The Fallacy That The Fed Can’t Influence The Price of Oil

Financial talking heads often state that the Fed cannot affect oil prices. That is simply not true. For example, consider where the U.S. economy would be had the Fed increased its Fed Funds rate to 7% or 8%.

The cost of capital would be substantially higher;

CapEx would be substantially lower;

Headcount reductions would be more severe;

Bankruptcies would be more numerous, and;

Consumer purchasing habits would trend down faster than they are today.

All of the above translates to less demand for Oil/Energy. Less oil for: daily commutes, vacations, ground transportation, you name it.

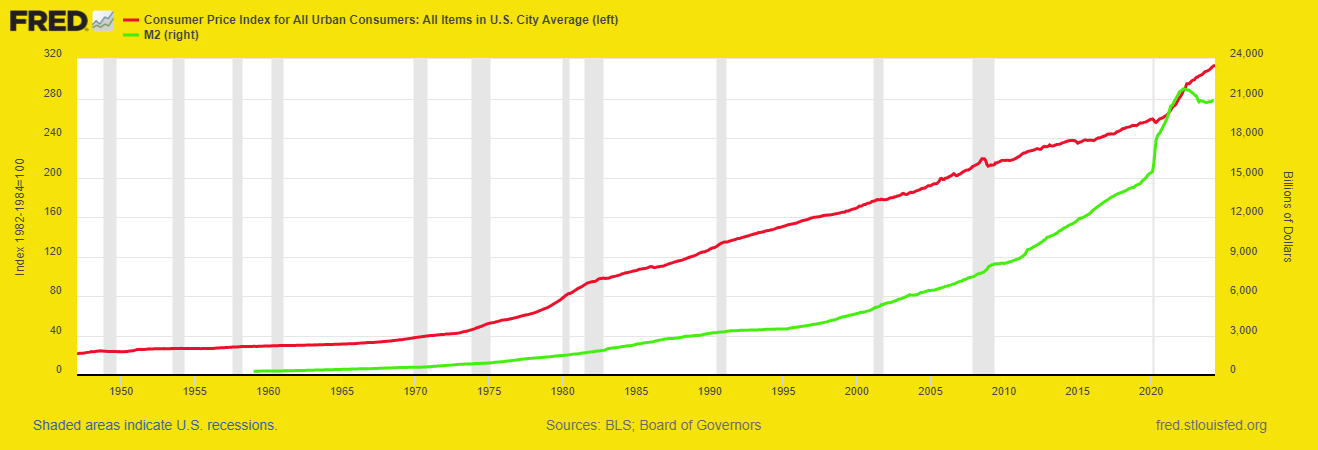

The Fed unfortunately impacts all pricing. Given the Fed’s misguided monetary policies over the past few decades (print first, ask questions later), prices have unfortunately moved in the wrong direction as the purchasing power of the Dollar continues to erode as a result of the Fed’s inflating the money supply. The chart below plots CPI (absolute pricing level) against the money supply as measured by M2. It is growth in the money supply that is not tied to productivity that causes price increases. The Fed’s propaganda about supply shocks and other various nonsense it spewed forth from 2021 through today about price inflation is just that - propaganda. The Fed will never admit that it is the cause of price inflation.