The Fed Has Eased Prematurely

The Fed threw fuel on the fire last week with Powell’s dovish comments. Market conditions were easing on weak economic data before Powell accelerated that easing with his dovish comments, increasing the risk of price inflation climbing higher, or being more stubborn than it needs to be.

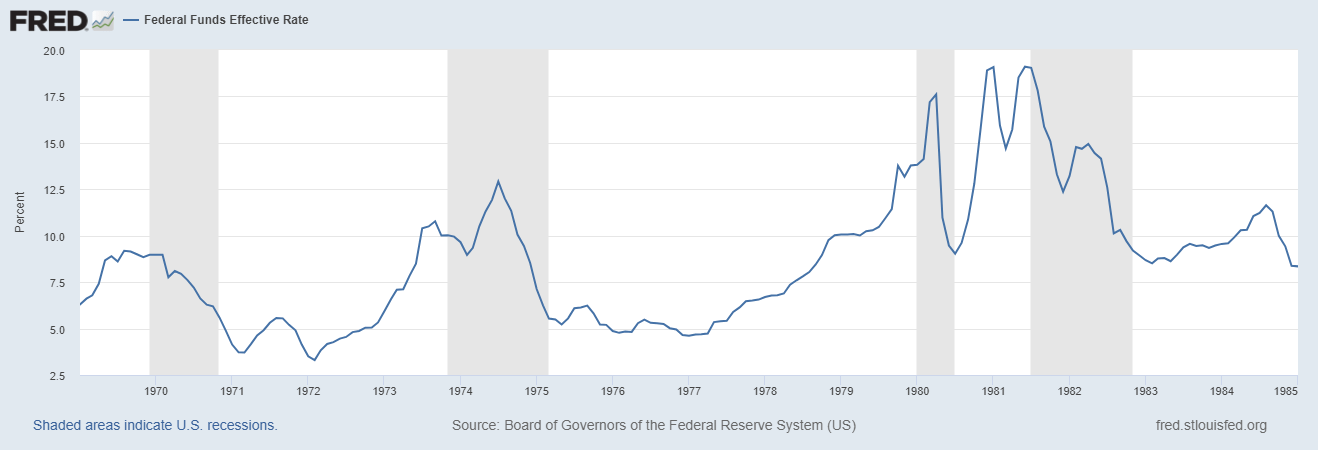

If you missed today’s podcast (you may find it HERE on our YouTube channel) we stated that Fed Chair Powell is Arthur Burns 2.0.

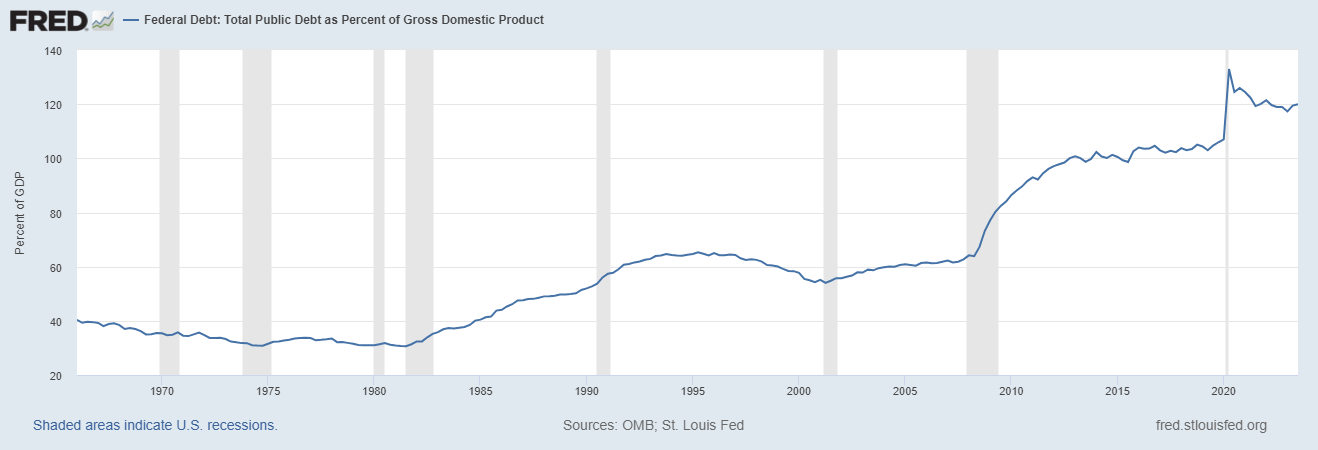

Arthur Burns of course is the former Fed Chair (February 1970 - January 1978) who prematurely loosened monetary policy, which allowed price inflation to bounce back to new highs before incoming Fed Chair Paul Volcker beat it back with a stick in the form of a 19% Fed Funds rate (Volcker of course did not have to deal with a mountain of Treasury debt that was larger than GDP, see 2nd chart).

