The Treasury Market Will Ultimately Force Fiscal Discipline on Washington

When the Fed decided to pursue Quantitative Easing (QE) and Zero Interest Rate Policy (ZIRP) back in 2009, perhaps it did not realize that it would unleash enormous fiscal deficit spending and an unholy appetite for debt. It has proven next to impossible for the Fed to extract itself from the QE/ZIRP paradigm, notwithstanding this current modest tightening period. Yet, unsustainable fiscal spending levels remain and will eventually cause the Fed to lower interest rates as the $35 Trillion Treasury debt mountain grows. Ultimately, the long-end of the Treasury yield curve will force fiscal austerity on Washington. Politicians will not have a say in the matter.

Make no mistake, the Fed is still operating under the QE/ZIRP policy umbrella.

The Fed’s rate hikes of 2022 and 2023 combined with QT-Lite are simply a reprieve from QE/ZIRP.

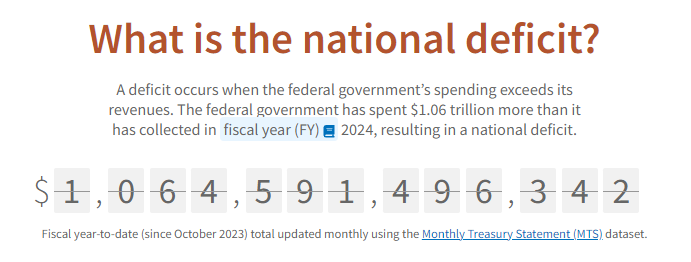

The Fed has no choice but to go back to ZIRP given the mountain of Treasury debt outstanding ($34.6 Trillion), the fact that Washington continues to spend at an unsustainable level ($1.1 Trillion deficit fiscal year-to-date), and the fact that banks are suffering (it is difficult to operate a bank when short-term rates are higher than long-term rates).

The Fed will eventually reinflate the U.S. economy this year or next and asset prices will be off to the races again once that happens.

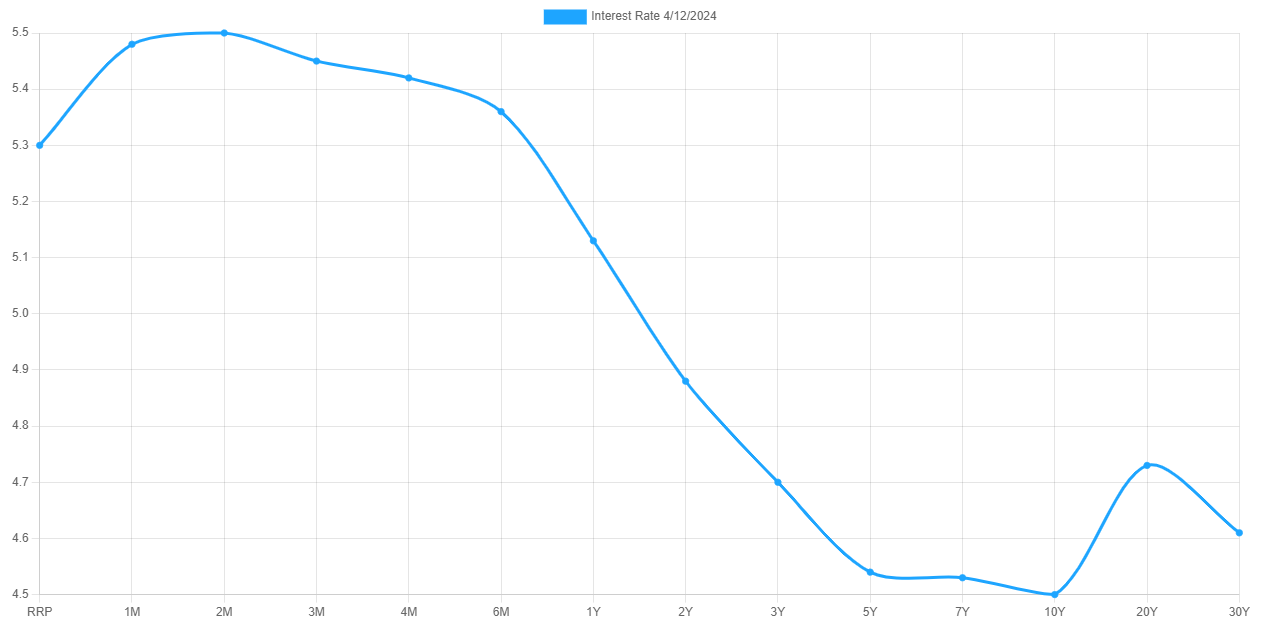

However, fixed income investors are not going to happily play at the long-end of the Treasury yield curve during an inflationary environment that regularly runs $2-4 Trillion annual fiscal deficits with Treasury yields at the long-end between 4-5%. Investors will demand higher yields.

The current fiscal spending trajectory is unsustainable, and that fact will eventually be reflected at the long-end of the Treasury yield curve. Once that happens, Washington D.C. will have no choice but to exercise fiscal discipline.

This crop of know nothing politicians has managed to put the United States in its weakest financial position in American history. The Bush, Obama, Trump and Biden Administrations and associated members of Congress have all failed to exercise fiscal discipline. The longer the U.S. waits to take its fiscal medicine, the greater the pain (fiscal austerity) will be. The U.S. will not have the option to print its way out of the ditch.