Weekly Update: Bank Term Funding Program

Before we get to this week’s BTFP activity, when investors ask “When will we see a recession?”, recall that back in March we were days away from a number of bank failures which surely would have caused those banks left standing to dramatically tighten access to credit. Rather than allow those mismanaged banks to fail, the Fed and the FDIC stepped in with the BTFP – which is a massive bailout that insured all deposits system-wide and allowed all banks to sell their bond holdings to the Fed at par value. It’s awful policy to bailout poorly managed firms rather than allow them to suffer the consequences. These days every darn company is “too big to fail”. This Nanny State-styled policy has bred moral hazard at scale to where bailouts are the norm versus extraordinary. “Don’t worry, the Fed will rescue the market with low rates and QE” seems to be investors’ battle cry. However, there is no free lunch. Every monetary and fiscal bailout comes with a cost. Bailouts add to the national debt and devalue the Dollar (the latter is the dreaded inflation tax). The correct approach would be to allow the market to purge itself of the past 15 years of monetary and fiscal excess, especially the tranche of excess that occurred from April 2020 to May 2022.

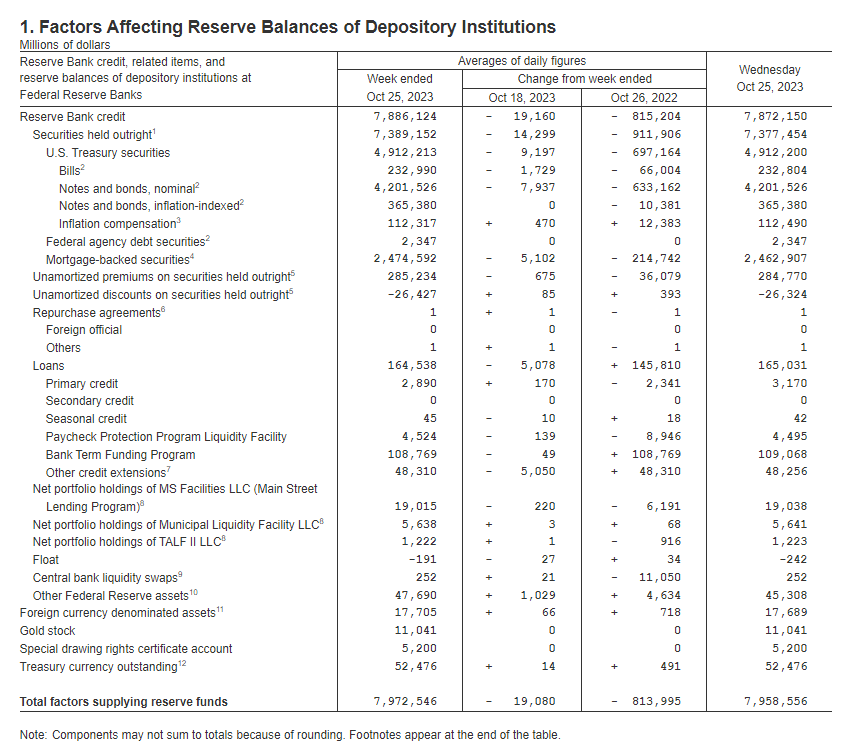

The Bank Term Funding Program (BTFP, bail out/QE) had approximately $109.1 billion in outstanding loans as of Wednesday this week, up from $108.8 billion (+ $0.3 billion) a week ago.

The “other credit extensions” line item of $48.3 billion includes the FDIC loans made to regional banks. This figure is down from $53.2 billion (- $4.9 billion) a week ago.

FEDERAL RESERVE statistical release: https://www.federalreserve.gov/releases/h41/current/