The Fed Is Well BELOW The Neutral Rate

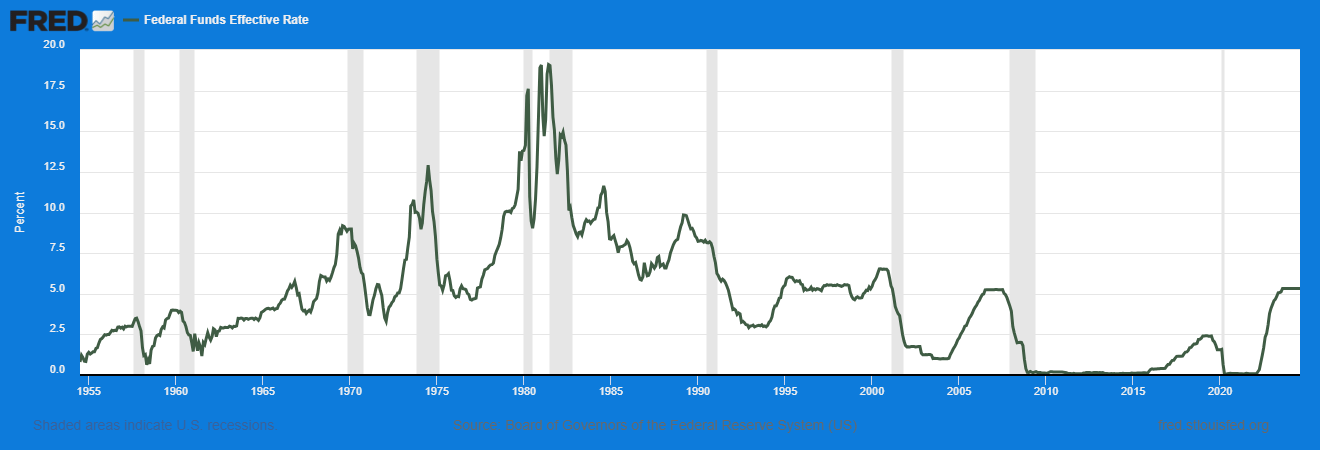

Core CPI is 3.2%. Fed Funds is 5.25-5.50%. Therefore, Fed Funds is in positive territory, correct? Incorrect.

CPI is woefully understated. CPI rotations are enough to render the figure worthless. CPI has not measured the price of goods and services on an apples-to-apples basis since the 1980s. Instead, the “rotation” methodology used to calculate CPI assumes that consumers rotate down to less expensive comparables (rotate down to ground beef from filet as an example) when the price of filet spikes in this example. This methodology precludes investors from measuring the true cost of price inflation. This is no accident, as CPI is used to calculate Social Security payouts. The lower the CPI kicker, the better if your name is Janet Yellen and your largest fiscal expense is Social Security payments ($1.34 Trillion as of August 31st).

The 10-year Treasury yields 3.6% (nominal yield), which means the 10-year carries a negative real yield. Fixed income funds are not performing as well in real yield terms as they advertise they are.

If the Fed eases Wednesday and in the months ahead, and if the fiscal side of the house continues to run large fiscal deficits through fiscal 2025 (fiscal 2025 begins October 1st 2024), then the combination of expansionary monetary and fiscal policy could turn the screw several notches on the stagflationary environment we are already living in, which means a no-to-low-real growth economy saddled with high debt, high future debt obligations (1.2x Debt/GDP), high taxes and high prices. Good luck growing out of that morass.

The permanent solution to long-term sustainable, Real GDP growth is to restructure entitlement spending (Social Security, Medicare, Government subsidized Healthcare, Housing and Education). Instead, the Fed has already significantly slowed the pace of QT and could be adding fuel to the stagflation fire by lowering its Fed Funds rate Wednesday.

$20 eggs anyone?