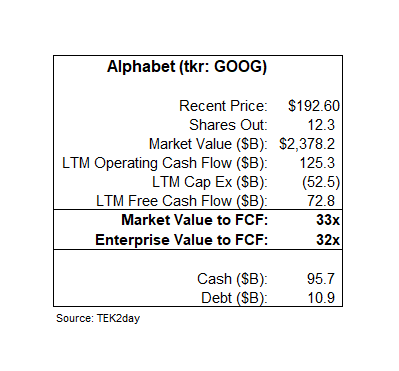

Why does GOOG 0.00%↑ deserve a 32-33x free cash flow multiple when free cash flow only grew 5% in 2024 and will likely grow by a similar amount in 2025?

Cap Ex growth is outpacing Operating Cash Flow growth as Google invests in AI infrastructure, primarily for its proprietary models. However, those proprietary models (and those of OpenAI and Anthropic and others) are under attack from open source AI model builders such as DeepSeek and META 0.00%↑.

Google’s free cash flow multiple ought to better reflect its free cash flow growth rate, and since Google has hitched itself to the frontier model wagon, that multiple ought to reflect the open source competitive risk.