Part 1: A Dangerous Precedent: Trump’s Attempt to Fire Fed Governor Lisa Cook Part 2: Money Creation

In an unprecedented move, President Trump has sought to fire Federal Reserve Governor Lisa Cook.

As if the Federal Reserve was not dovish enough, President Trump would like to place the Federal Reserve under Treasury’s purview where the Fed would essentially become Treasury’s dedicated banker, setting dovish rate policy at Treasury’s whim. Trump’s thought is remove Cook, weaken Powell’s standing and accelerate the move to lower the Fed Funds rate as Treasury plans to finance U.S. expenditures at the short-end of the yield curve. A federal judge has now temporarily blocked this attempt, reaffirming the principle that the Fed must remain insulated from partisan politic. That said, it seems to me that as it relates to fiscal and monetary policy, there is a singular view in Washington D.C. and that view is highly liberal. D.C. completely lacks fiscal and monetary discipline. Multi-trillion Dollar fiscal deficits and zero percent reserve requirements ensure that the money supply will continue to expand faster than Real Productivity (negative if you back out true price increases from GDP), thereby locking-in Dollar devaluation.

A First in Fed History

On August 25, 2025, President Trump announced on social media that he was removing Governor Cook, accusing her of “deceitful and potentially criminal conduct” based on unverified mortgage fraud allegations. This marks the first time in the Federal Reserve’s more than century-long history that a president has attempted to oust a sitting governor.

The allegations originated from Federal Housing Finance Agency Director Bill Pulte - a Trump appointee - who claimed Cook had listed multiple properties as primary residences to gain favorable loan terms. He referred the matter to the Department of Justice. However, no criminal charges have been filed, and Cook denies any wrongdoing, describing the president’s actions as politically motivated and outside the law.

The Court’s Response: Upholding Law Over Politics

On September 9, 2025, U.S. District Judge Jia Cobb granted a preliminary injunction preventing Cook’s removal while litigation proceeds, citing that the Federal Reserve Act permits dismissal only for "cause"- typically misconduct or neglect occurring during the governor’s term of service - not pre-appointment actions. Judge Cobb’s ruling underscored that allowing such a removal would violate due process and pose a serious risk to Fed independence.

Cook will continue to serve and participate in upcoming Federal Reserve policy meetings as the case unfolds.

Why This Matters: Fed Independence Must Be Preserved

The Federal Reserve’s institutional insulation from direct political control has been vital to its credibility. Central banks need authority to raise interest rates during inflationary periods - even when doing so is unpopular. Allowing a President to remove governors at will would compromise this independence, turning the institution into a political tool rather than a guardian of economic stability (which clearly the Fed has not been under Chairman Powell).

Fed critics who argue the bank is already “too dovish” might see this as an opportunity. But subordinating the Fed to fiscal priorities would exacerbate that bias: a central bank under political thumb becomes effectively an appendage of the Treasury, more likely to accommodate government borrowing rather than check inflationary pressures.

What’s at Stake

Legal Precedent: If Trump’s maneuver succeeds, it would rest on a dangerous reinterpretation of “for cause,” allowing Presidents to dismiss governors for political disagreements.

Market Confidence: Investors count on the Fed’s independence; politicizing monetary policy could roil markets, weaken the Dollar, and raise borrowing costs.

Long-Term Stability: A Fed aligned with short-term political goals risks runaway inflation and diminished credibility - both domestically and abroad.

The Fed already plays monetary policy fast and loose, in particular with its zero percent fractional reserve lending requirement.

How Money Is Created: Fractional Reserve Banking in the U.S.

