The United States’ Spend, Print, Inflate Fiscal Policy Is Unsustainable. The Fed’s Monetary Policy Isn’t Helping.

The final numbers are in. The Federal Government posted a fiscal deficit of $1.7 trillion in fiscal year 2023 on $6.1 trillion in fiscal spending. The fiscal deficit figure is up 23% from fiscal 2022’s deficit. Blame the Biden Administration and Congress for the deficits in fiscal years 2021-2023. Blame the Fed for subsidizing those deficits. The Federal Reserve really is the lap dog to the U.S. Treasury. Treasury is a fiscal debt ($33.7 trillion and counting, not including unfunded liabilities such as Social Security), generating machine with an unbridled spending appetite.

Biden knows his spend-heavy fiscal policies are wrong-headed (or does he?) Congress knows the same to be true but does not care. For at the end of the day, Presidents and Congressional members get re-elected by spending money that the U.S. does not have to spend – primarily spending money on welfare programs.

It would make more sense for the Federal Government to allow Americans to keep all of the money they earn rather than collecting various income taxes only to return a portion of it to Americans over time.

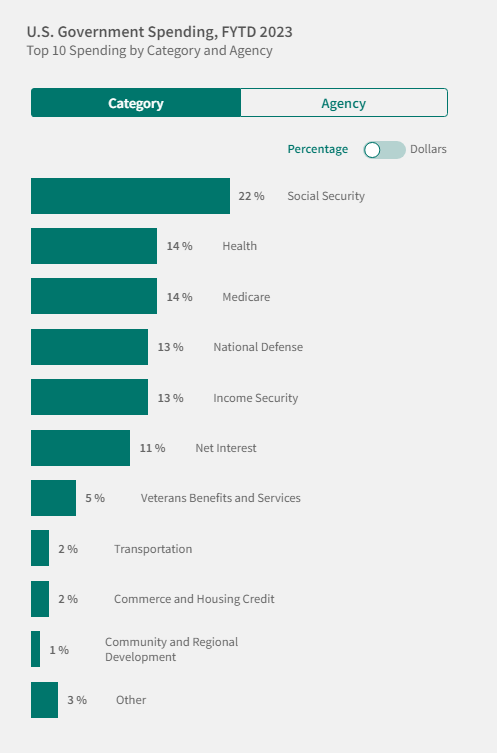

Look at the figures below:

22% of Federal Spending goes to Social Security;

14% to Government subsidized Healthcare;

14% to Medicare;

13% to “Income Security”;

The above items total 63% of Federal Spending. That’s $3.8 trillion that is allocated to various welfare programs. The Government only took in $4.4 trillion in tax revenue in fiscal 2023. When you factor in $670 billion in Interest Expense on the fiscal debt, that exceeds the $4.4 trillion in Government tax revenue by approximately $100 billion. Next year that Interest Expense figure will be approximately $1 trillion. Good luck to balancing the budget when the Interest Expense alone is $1 trillion. That’s why the Fed will ultimately be forced to lower rates – the Interest Expense is crowding out Government spending and Washington’s political class won’t allow that to happen. These fiscal spending levels and the nature of what taxpayer Dollars are spent on is unsustainable.

Ever wonder why the average price of a new car is at a nosebleed sticker price of $49K?

Curious as to why housing prices are so steep?

Why equities are overvalued?

Why most every asset is overvalued, not to mention the price of everyday goods such as food and gasoline?

The reason the price for goods and services is inflated is because of self-serving fiscal spending policies that screw the American people to the benefit of elected officials. The more the United States spends money that it does not have, the more it is forced to issue debt to cover fiscal deficits. The problem is that there are not enough buyers of fiscal debt (i.e. Treasury securities). Therefore, the Federal Reserve must step in and suck up the excess Treasury supply. To do so, the Fed must print new money. By definition, printing new money devalues the money already in circulation by way of increasing the money supply (money is a commodity like any other). Thus, Americans are hit with an “inflation tax”, a tax we did not vote for.

This devilish game will continue in fiscal 2024 (we are in fiscal 2024 now). Treasury is issuing debt to cover the deficit, much of it will be purchased by the Fed, thus money printing / Dollar devaluation will occur. Treasury yields will climb as Treasury supply increases and as the United States’ fiscal position deteriorates.

Add to the mix the forthcoming omnibus bill (likely in December). This fiscal spending bill is going to be a whopper. My guess is that the United States will run a fiscal 2024 deficit north of $2 trillion, further deteriorating the United States’ fiscal position.

If the Fed eases monetary policy as CPI continues to climb higher, long yields will get away from the Fed. Under that scenario, the Fed will intervene with QE at the long-end of the yield curve, which will create a new inflation cycle. That will be great for stocks, but extremely bad for the real economy and unsustainable over the intermediate to long-term.