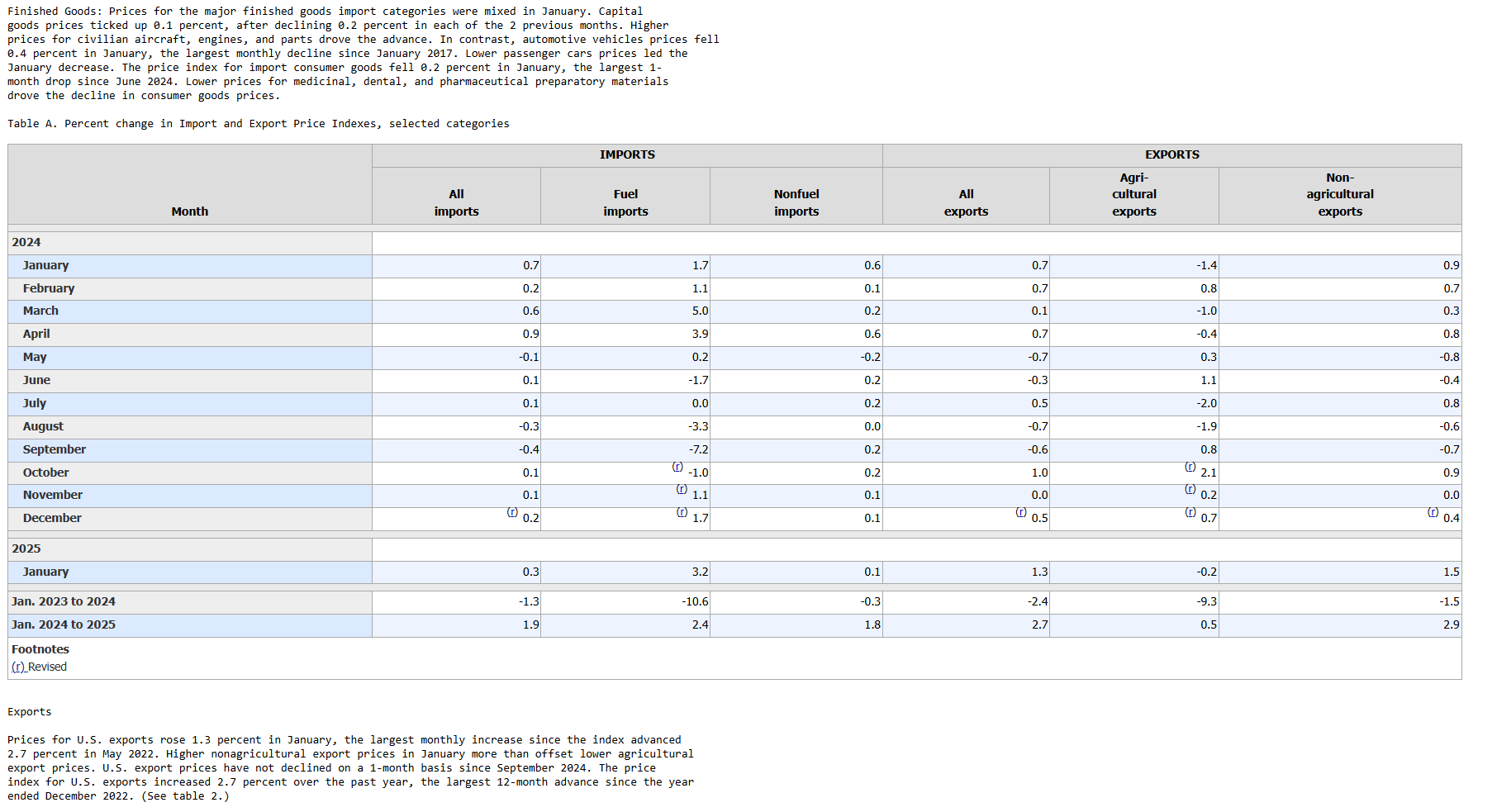

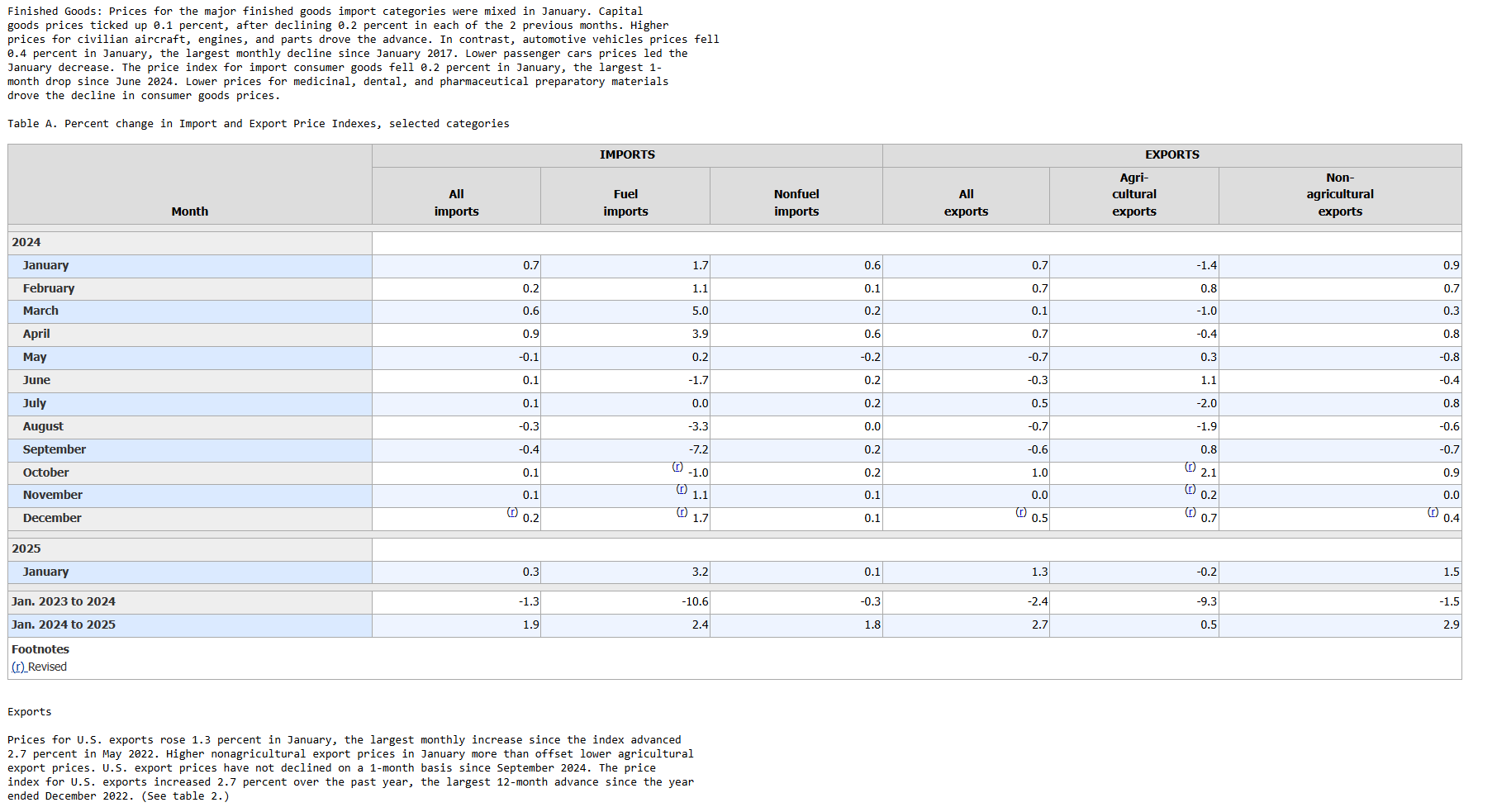

Import Export Prices Suggest Yields Are Too Low

I was hoping to turn this into a podcast, but a podcast is not in the cards today. The short story is that between CPI and today’s import/export prices, prices are headed in the wrong direction. At risk of sounding like a broken record, the 10-year Treasury yield ought to be significantly higher to reflect both the elevated price environment and the fact that the U.S. Government will continue to operate at a loss as far as the eye can see - or at least until it manifests the courage to restructure entitlement spending.

U.S. Debt to Federal Tax Receipts is $36 Trillion to $5 Trillion = 7.2x.

U.S. Debt plus Unfunded Liabilities ($36 Trillion plus $71 Trillion) to Tax Receipts ($5 Trillion) = $107 Trillion to $5 Trillion = 21.4x

Who would invest in a cash-burning company with these debt ratios to only be compensated with a 4.5% yield on a 10-year security in an environment where prices are moving higher? Nobody on earth would take that trade.

The only reason that the U.S. is not in default is because it still has the ability to issue new debt to pay down the old. It cannot pay down the old with cash from operations. Every new debt issue therefore carries more default risk. Therefore, the 10-year needs to move higher than the delusional 4.5% present yield.

If you do not share my level of concern, simply look at Treasury issues over the past 5 years. The market greatly prefers short-term maturities (T-Bills in particular, which have a maturity of less than 1 year), over longer-term Treasury maturities. This is because Treasury investors cannot see well into the future given the United States’ messy fiscal situation which creates a natural inflationary pricing environment.

Source: HERE