This May Have Spooked The Fed. Rate Cuts In Early 2024.

Just a couple of weeks ago Fed Chair Jerome Powell said “we are not even thinking about lowering rates”. A week later Powell and the FOMC told the world not only had the Fed thought about lowering rates, but that the FOMC consensus was three rate cuts for 2024. What could have changed Powell’s tune? Further, we believe the Fed will lower rates in early 2024 (around the end of Q1/early Q2).

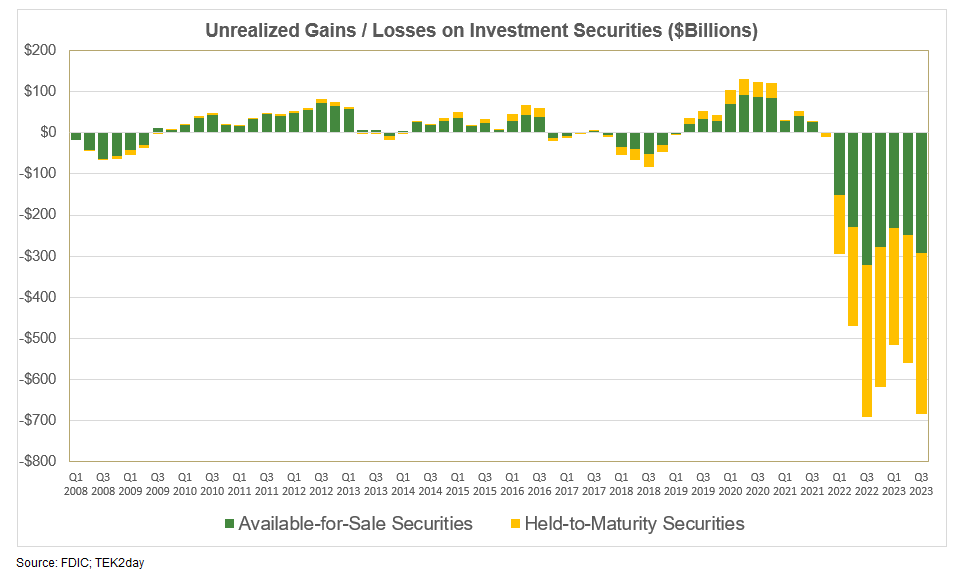

Back on December 2nd we wrote about the fact that the Bank Term Funding Program (BTFP) was here to stay given that FDIC-insured commercial banks in total carried $684 billion in unrealized losses as of the end of Q3 (see chart below).

Bank of America alone had $132 billion in unrealized losses as of the end of Q3 (Perhaps Bank of America CEO Brian Moynihan lobbed a call into Powell? Technically, U.S. banks that are members of the Federal Reserve system own the Fed).

Unrealized losses are not a problem for banks until such time as a particular bank needs liquidity. Then, said bank may be forced to sell securities in order to generate the needed liquidity. At that time the bank would record any losses on the securities sold. Further, as the economy slows, the probability that banks will need to generate liquidity grows. Large unrealized losses are likely to cause banks to pull pack on credit, which only exacerbates the problem during slow economic periods. Bank of America is more levered to the consumer than its other three large peers - J.P Morgan Chase; Wells Fargo and Citi.

My theory is that the Fed sees banks’ unrealized losses as a ticking time bomb and rather than allow banks to potentially fail, the Fed has decided to lower rates, which will reinflate bond values and enable the banks to shrink the $684 billion in unrealized losses on their bond portfolios.

How did the banks get into this mess? When Treasury and the Fed were stimulating the economy and banks were flush with cash, many banks decided to gorge on low rate debt rather than save cash for a rainy day. As rates rose, debt values naturally plummeted given the inherent inverse relationship between bond values and bond yields. Rather than allow those greedy banks to suffer the consequences, the Fed believes it is supposed to bailout those troubled banks with taxpayer Dollars. Thus, the BTFP was born in March 2023.

This rate cut is not due to the Fed having vanquished inflation, but rather a result of wanting to protect the banks and number two, reduce the interest expense on the ballooning $34 Trillion debt load. Given the size of the debt load the Fed was always going to lower rates in 2024 no matter where CPI sat. However, the precarious position the banks find themselves in will probably cause the Fed to lower rates in 1H 2024 rather than 2H 2024.