Solera: When Debt Is an Obstacle to Growth

There are lots of good people at Solera (SLRA), but the company carries 3.3x the amount of debt (and to be fair - 2x the revenue), compared to when I was with the company. The amount of debt that Solera carries will challenge growth initiatives (organic and M&A) and limit product innovation. This for a company that sells into a staid, slow growth industry.

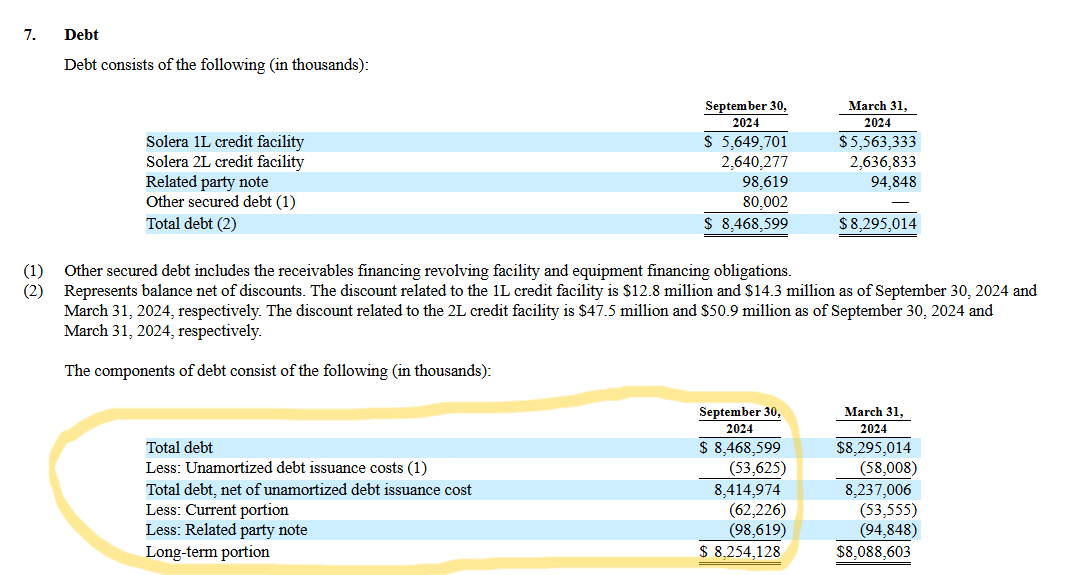

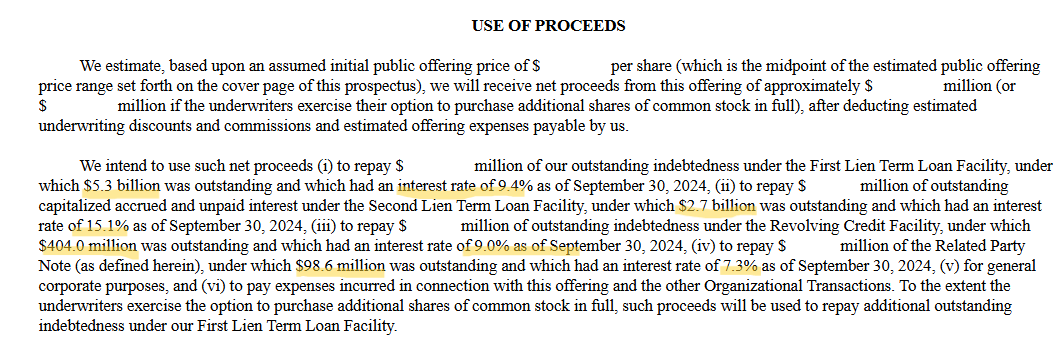

Solera not only carries a significant amount of debt, it does so at high interest rates (below).

Investors are too sanguine about the Fed lowering its Fed Funds rate. Many companies carry debt at high rates and will have to refinance at potentially higher rates, or pay down debt with cash on hand, or with cash raised from equity offerings or from asset sales.

What the Fed has done in its last two meetings (lowering Fed Funds by a combined 75 BPS) is inconsequential to many companies, especially as long rates move higher (The 10-year Treasury yield is at 4.43%, which does not bode well for corporate issuers).

My recent thoughts on CCCS (HERE).