Peloton Shows High Yield Spreads Have Room To Widen

PTON is marketing a $1 billion debt issue at an 11.5% yield.

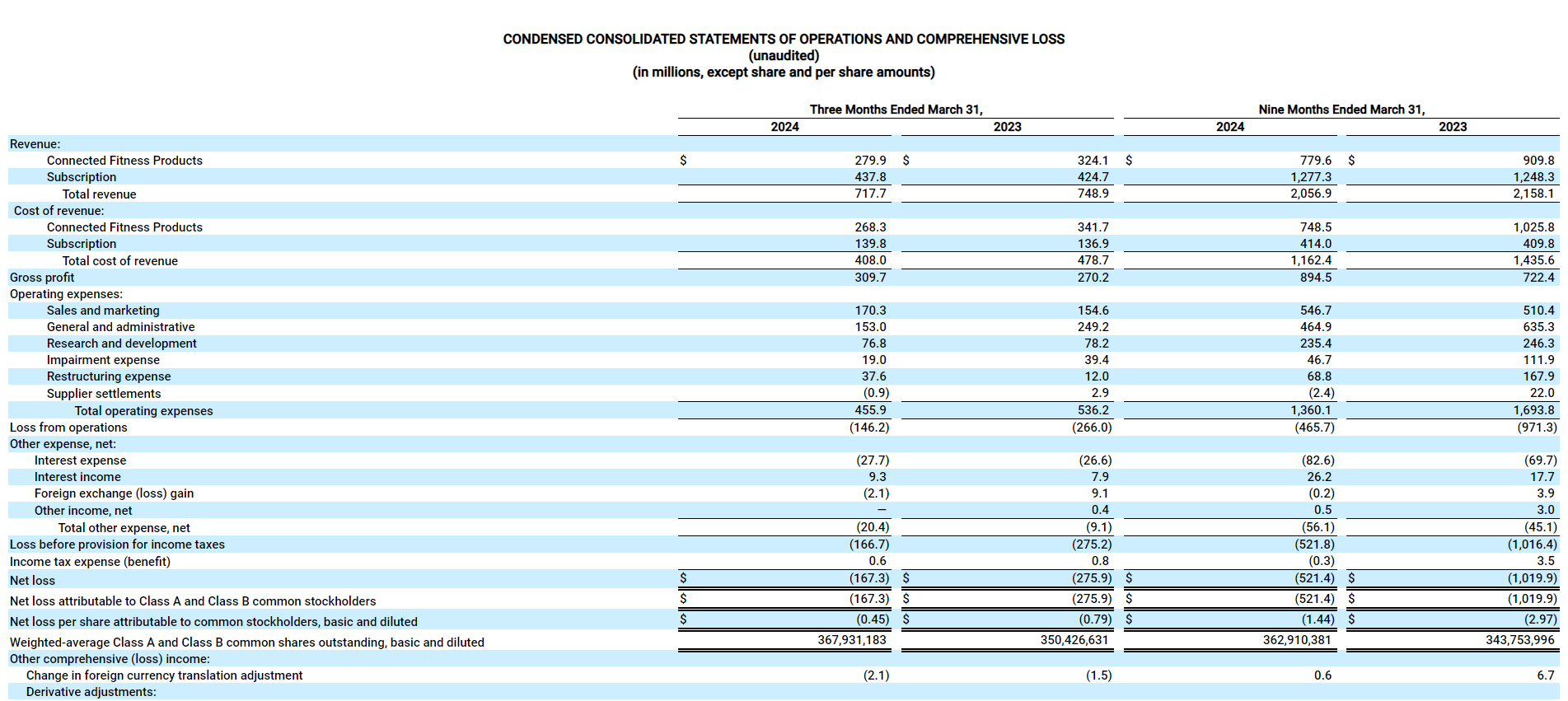

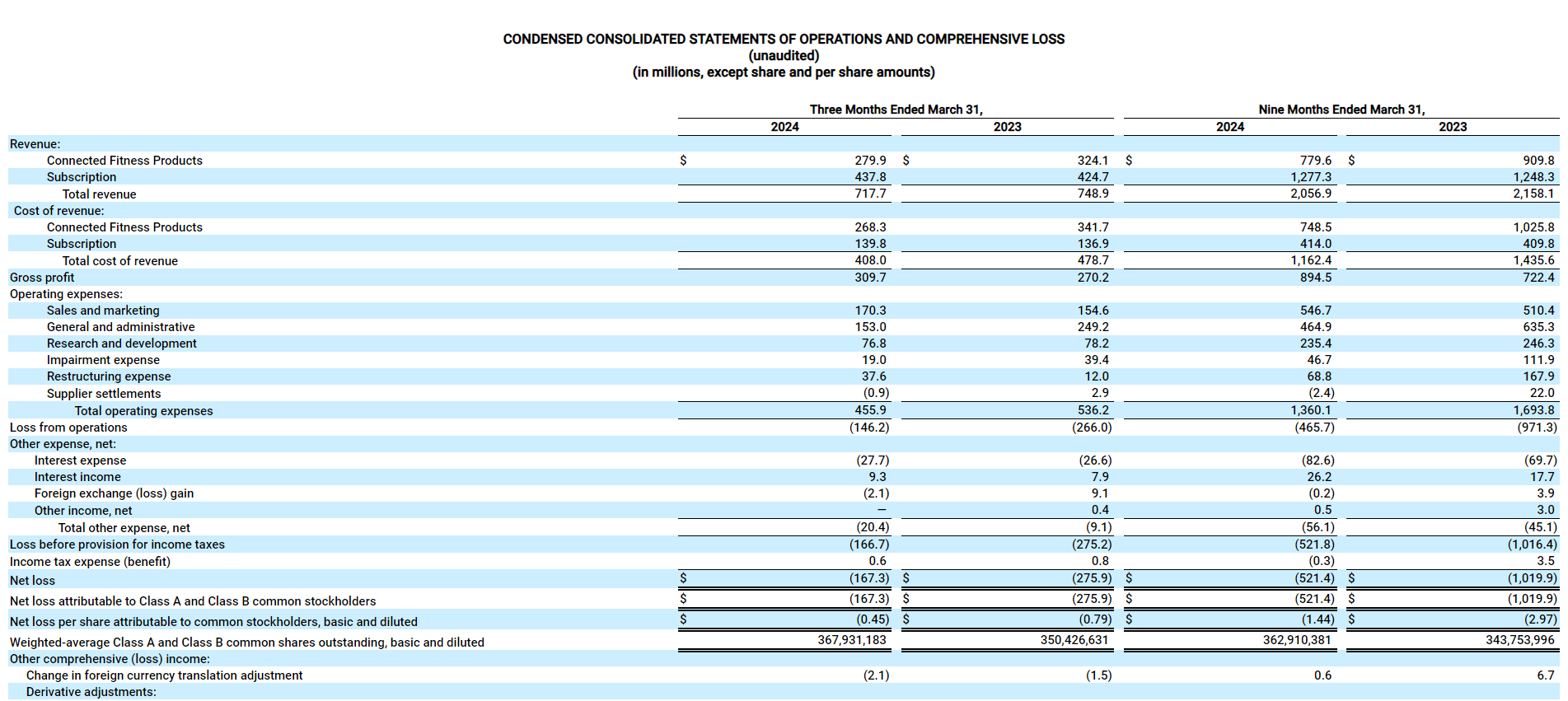

PTON’s Connected Fitness Products business is shrinking and is essentially a breakeven business at the Gross Margin line. It does not move the Cash Flow needle (unless of course PTON winds down this business unit).

PTON’s Subscription business is barely growing (only 3% Y-O-Y growth) and is Gross Margin profitable. Yet, how will PTON grow this business if Revenue growth requires increasing Sales & Marketing spend?

Free cash flow was only $8.6 million in the most recent quarter, which means OpEx has to be slashed in order to generate consistent free cash flow.

My guess is that a default is in PTON’s not-too-distant future. A 20-25% yield would not be sufficient for me to own PTON’s debt.

When will the ratings agencies get around to downgrading all of the corporate debt that needs to be downgraded?

Source: PTON