High Yield Credit Spreads Are Too Narrow

Spreads do not accurately reflect high yield credit risk

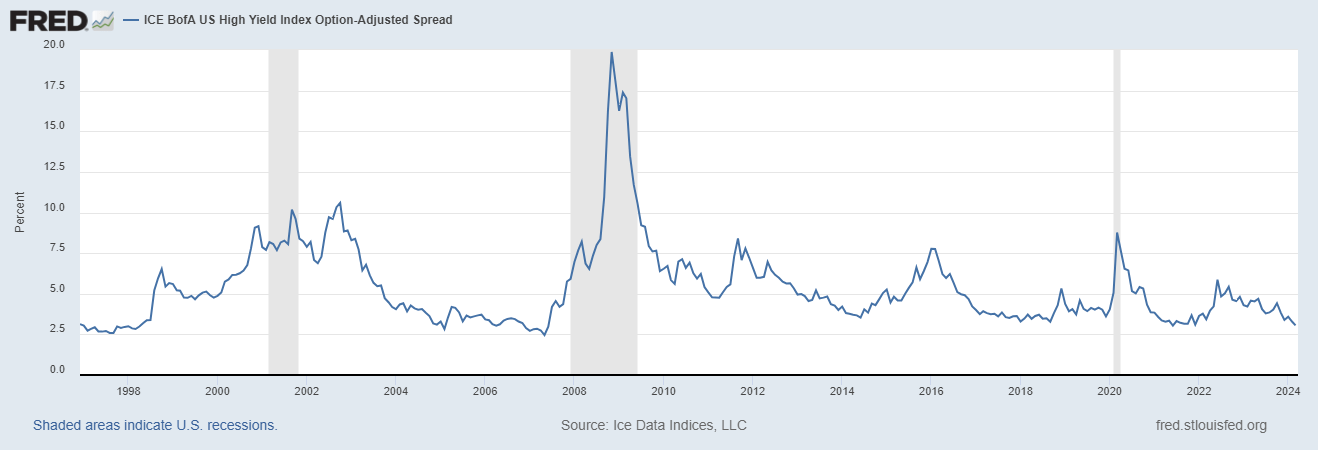

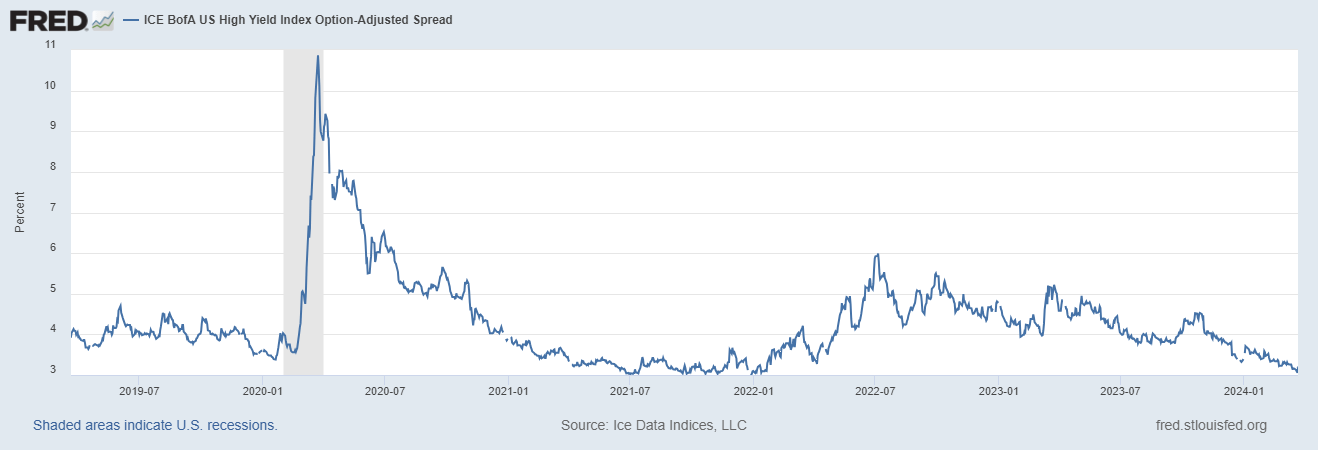

Given where option-adjusted spreads are (3.05%), it tells you that fixed income investors believe the economy is wonderful, or, that they believe the Fed will take rates to zero. Otherwise, there ought to be a much wider spread between High Yield bonds and Treasuries given high yield credit risk in the aggregate.

