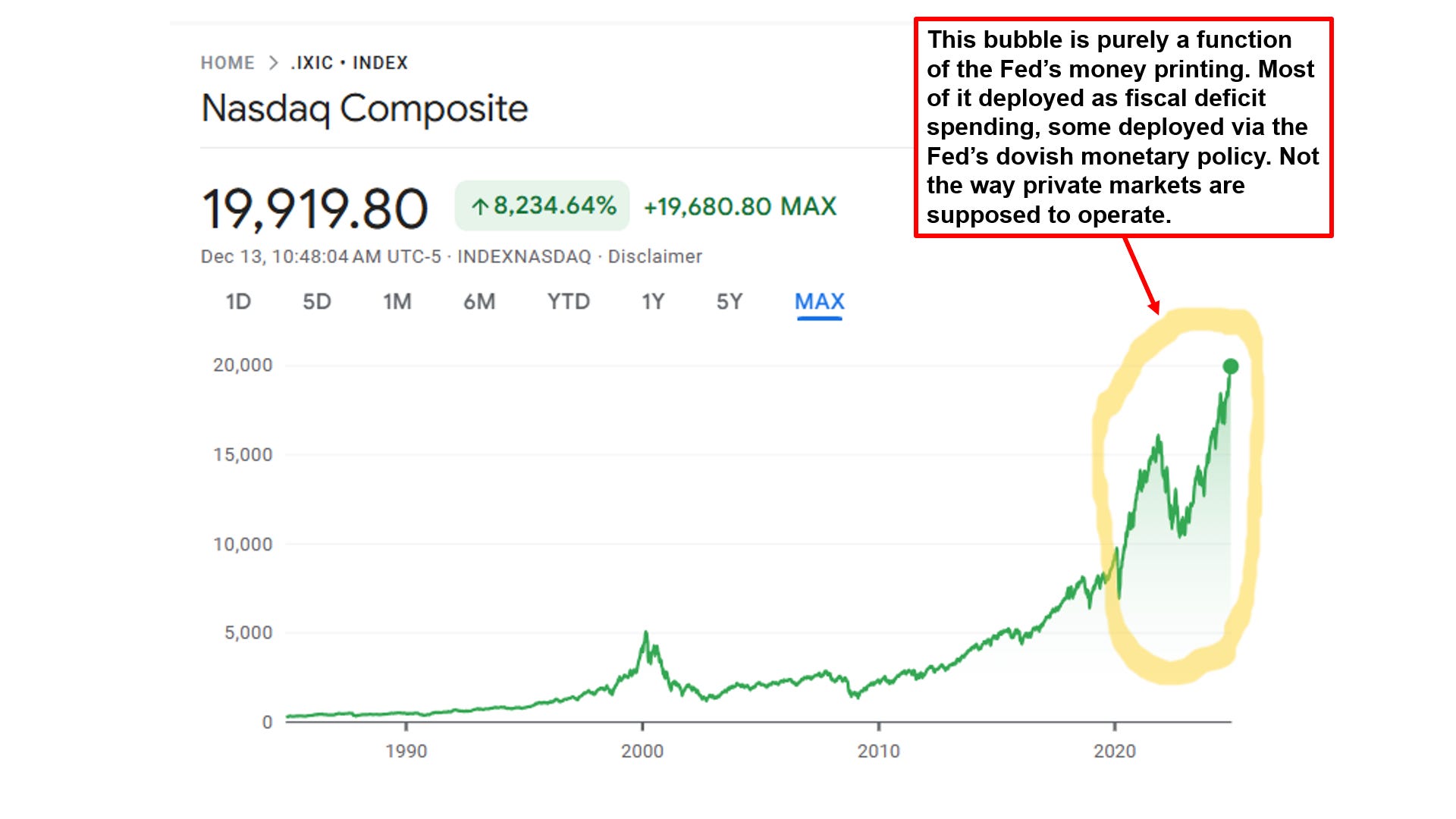

The Dollar Has Paid The Price for Expansionary Monetary Policy

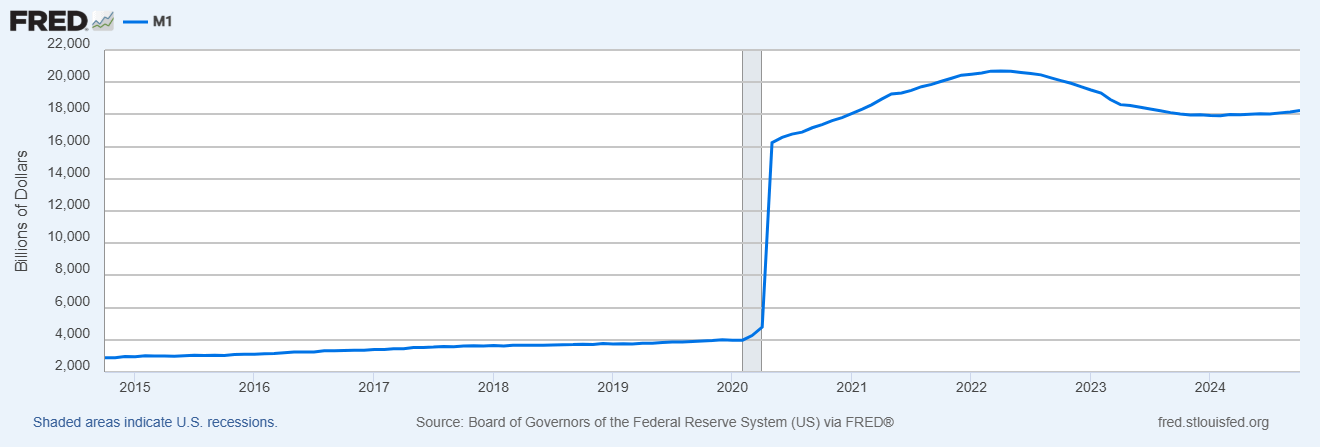

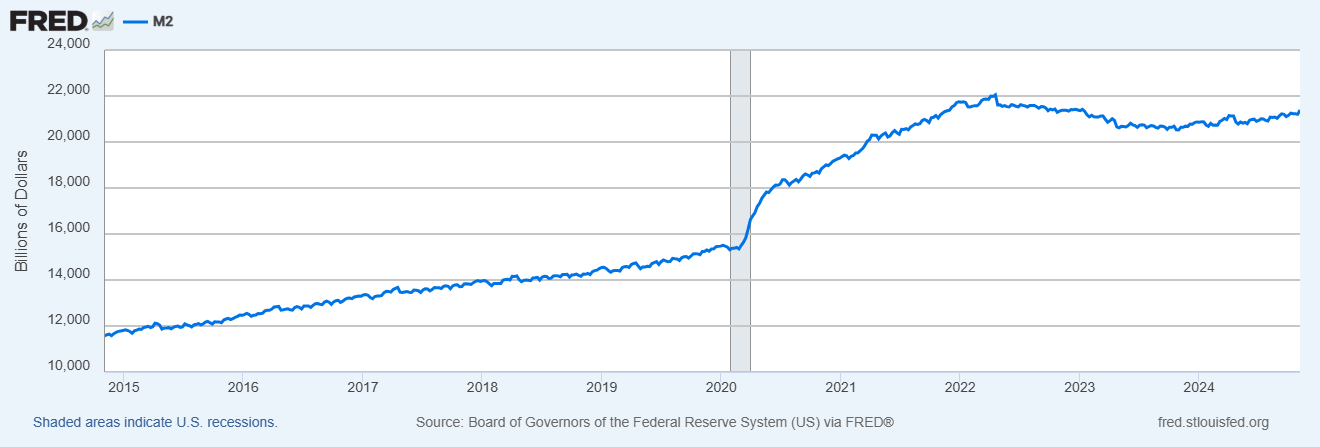

I have railed against the debt-generating, Dollar-dilutive fiscal and monetary policy that Congress and the Fed have pursued since 2020. Those institutions have nationalized the private debt and equity markets at great cost.

The value of cash and credit has declined by approximately 43% since January 2020 (as measured by M2). There is your hard landing.

Every fiscal and monetary bailout program (BTFP and multi-trillion Dollar deficits the most recent, a return to QE in 2025 or 2026 will be next as the Fed seeks to control the yield curve), can only further erode the value of the Dollar. A devalued Dollar is the only outcome of expansionary monetary policy.

Expansionary monetary policy may be good news for equities in the short-term, but is harmful to the real economy over the short, intermediate and long-term.

It is my hope that the more I call attention to this problem it will spark discussion on the topic. Even those who benefit in the short-term (BlackRock for example), ought to care about the long-term outlook for their respective firms. Should the real economy crumble, so too shall the BlackRocks of the world.

Meanwhile, the 10-Year Treasury yield ticks up to 4.4%. Should the Fed cut rates again next week, the 10-Year Treasury will see 5% in Q1 2025.