The Mechanics of Modern Money Creation

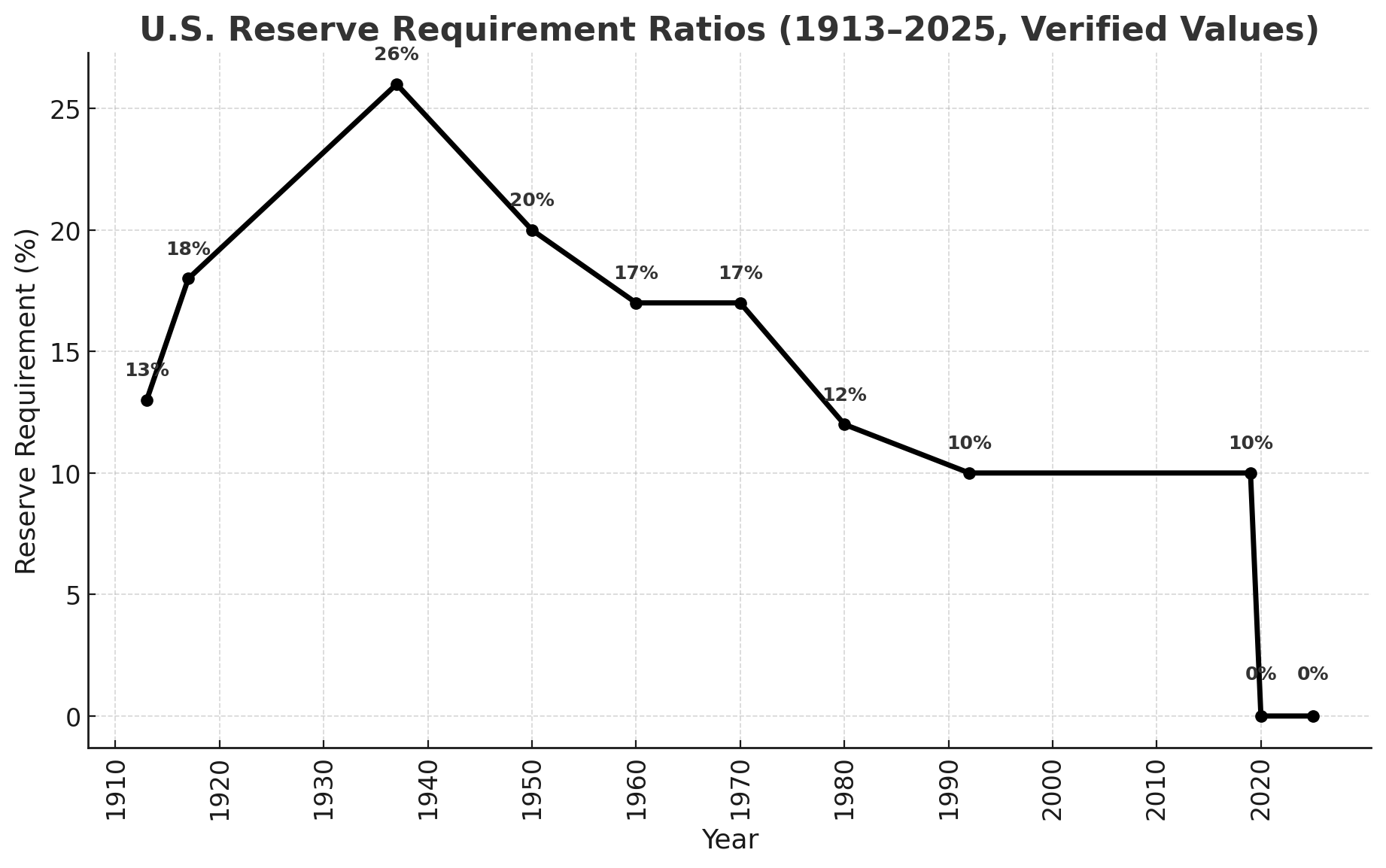

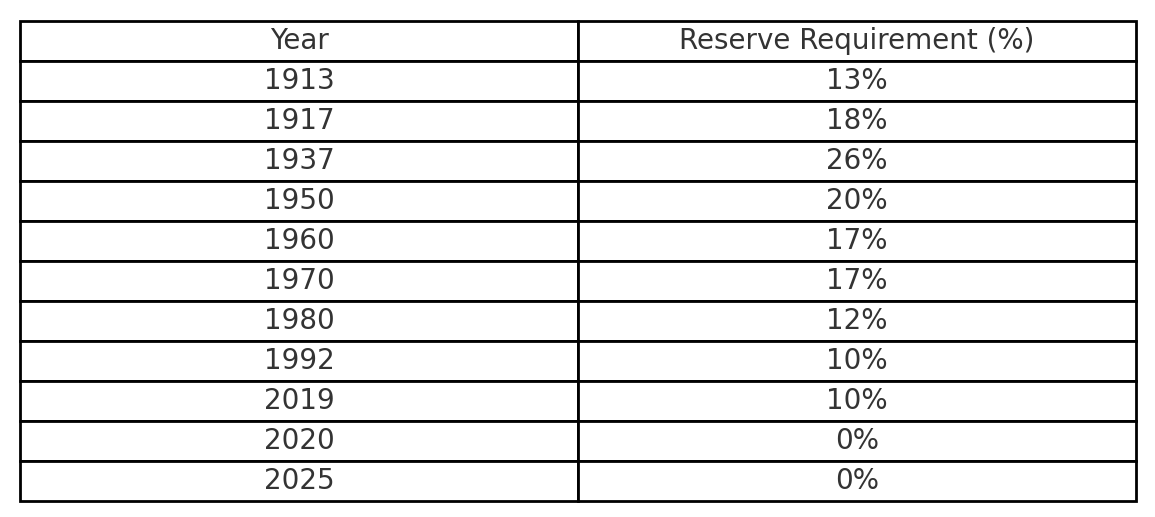

Contrary to the common assumption that the Federal Reserve “prints money,” most new money in the U.S. is created by commercial banks through the lending process. Under a fractional reserve system, banks are required to hold only a fraction of their deposit liabilities as reserves - either as vault cash or as balances at the Federal Reserve. The rest can be lent out. Since 2020, that reserve requirement is zero percent.

Here’s how the process works:

Deposit Creation: A customer deposits $1,000 into a bank.

Reserves Held: If the reserve requirement is 10%, the bank must hold $100 as reserves.

Lending: The bank can then lend out $900 to a borrower.

Money Multiplier Effect: When the borrower spends that $900, it is deposited into another bank, which then holds 10% in reserve ($90) and lends out $810. This cycle continues, expanding the money supply far beyond the original $1,000 deposit.

In today’s U.S. system, the formal reserve requirement has effectively been reduced to zero (since 2020), but banks are still constrained by capital requirements, risk assessments, and demand for credit. In other words, while reserve ratios once anchored money creation, now it is the interplay of regulation and market forces that defines how much money banks can create (and the Fed’s rate manipulation).

Historical Development in the United States

Early Banking and Free Banking Era (1790s–1860s)

Fractional reserve banking has existed in some form since the nation’s founding. Early U.S. banks operated with minimal regulation, often issuing their own banknotes backed by gold or silver reserves. Because reserves were limited, banks frequently over-issued notes, leading to periodic panics when depositors demanded redemption. The Panic of 1819 and subsequent banking crises underscored the fragility of fractional reserves without a central backstop.

National Banking System (1863–1913)

The National Banking Acts of the 1860s established a more uniform system. National banks could issue notes backed by U.S. government bonds, bringing some stability. Yet, fractional reserve lending still amplified credit cycles, and without a central bank, liquidity crises persisted. Bank runs were common, culminating in the Panic of 1907, which became a catalyst for deeper reform.

