The Treasury Basis Trade: Understanding A Key Market Arbitrage Strategy

(Click HERE to view the PDF version of this article).

The Treasury Basis Trade: Understanding a Key Market Arbitrage Strategy

The Treasury basis trade represents one of the most significant arbitrage strategies in fixed income markets, gaining prominence especially after the 2008 financial crisis. This strategy exploits price differences between Treasury cash bonds and their corresponding futures contracts, offering traders potential profit with theoretically minimal risk.

What is the Basis Trade?

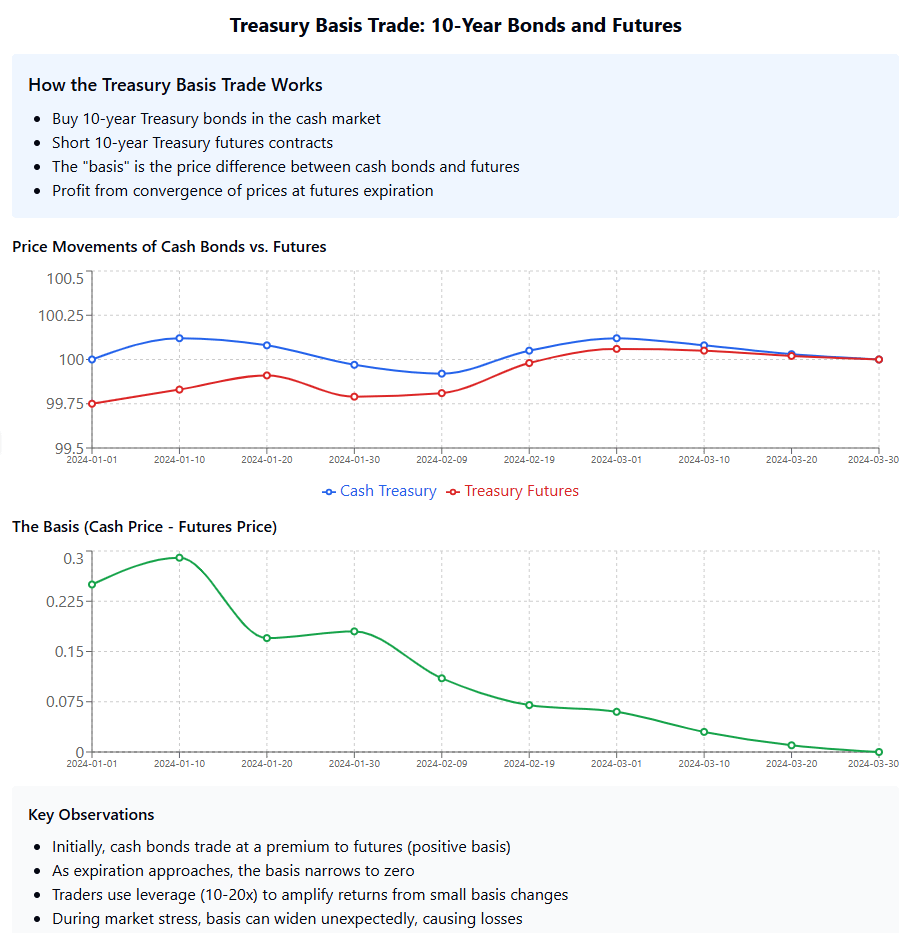

At its core, the basis trade involves simultaneously taking opposite positions in Treasury cash bonds and Treasury futures contracts. The "basis" refers to the price difference between these two related instruments. In a typical execution, traders buy Treasury bonds in the cash market while shorting Treasury futures contracts (or vice versa), aiming to profit from price convergence at the future's expiration.

The trade exploits the fact that Treasury futures contracts have a delivery option allowing sellers to deliver any bond from a basket of eligible securities. This delivery option creates pricing discrepancies that skilled traders can leverage.

Mechanics of the Trade

The basis trade typically follows this structure:

Purchase Treasury bonds in the cash market

Short Treasury futures contracts

Finance the long bond position through repurchase agreements (repos)

Hold positions until futures expiration or until the basis narrows sufficiently

The strategy's profitability depends on the relationship between:

The yield of the cash Treasury bond

The implied yield of the futures contract

The financing cost of the position (repo rate)

When executed properly, the trade captures the difference between these rates while hedging interest rate risk.

Leverage and Magnification

What makes the basis trade particularly attractive—and potentially dangerous—is the minimal margin requirements for futures positions. This allows traders to apply significant leverage, often 15x to 20x or higher. While the basis spread might be small (measured in basis points), this leverage can amplify returns substantially.

For example, a 5 basis point move might generate a 1% return on capital—unremarkable on its own. However, with 20x leverage, this translates to a 20% return, making the strategy highly appealing to hedge funds and proprietary trading desks.

Market Impact and Systemic Significance

The Treasury basis trade has grown to represent hundreds of billions, potentially trillions, of dollars in market exposure. Major participants include hedge funds, primary dealers, and proprietary trading firms. The strategy's popularity has several important market implications:

Market Efficiency: The trade helps align pricing between cash and futures markets, theoretically improving market efficiency.

Liquidity Provider: Basis traders provide significant liquidity to Treasury markets, particularly in off-the-run securities.

Systemic Risk Concerns: The high leverage involved creates potential systemic vulnerabilities. During market stress periods, these positions can amplify selling pressure if traders are forced to unwind simultaneously.

The March 2020 Disruption

The COVID-19 market panic in March 2020 provided a stark illustration of the basis trade's systemic importance. As market volatility surged, Treasury markets experienced unprecedented dysfunction. The basis between cash Treasuries and futures widened dramatically, contrary to conventional expectations that Treasuries would serve as a safe haven.

This dislocation forced many basis traders to unwind positions simultaneously, contributing to a liquidity crisis in the Treasury market. The Federal Reserve ultimately had to intervene with extraordinary measures, including massive Treasury purchases and the establishment of a special repo facility.

Regulatory Considerations

The basis trade exists in a regulatory gray area. While individual positions may comply with risk management guidelines, the aggregate market exposure creates potential vulnerabilities that transcend individual firms.

Regulators have grown increasingly concerned about several aspects:

Leverage and Counterparty Risk: The high leverage inherent in the trade creates significant counterparty exposure.

Market Integrity: Basis trading affects price discovery in Treasury markets, which form the foundation of the global financial system.

Liquidity Risks: The strategy's prevalence means market stress can trigger correlated position unwinds, exacerbating liquidity problems.

Future Outlook

The Treasury basis trade will likely remain a core strategy for many market participants despite its risks. Several factors support its continued relevance:

Market Structure: The fundamental structure of cash and futures markets creates natural arbitrage opportunities.

Balance Sheet Efficiency: Basis trades offer efficient use of balance sheet for banks and financial institutions.

Search for Yield: In low-yield environments, the enhanced returns from leveraged basis trades remain attractive.

However, potential regulatory changes could impact the strategy's profitability. These might include modified leverage requirements, increased transparency, or changes to the futures delivery mechanism.

Conclusion

The Treasury basis trade exemplifies the sophisticated arbitrage strategies that define modern financial markets. While theoretically a low-risk proposition, its widespread adoption and inherent leverage transform it into a strategy with systemic implications. Understanding this trade provides insight into market functioning, liquidity dynamics, and the interconnections between different segments of the fixed income universe.

As markets continue to evolve, the Treasury basis trade will remain an important barometer of market health and a significant contributor to Treasury market liquidity and efficiency—albeit one that requires careful monitoring by both participants and regulators.