The High Yield - Treasury spread sits at 3.05% - far too low. When spreads eventually widen, it will be a sharp, abrupt widening. If spread widening does not occur in the next 24 months, it will be because the Fed took rates back to zero and the fiscal side will have continued to stimulate the U.S. economy with deficit spending - which of course will only make the ultimate day of fiscal reckoning worse. In the meantime, expect CPI to go higher when the best thing for Americans would be for a flat CPI environment after prices come down to offset the prices increases of late 2020 through today - courtesy of poor fiscal and monetary policy.

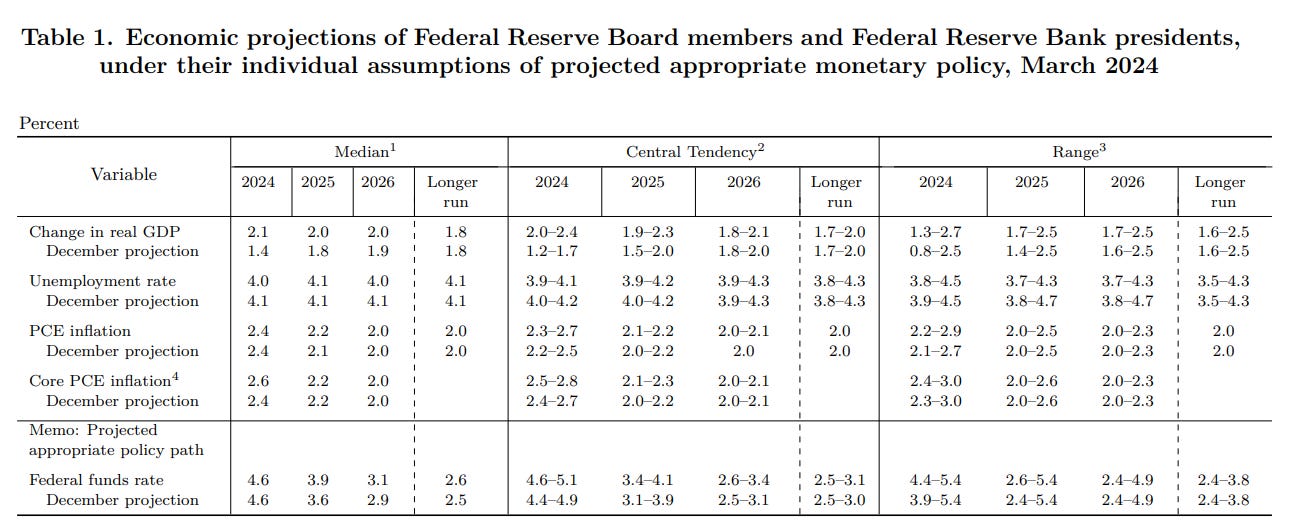

If the Fed took its Fed Funds down to 3% or 4% tomorrow, many high yield credits would have a problem when the time comes to roll over debt that was issued when Fed Funds was at zero percent. There will be many corporate debt issues that are due to mature in 2024 - 2027 that were issued when Fed Funds was at zero. We will witness the death of many high yield credits should the Fed do what it has outlined in its economic projections (below), which would be to maintain its Fed Funds rate above 3% through 2026. I simply do not believe the Fed will do so. I believe Fed Chair Powell will take Fed Funds back to 0-1% within 24 months.

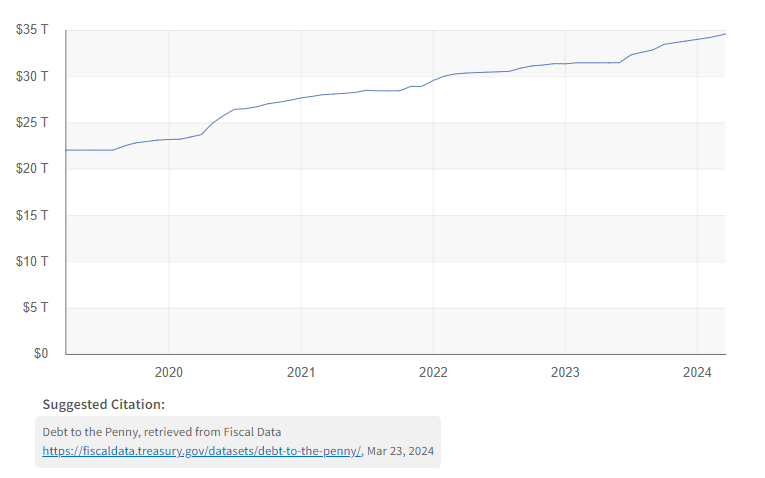

Investors forget that the United States has a $34.6 Trillion (yes, it grew by $200 billion since TEK2day’s last printing) mountain of debt that is strangling the country. Interest payments due are substantially less when Fed Funds is at zero percent. Therefore, Fed Funds will be back to zero percent.