The Fed’s Balance Sheet Reduction (QT) Update

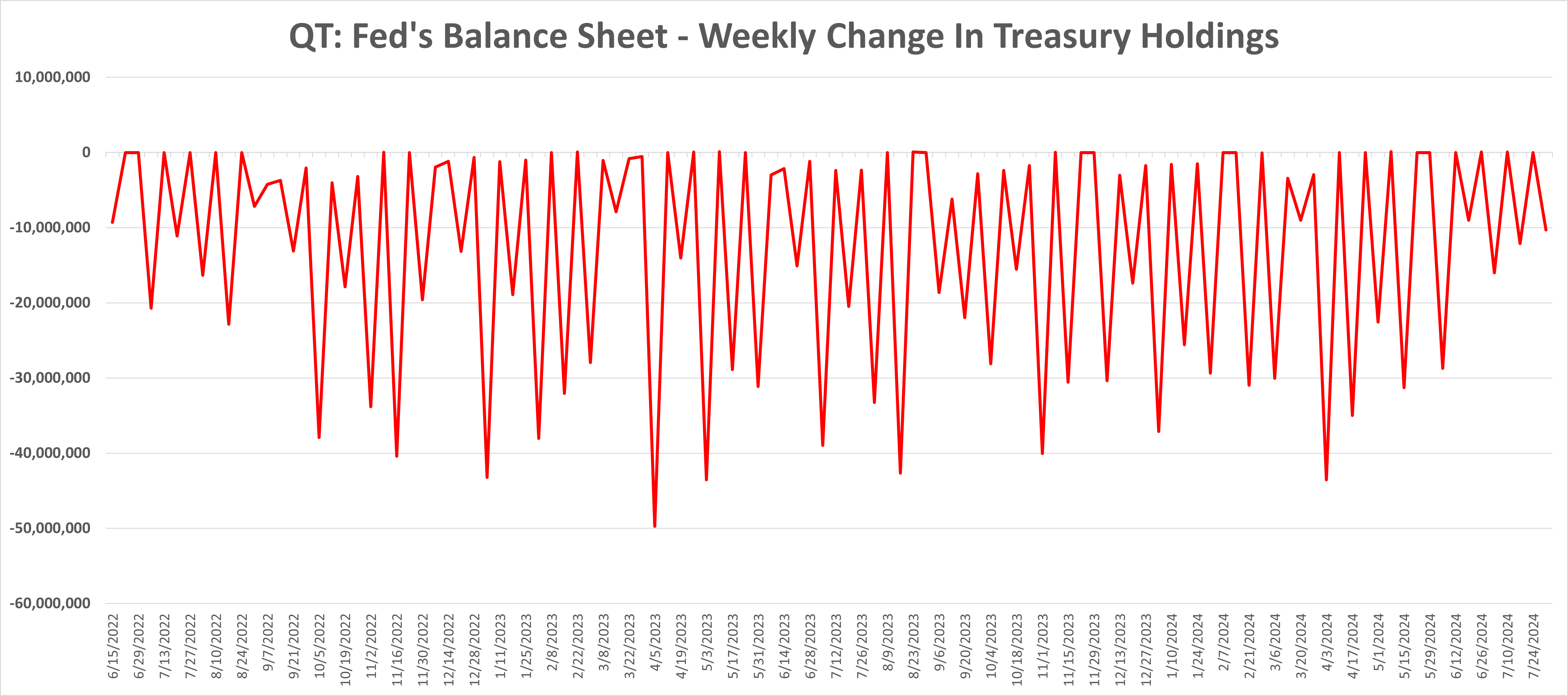

The Fed continued its modest QT program for the week-ended July 31st having trimmed its Treasury position by $10 billion and its mortgage position by $14 billion. Our monetary policy view has been that the Fed ought to have been less aggressive on rates and far more aggressive about shrinking the money supply. The Fed’s expansion of the money supply from January 2020 - April 2022 caused prices to explode. The best approach toward gaining control of rapid price increases is to contract the money supply, albeit at a far more rapid pace than the Fed’s tortoise-like pace. However, the damage is done as the U.S. has permanently elevated prices levels. The fact that year-over-year CPI increases have slowed is irrelevant. Last, do not be fooled by the Fed as the central bank will have its Fed Funds rate back at zero percent next year, which will reduce the interest expense burden on the United States’ $35 Trillion mountain of debt.

Treasuries: The Fed’s Treasury security holdings declined by $10.3 billion for the week ended July 31st. The Fed’s Treasury holdings declined by $22.4 billion on a rolling 4-week basis.

Agencies: The Fed’s Government Agency security holdings declined by $14.0 billion for the week-ended July 31st and declined by $17.8 billion on a rolling 4-week basis.

The Fed’s balance sheet holdings: https://www.newyorkfed.org/markets/soma-holdings

Excel file: Our Excel file detailing the Fed’s holdings of Treasury and Agency securities: HERE.