Short The Dollar

It is obvious - isn’t it? Treasury has been inflating the U.S. Economy since April 2020 via historical deficit spending levels. The Fed, also guilty of inflating asset bubbles - most notably housing - from April 2020 - May 2022, will soon get back into stimulation mode.

The Fed did not get out of the stimulation game entirely in May 2022. The Bank Term Funding Program (BTFP) of March 2023 was a Banking bailout that demonstrated that Government interventionism and Corporate Socialism is alive and well.

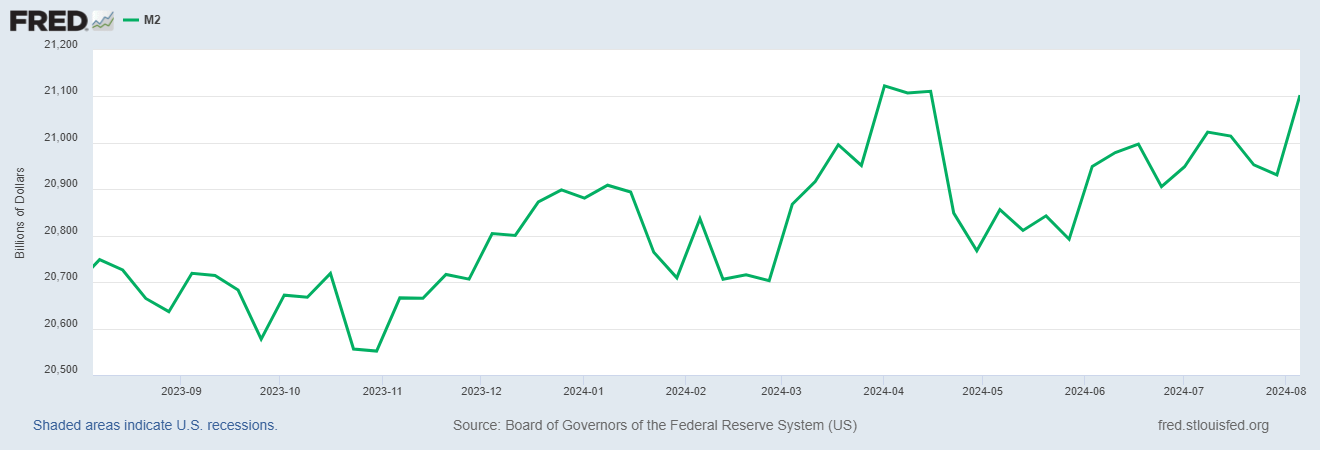

The Money Supply is growing. Further, the Fed in conjunction with the banking system has expanded the Money Supply as defined by M2 since May 2024.

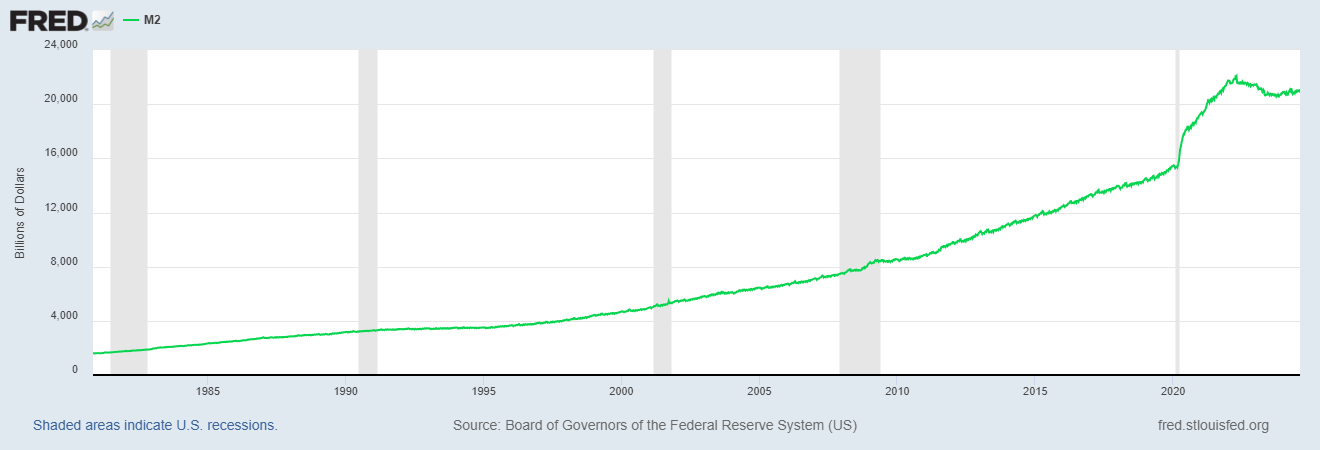

Someone forgot to tell Fed Chair Powell that if you wish to not have price inflation - do not grow the money supply when it is not tied to production (i.e. stimulus checks, QE, non-recourse credit facilities and subsidizing various Federal programs designed to distribute money in exchange for zero productivity). The Fed grew M2 by 44% between January 2020 and April 2022.

