This Fed Is Rudderless

The economy is softening as food and energy prices are up while the Fed is expanding the money supply

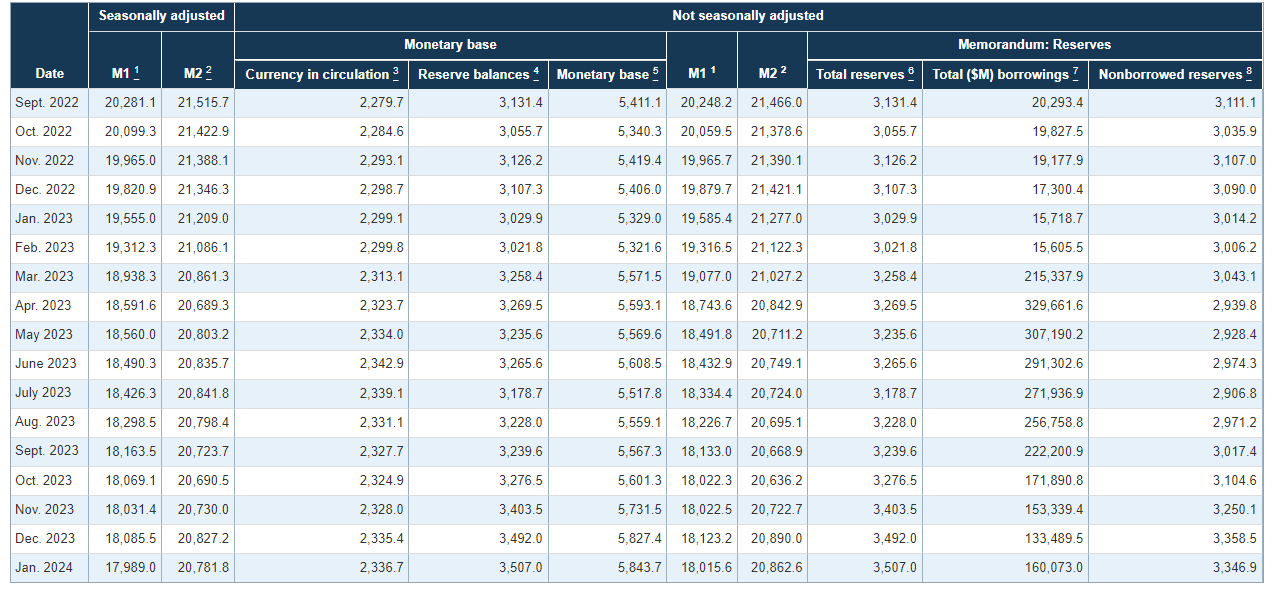

Money supply data is out. January M1 and M2 levels were flattish with December. I would prefer that the Fed exercise monetary policy exclusively by flexing the money supply. Allow the market and only the market to set interest rates.

The money supply will grow this year as the Fed Funds rate comes down and as Treasury issues new debt, much of which will be purchased by the Fed, thereby increasing the money supply. The money supply is up from October levels.

The recurring question is “when will the recession hit?” Recall that the economic hard landing was here in March of 2023 when banks ran the discount window outstanding balance to $152 billion. Banks were pulling back on credit until the Fed and FDIC swooped in with the BTFP bailout. The BTFP expires on March 11th, and it will be key to observe bank behavior in the weeks following March 11th for clues as to when they may pullback on credit.

