Look To The Fed's Discount Window For Insight Toward Banking Sector Weakness

Look to the Fed’s discount window in March to get a read on the strength of the banking sector (punchline: it is weak).

The Fed has publicly stated that it plans to allow its Bank Term Funding Program (BTFP) to expire on March 11th, 2024. As the BTFP winds down, one would expect a number of banks to utilize the Fed’s discount window (the Fed is the lender of last resort).

Banks are still carrying hundreds of billions of unrealized losses on debt securities purchased when interest rates were at or near zero percent. This problem is not going away.

The Fed’s discount window does not allow banks to mark-up the value of their underwater debt securities (used as collateral when borrowing from the Fed) to par value as was the case with the BTFP. Further, the Fed’s discount window does not allow banks to borrow at 100% margin as was the case with the BTFP (here is the Fed’s discount window collateral valuation and margin table).

This means that post-BTFP, banks will become more conservative in their lending practices. Banks will tighten credit in March. The Fed will likely loosen monetary policy at that time.

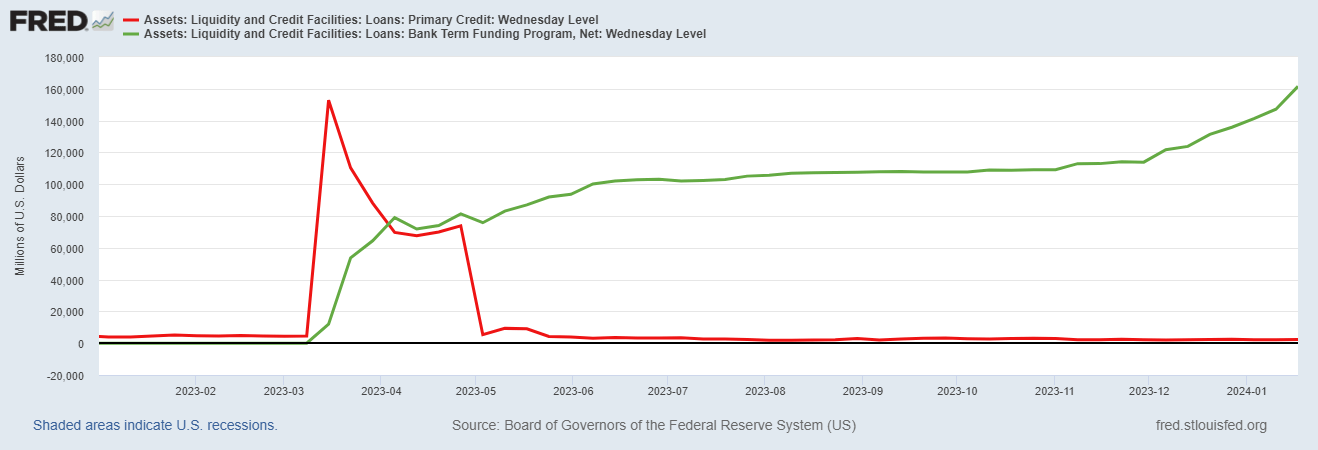

Discount window borrowing activity is reported each week.

The red line below details discount window bank borrowing.

The green line details BTFP bank borrowing.

Discount window borrowing spiked in March 2023 when banks ran into trouble in the weeks leading up to the Fed standing up its latest bailout facility, the BTFP.