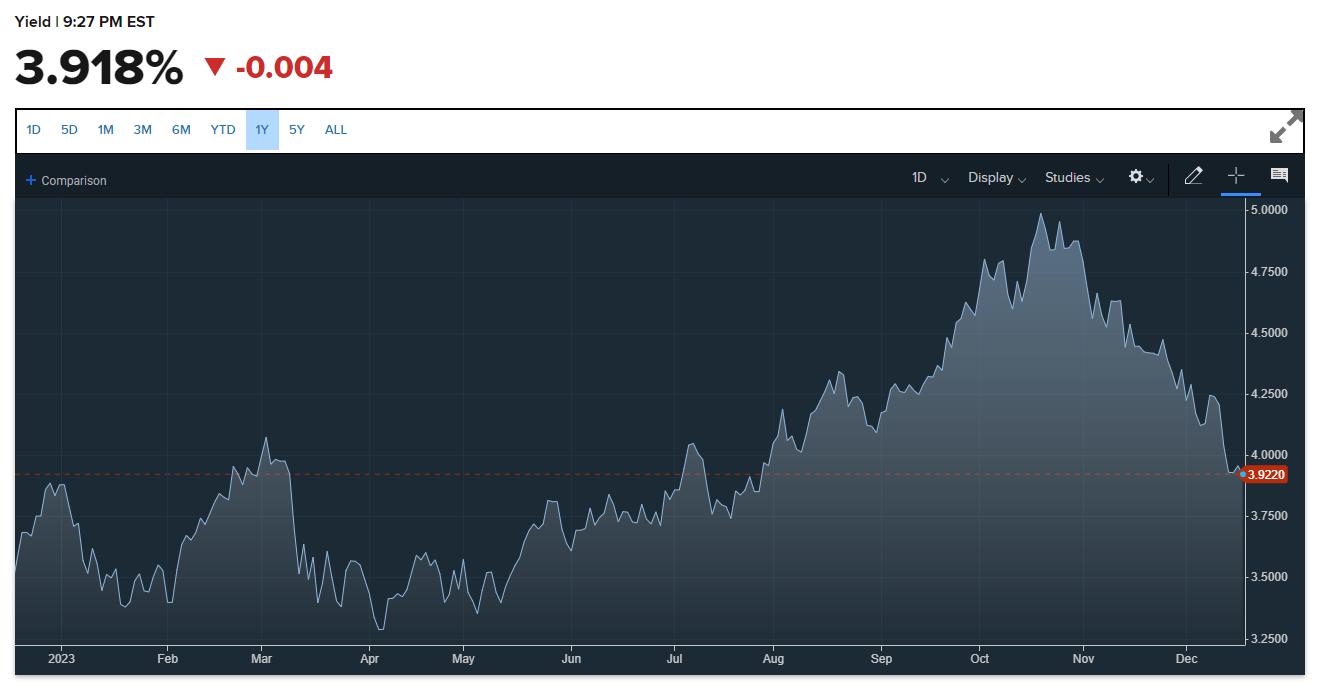

10-Year Treasury Yield retreats on Powell’s dovish comments: The 10-year Treasury yield had already declined to 4.2% from 5.0% on weak economic data and has since retreated an additional 7% to 3.9% since Powell’s dovish comments on December 13th.

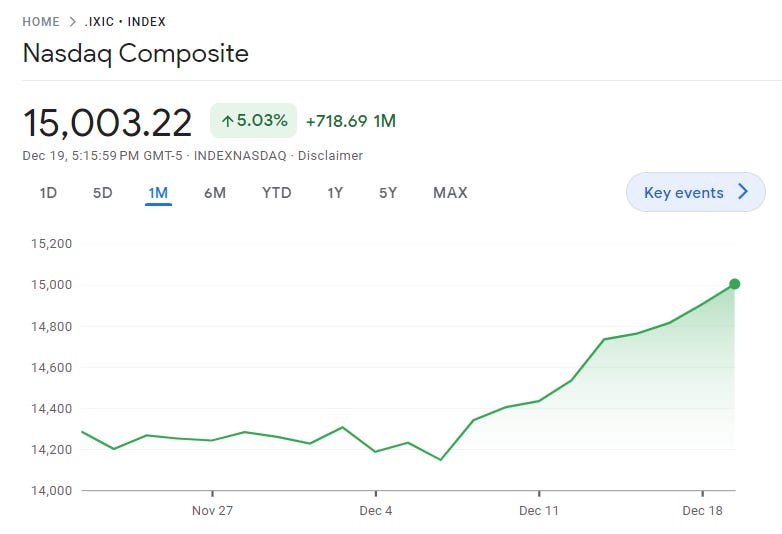

Adding fuel to the NASDAQ fire: The NASDAQ is up 6% over the past 12 days with half of those gains coming since Powell’s remarks last week. The NASDAQ is up 44% YTD heading into a recession. What is the probability that Portfolio Managers sell in the next few weeks once 2023 returns are locked in? I’d say quite high.