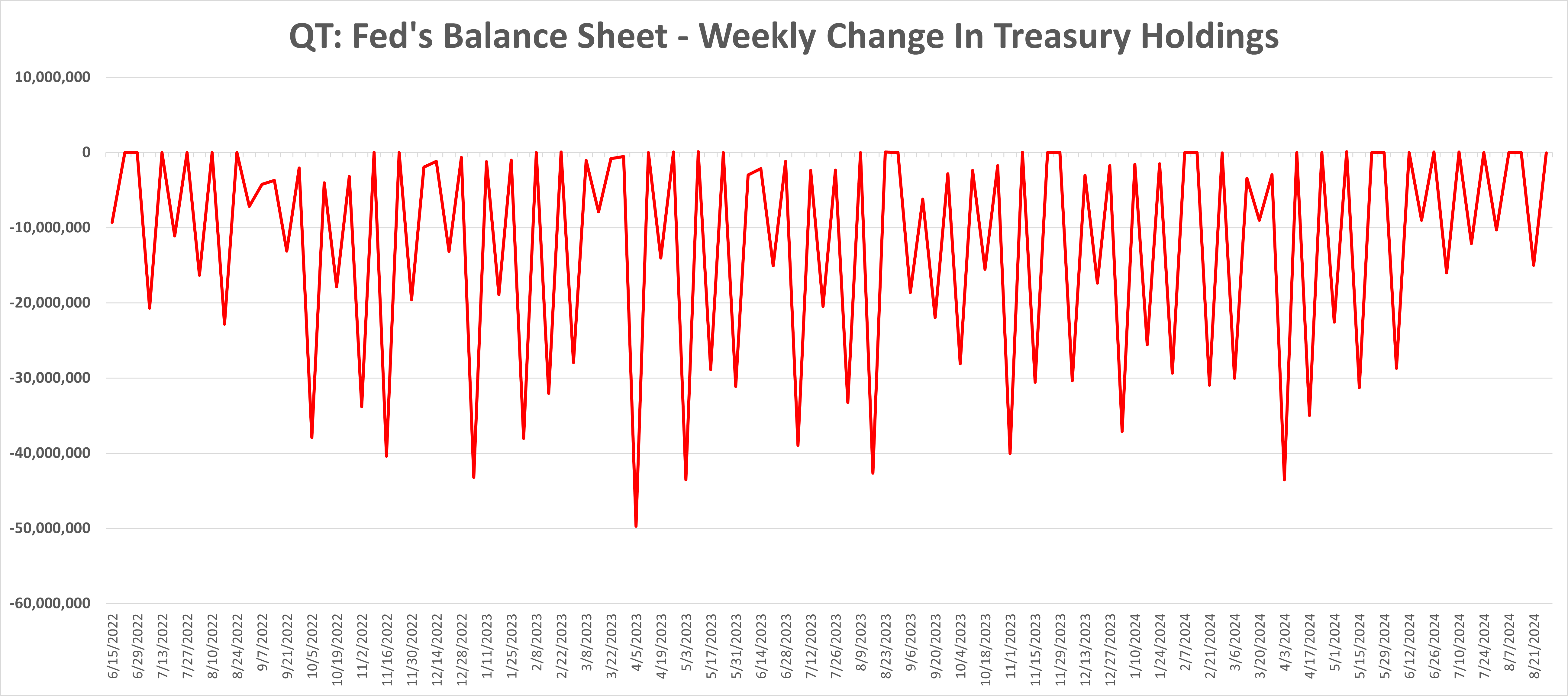

The Fed has also eased the pace of QT:

More fiscal and monetary stimulus is coming for the remainder of this fiscal year as well as the new fiscal year beginning in October. More fiscal and monetary stimulus means a weaker U.S. Dollar. The DXY ought to begin trading lower once the Fed lowers rates in September. Thus, the next asset bubble begins, but not due to greater productivity and wealth generation, but rather because of a devalued U.S. Dollar, which means less purchasing power for all Dollar holders. Therefore, I say short the U.S. Dollar.