Treasury Market Is Wrong About Future Treasury Secretary Scott Bessent's Ability To Mitigate Fiscal Spending

Scott Bessent worked with Stanley Druckenmiller at Soros Fund Management in the 1990s. Druckenmiller has correctly preached for over a decade that in order to get fiscal spending under control, entitlement spending must be restructured (i.e., Social Security, Medicare and Medicaid, Obamacare, Income Assistance, etc.). That’s not happening under Trump.

Entitlement restructuring won’t happen until the people demand fiscal austerity because they can no longer bear the cost of inflation. If Druckenmiller believed that Trump was open to entitlement restructuring, he would be Treasury Secretary. Bessent may try to reduce spending to a degree, but entitlement restructuring is not on the table.

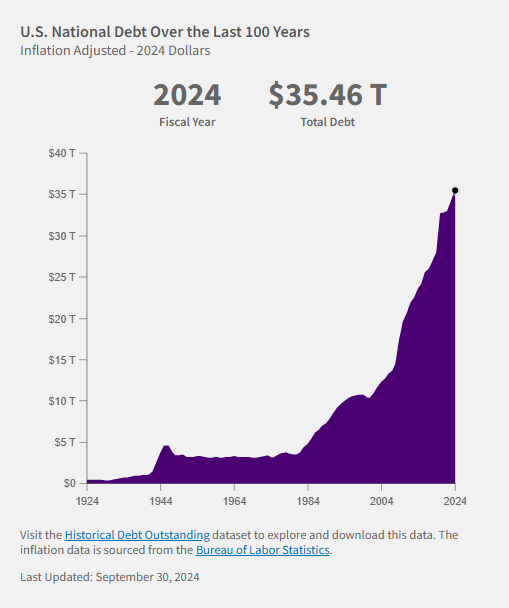

Best case scenario is that Elon Musk and Vivek Ramaswamy knock $1 trillion or so from the fiscal budget via executive order. While that is happening, Trump will pressure Powell to reduce the Fed Funds rate and thereby reduce the cost of short-term debt. However, a reduction in interest expense via rate reduction is not the same thing as reducing the debt load (currently at $36 trillion). Cutting rates - i.e., easing monetary policy - will only further inflate the “everything bubble”. Kicking the can down the road will only make the fiscal debt and weak Dollar / inflation problem worse.

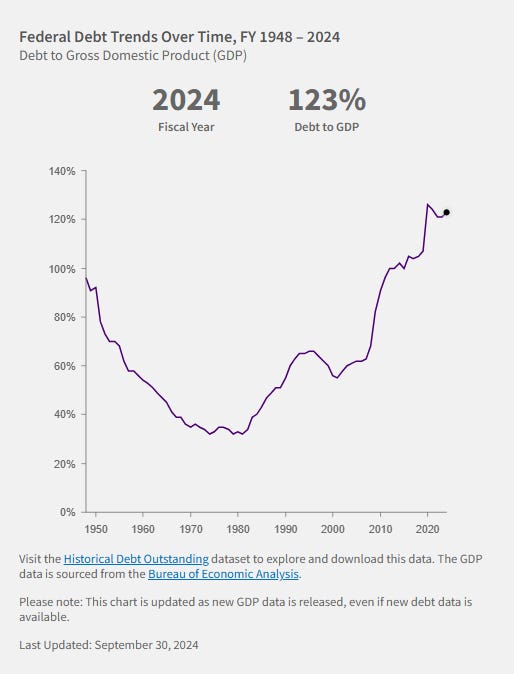

For the next decade or so, I expect flat Real GDP given the elevated price environment combined with the U.S.’s massive debt load. Perhaps equities will melt up further, who knows? One thing is for sure is that the fiscal debt grows everyday, thereby weakening the Dollar and the U.S. economy. At some point we will have to deal with fiscal austerity, or it will be forced upon us by the Treasury market when Treasury investors realize the U.S. debt problem is only getting worse. It is better to deal with debt proactively.