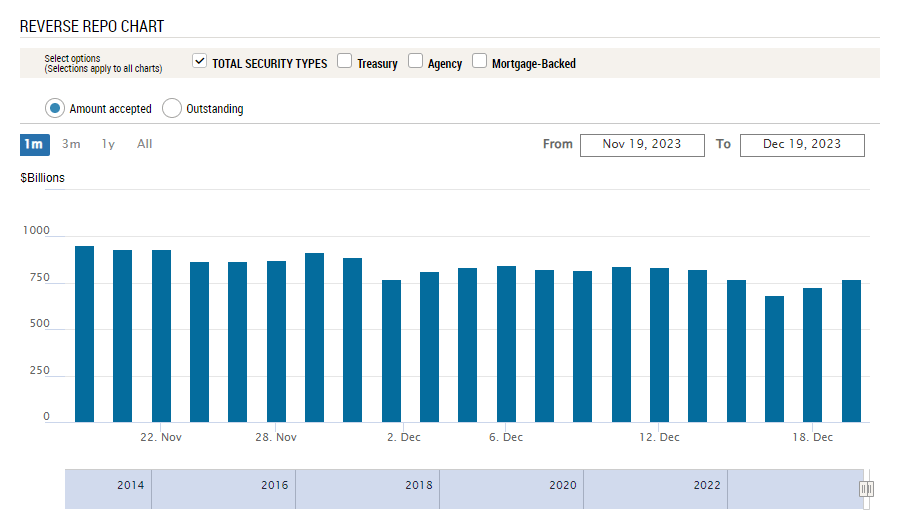

Do banks and non-bank institutions have incrementally more excess capital to park overnight with the Fed? It would seem the answer is “Yes”: The Fed’s Overnight Reverse Repo facility (ON RRP) - a proxy for excess liquidity in the system - has started to climb higher over the past several days.

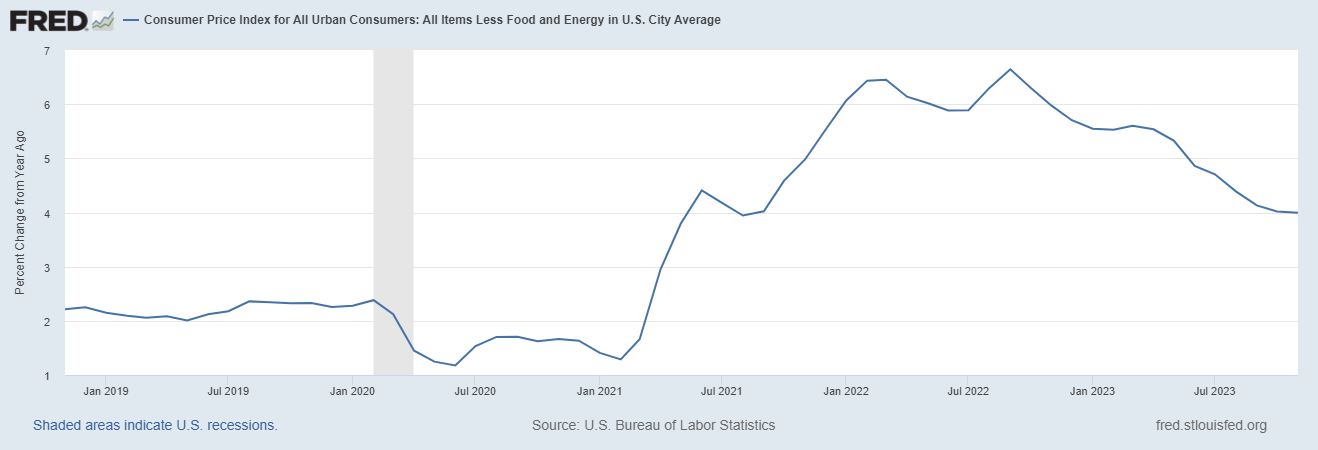

When will a 2% CPI be achieved? The Fed pushed that horizon outward when Powell spoke at last week’s FOMC meeting. Recall that Core CPI sits at 4% year-over-year and was flat month-to-month. That’s quite a ways away from the Fed’s 2% target. Further, why is 2% CPI accepted by the general public, the business community and the investor class? Why is 2% annual currency devaluation a good thing? Prices ought to come down if supply is plenty and production is high.

Some questions:

Will the Fed lower its Fed Funds rate this year? Yes. The Fed has no choice but to lower its Fed Funds rate given the $34 Trillion debt load the U.S. carries. The average interest rate on that debt now sits at 3.1%.

The question is when? My guess is toward the end of Q1 2024. Historically the equity market does not bottom until after the Fed lowers.

How low will the Fed go? Much lower than what it is letting on to for 2024. The Fed could find itself at a 2% CPI very quickly.

Will the Fed end QT? Yes. Also sometime in Q1. I prefer the Fed lower its Fed Funds rate to around 3% in the near-term, but that the Fed simultaneously increases its QT effort to be equal to its QE effort of 2020-May 2022.

What will Tech company 2024 guidance look like? Conservative on the top and bottom lines. Analysts will be required to lower estimates.