The Fed's Feeble Attempt To Tame Inflation

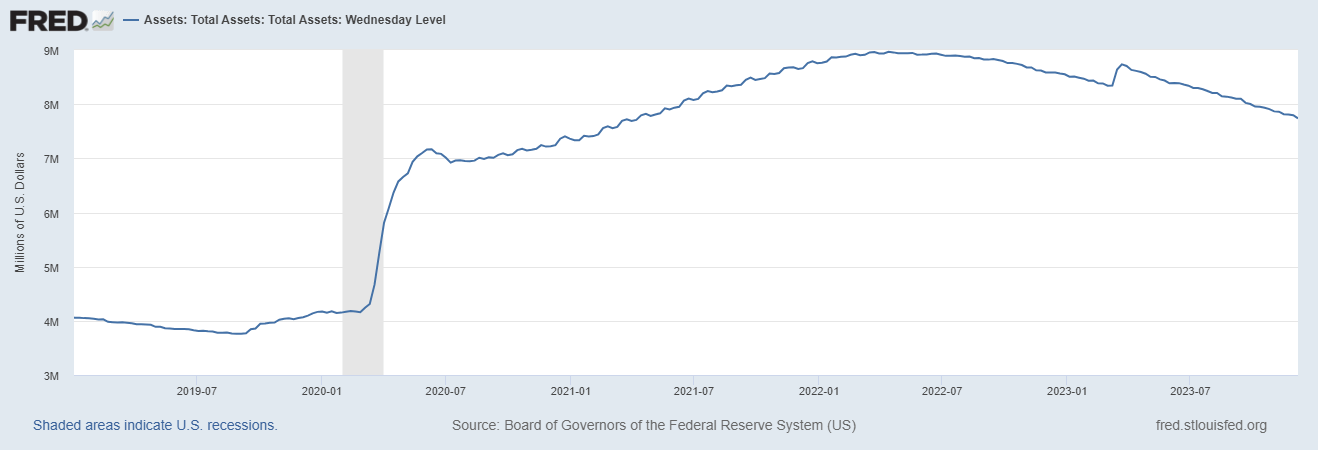

The Fed has removed a modest amount of liquidity from the economy during 2023. The Fed’s balance sheet began the calendar year at $8.51 Trillion and stands at $7.74 Trillion today, a 9% reduction.

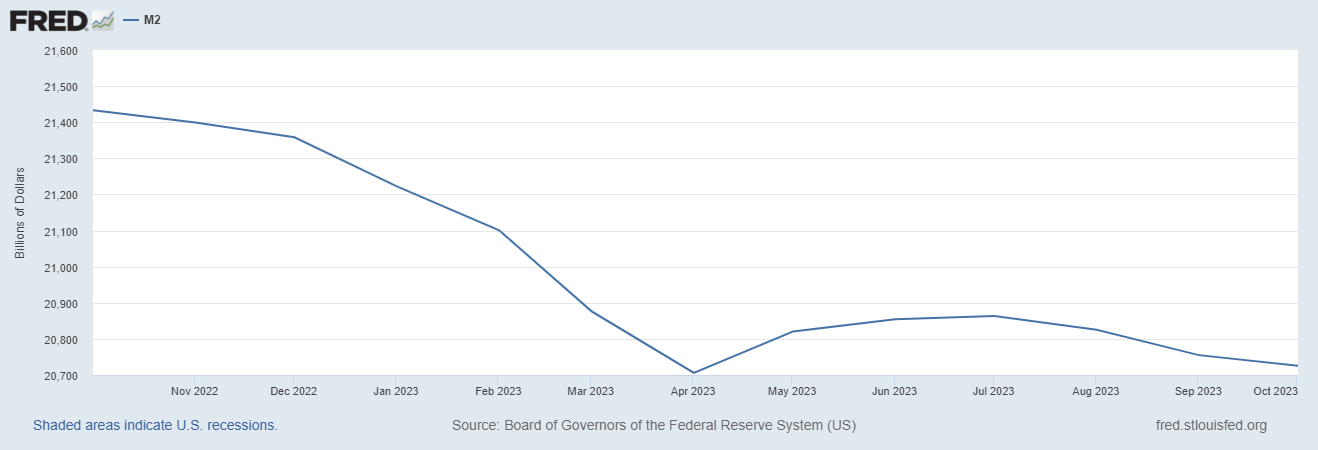

Meanwhile, the money supply as measured by M2 has shrunk by 2.4% from January 2023 through today.

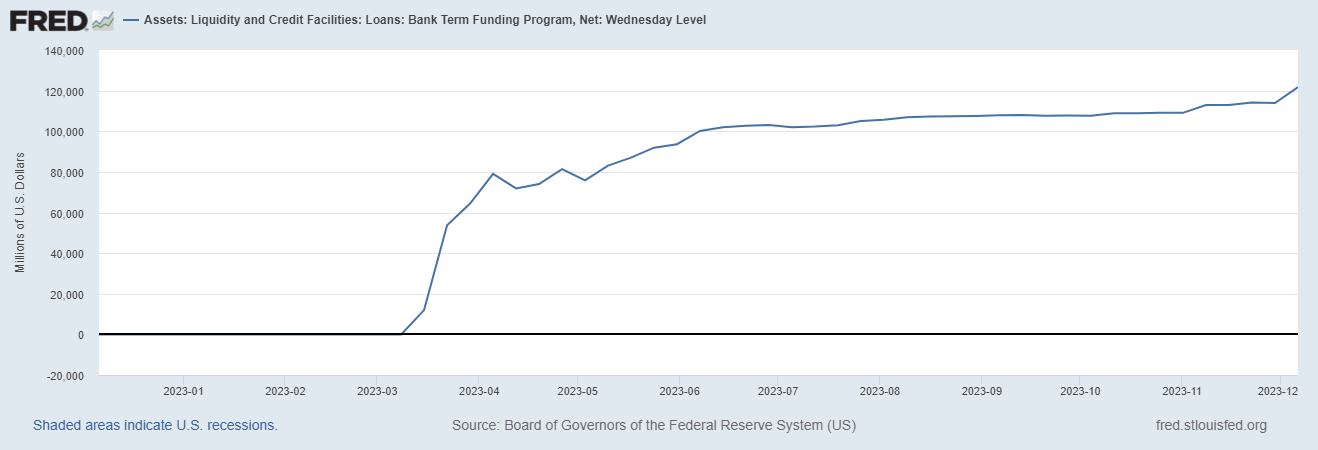

The Fed has also run a backdoor QE program this year with its Bank Term Funding Program (BTFP), a bank bailout at scale that we believe will be renewed in March 2024.

Thus, while the Fed has only slowed the rate of growth in price increases as measured by CPI, it may have done enough to tip the U.S. economy into an official recession early next year which may bring much needed deflation to the economy.

The Fed had a recession on its hands in March 2023, it just simply was not the style of recession that the Fed was looking for. Therefore the Fed decided to put the recession off by bailing out all of America’s banks and all bank depositors.

Believe it or not, there was a time (pre-2009) when the largest player in the Capital Markets was not the Federal Reserve. Pre-2009 was a time when the Fed did not prop-up every darn asset class. Investors could go long or short and the market would find a natural equilibrium. Today, the Fed is of course one of the two largest players in the equity and fixed income markets along with the fiscal side of the U.S. Government.

The best course of action for the Fed would be to maintain a 3% Fed Funds rate, halt all QE, QT and bailout programs in conjunction with massive entitlement cuts on the fiscal side of the ledger. This would enable the U.S. to run fiscal surpluses while reducing its massive debt load and simultaneously strengthening the Dollar.