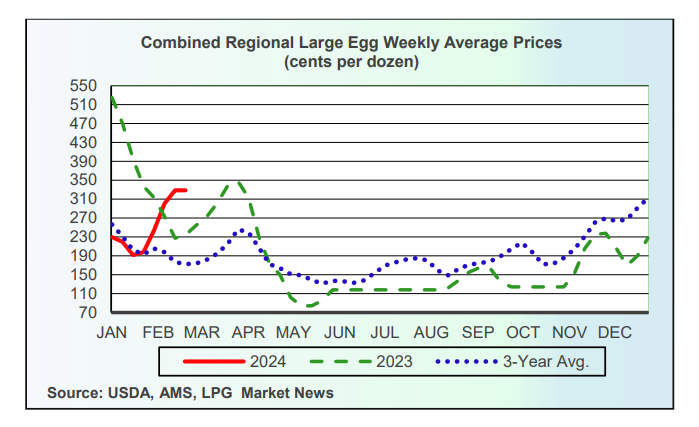

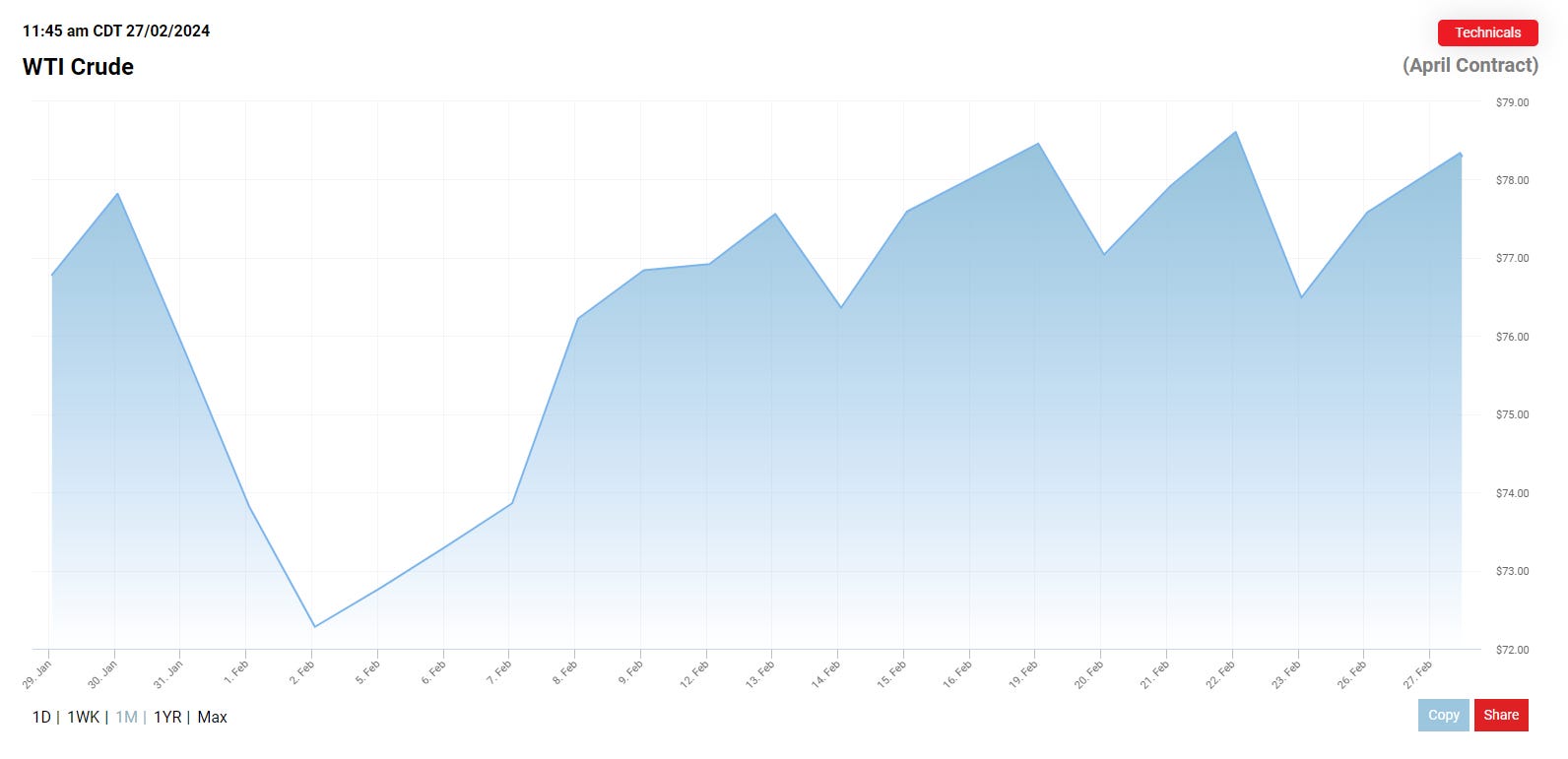

I know the Fed has its preferred economic indicators, but Food and Energy are the two expense categories that have the greatest impact on the most American households. Those costs continue to increase sequentially and do so at a greater rate than what the BEA prints in its heavily-massaged CPI figure (not only is there an incentive to keep CPI down so that price inflation does not look so bad, but there are $ Trillions in entitlements - including social security payments - that are indexed to CPI, all the more reason to manipulate the number to the low end).

If we don’t have another banking crisis by June/July as yields continue to rise, and if the Fed maintains elevated rates, then the economy will continue to grind slower, bankruptcies will remain elevated, and the consumer will go deeper into debt - although there is no guarantee that food and energy price increases will abate.