Solera (SLRA) Saddled with Too Much Debt

My old firm is saddled with far too much debt. Debt to Adjusted EBITDA is more than 8x pre-IPO. Debt to Operating Cash Flow is 42x. Vista Equity loaded-up Solera with debt. It will take years to dig out of this mess.

Not much Revenue growth to speak of. Vista acquired Solera, (then ticker SLH), in 2016. Organic growth was 3-5% back then. It looks to be about the same, maybe a bit less growth now. Solera will not be growing its way out of debt.

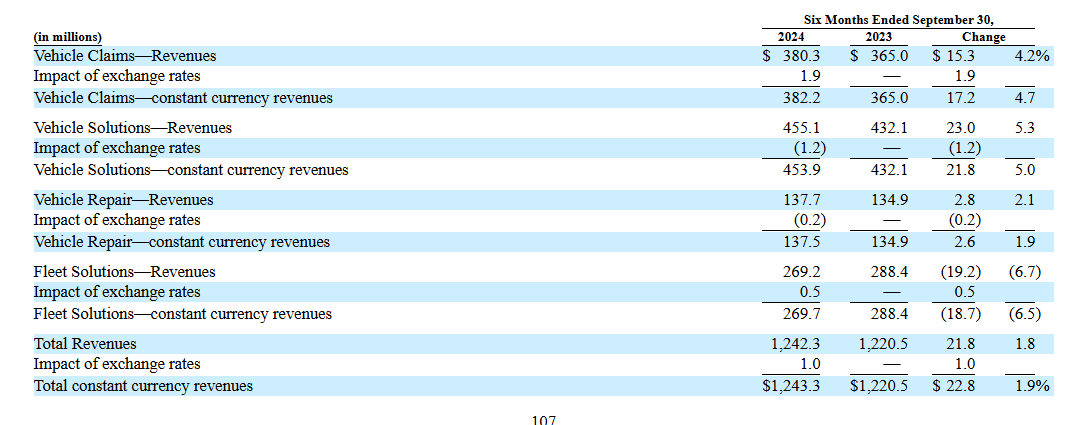

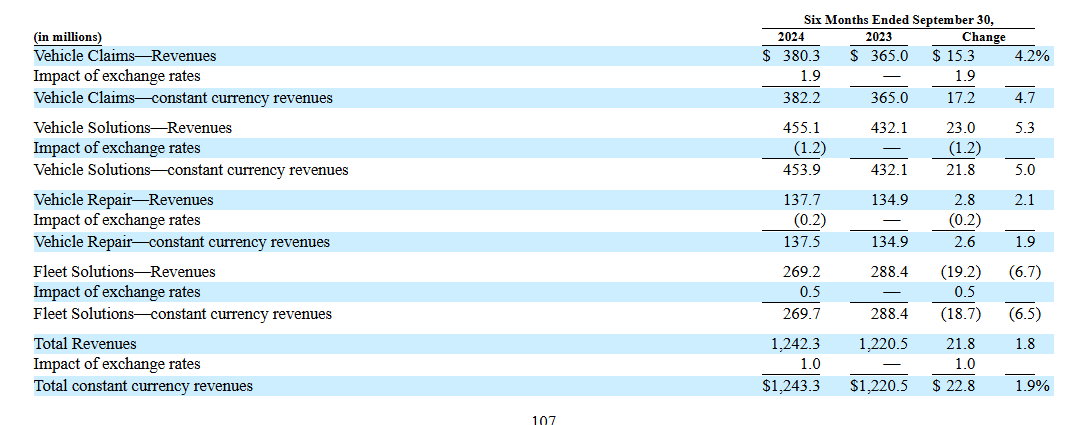

The S-1 offers too much detail in my view. Investors will clamor for this data each quarter and I’m not sure that I like the financial segmentation.

I would rather segment the financials by country, as each country used to have a country manager with P&L responsibility. I’m not sure if the company continues to run a decentralized operating model - which is THE only way to run a business. Give your people operating control and hold them accountable.

Decision by committee with no accountability does not work in Government, does not work in the NFL, and certainly does not work in business.

Vista caught between a rock and a hard place. The thing of it is, Vista has to take Solera public. What other PE firm could afford to acquire Solera and saddle it with even more debt?

Who loses? Solera loses. Good luck trying to invest for growth when your Debt-to-EBITDA ratio is north of 8x.

Source: Solera S-1