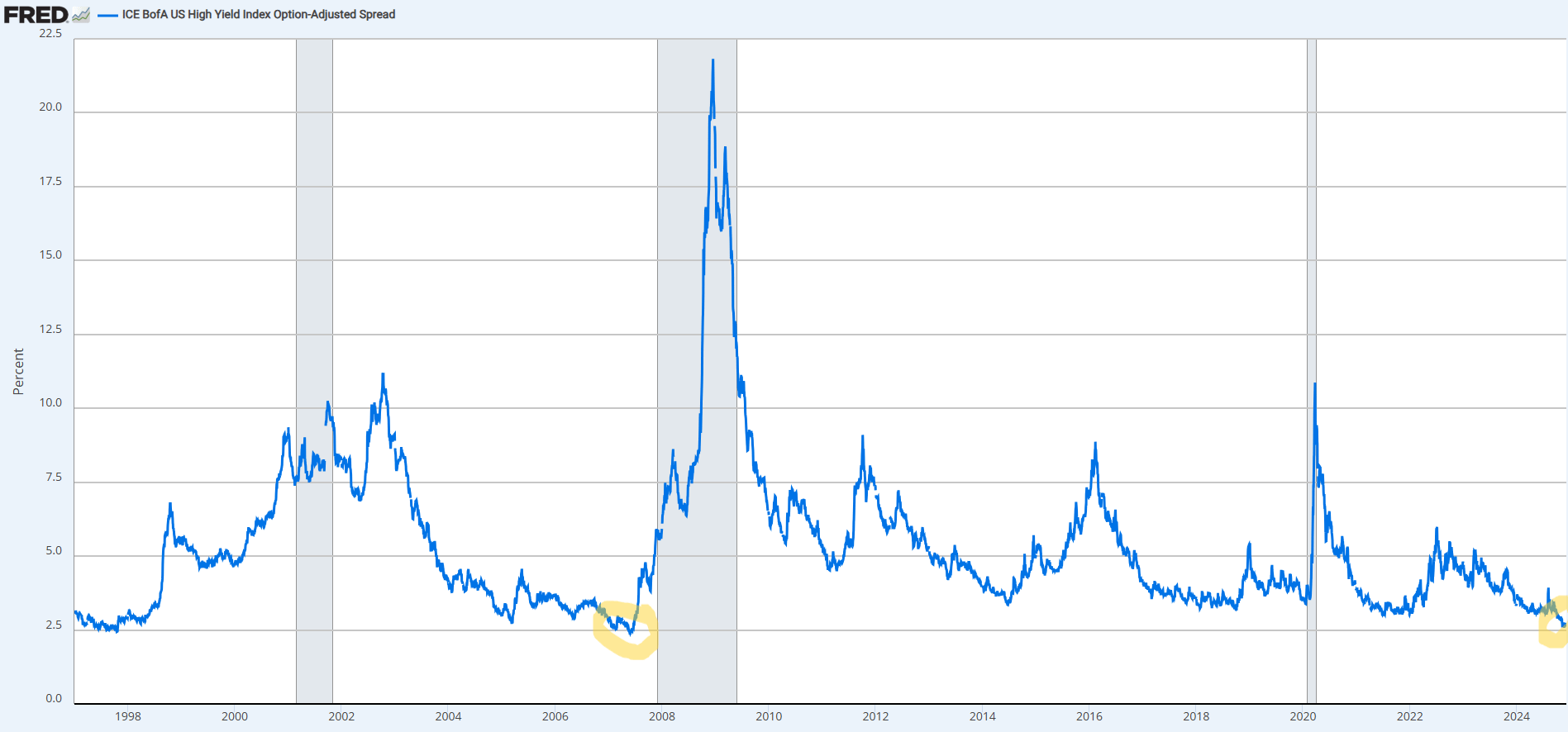

High Yield Spreads Say Financial Conditions Are Easy

How can one argue that financial conditions are tight when high yield spreads are as tight as they were in 2007?

Liquidity is plentiful, speculative mania is alive and well (when you have grocery clerks telling you to buy bitcoin, you know you’re at a top in the market). The question is, how long will this top last before the inevitable fall?

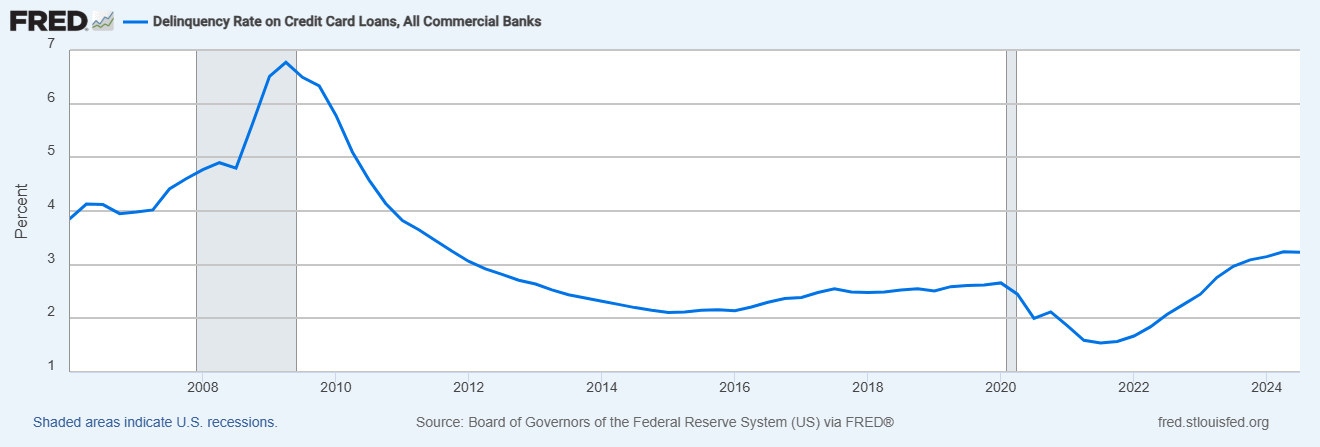

I believe the bond market is wrong about credit spreads given that credit card delinquencies are back at 2011 levels and the number of bankruptcies continue to grow. My guess is that the Fed will be in full QE swing in 2025 working to push the yield curve in the out years lower. Let’s hope the Fed does not intervene.

Watch the 10-year Treasury yield. If the Fed continues to lower the front-end of the yield curve and the 10-year remains above 4%, the Fed may step in with QE. If in 2025 under new Treasury Secretary Bessent the 10-year yield was to move above 5%, the Fed will absolutely engage in a new QE program at the long end of the curve, which of course will only exacerbate the Debt and Devalued Dollar (i.e., inflation), problem that is the 800 pound Gorilla in the room. Russia is not the problem, Iran is not the problem, China is not the problem. The fact that the money supply has been inflated by 40% over the past several years while the Dollar has lost 46% of its value versus gold over the same period is the problem all Americans ought to be concerned with.