Creation of the Federal Reserve (1913)

The Federal Reserve Act of 1913 established the central bank as a lender of last resort and regulator of reserve requirements. By managing reserves, the Fed could influence credit creation, dampen panics, and stabilize the banking system. This was the formal institutionalization of fractional reserve banking in the U.S., marrying commercial bank lending with central bank oversight.

Depression-Era Reforms and Beyond (1930s–1970s)

The Great Depression revealed severe weaknesses in fractional reserve banking when thousands of banks failed. Reforms followed: the creation of the FDIC to insure deposits, stricter reserve requirements, and separation of commercial and investment banking under Glass-Steagall. These steps helped restore trust while constraining excesses of credit creation.

Deregulation and Modern Era (1980s–Present)

Over the late 20th century, financial deregulation, technological innovation, and globalization reshaped banking. Reserve requirements remained a key regulatory tool until the Fed reduced the reserve requirement ratio to zero in March 2020. Today, banks still create money through lending, but the process is bounded more by capital adequacy rules (Basel accords), liquidity coverage ratios, and central bank oversight than by fractional reserve rules in the old sense.

Why It Matters

Understanding fractional reserve banking clarifies why credit expansions and contractions have such profound effects on the broader economy. When banks lend aggressively, money supply expands, fueling growth but also risking inflation or asset bubbles. When banks retrench, money supply contracts, deepening recessions. This cycle explains why central bank policies - like setting interest rates or providing emergency liquidity - are critical to economic stability.

Conclusion

Fractional reserve banking has been both a cornerstone of U.S. economic development and a source of systemic risk. Its history - from the wildcat banks of the 19th century to today’s highly regulated financial institutions - shows a constant balancing act between credit creation and financial stability. While the mechanics of reserves have evolved, the basic principle remains: commercial banks, through lending, are the primary creators of money in the U.S. economy.