Why The U.S. Economy Has Slowed at A Glacial Pace

There is logic behind why the U.S. economy has slowed at a glacial pace.

First, Real GDP had to slow in percentage terms in 2022 given that 2021 was such a tough comp.

Second, the Fed in combination with the commercial banks shrunk the money supply as measured by M2 from its peak in April 2022 through October 2023. Such a decline in the money supply would normally lead to a pronounced recession. However, there were two significant economic buffers that deflected much of the economic blow.

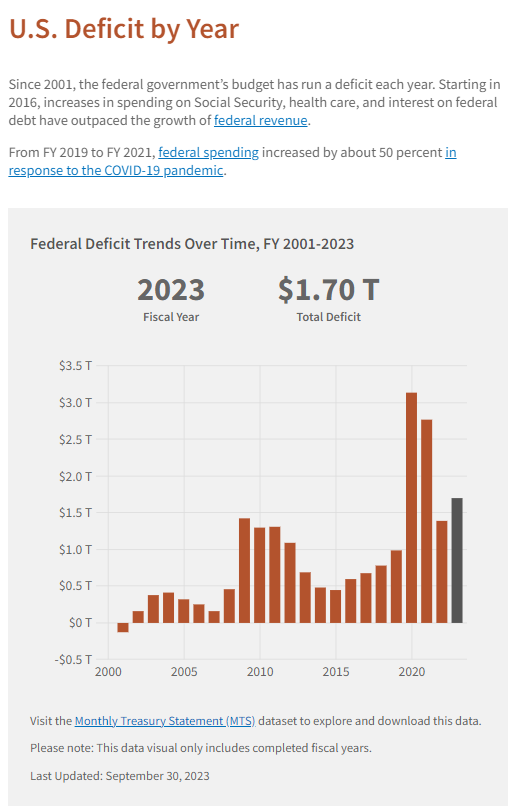

The first buffer was the large fiscal deficits the Biden Administration ran in 2022, 2023 and in fiscal 2024 (chart through FY’23 below). Fiscal 2022 and 2023 in particular benefitted from various COVID relief programs, which we have written about in the past such as the Employee Retention Credit (ERC). Fiscal 2024 should see a fiscal deficit in excess of $2 trillion and is 24% higher than 2023’s deficit year-to-date.

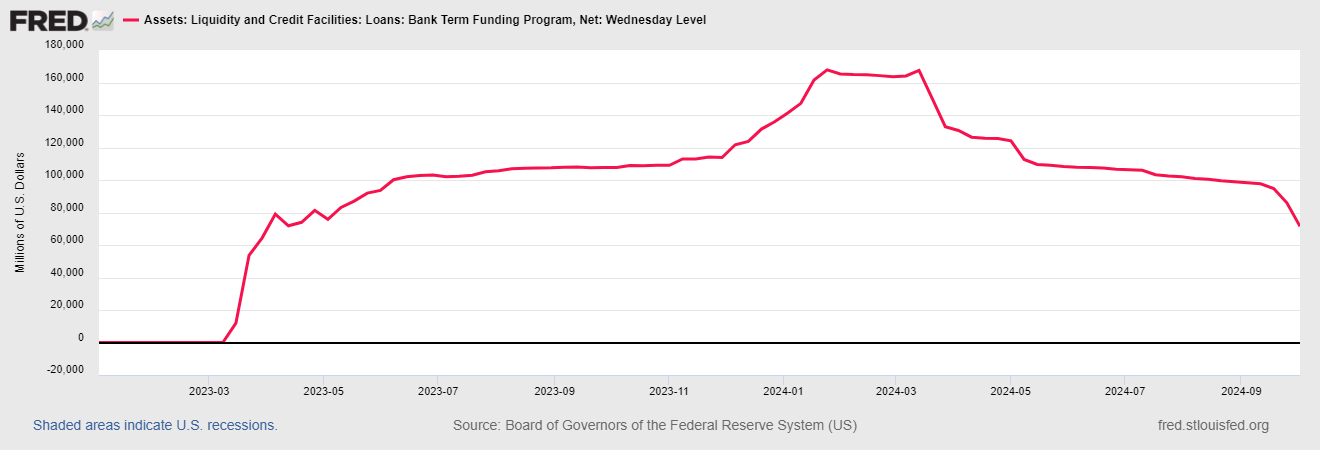

The second significant economic buffer was the Bank Term Funding Program (BTFP). The BTFP was a $200 billion (approximately) bank bailout that ran from March 2023 – March 2024. The BTFP kept the banks lending. Recall that many commercial banks, especially Bank of America (BAC), are underwater on their fixed income investment portfolios as a result of overbuying debt securities when rates were at or near zero percent, only to have interest rates move higher in 2022, 2023 and remain higher in 2024. When banks suffer large paper losses on their investment portfolios, they typically curtail lending. Given the size of the unrealized losses, it would have made sense for the banks to significantly curb lending in Q1 2023, combined with the mild panic set off by Silicon Valley Bank (SVB). As we wrote last year, I believe that Fed Chairman Jerome Powell turned dovish on December 13th 2023 because Bank of America CEO Brian Moynihan likely got in Powell’s ear and told him that higher yields were making it difficult for BAC to extend credit, despite the BTFP.

Nonetheless, the BTFP prevented banks from failing, but at great cost - moral hazard on the part of bank CEOs (and other CEOs who observed the Fed’s corporate welfare), plus the $200 billion of capital (maybe more). I would have preferred that the market run its course, even if that meant many high profile bank failures.

These two economic buffers staved off a more pronounced economic decline, but at the significant cost of prolonged price inflation and moral hazard.

Through this 2021-2024 period, prices for goods and services have continued to move higher. Higher prices are stretching the consumer. That is why the consumer savings rate has come down. That is why consumers are taking more than one job (one full-time, one part-time or multiple part-time jobs).

The U.S. economy needs to be allowed to run its course. If the Fed goes “full dove” and takes rates to zero percent and uses QE to fight higher yields at the long end of the curve, it will only exacerbate higher prices for goods and services. Further, if the fiscal side continues to run multi-trillion Dollar deficits, that behavior will only feed the inflation fire. This fiscal and monetary mess we are in is a result of Government interventionist policy. It will only get worse if fiscal and monetary policy continue to run the same playbook.