Will The Equity Market Ever Roll Over?

Will the equity market ever roll over? Technology stocks pulled back a bit last week, but when one considers the amount of liquidity that has been pumped into the U.S. Economy since 2020 - that liquidity has to go somewhere. Historically, the equity market does not roll over until after the Fed lowers rates.

If you listened to the March/April quarter earnings calls, you know that business is slowing.

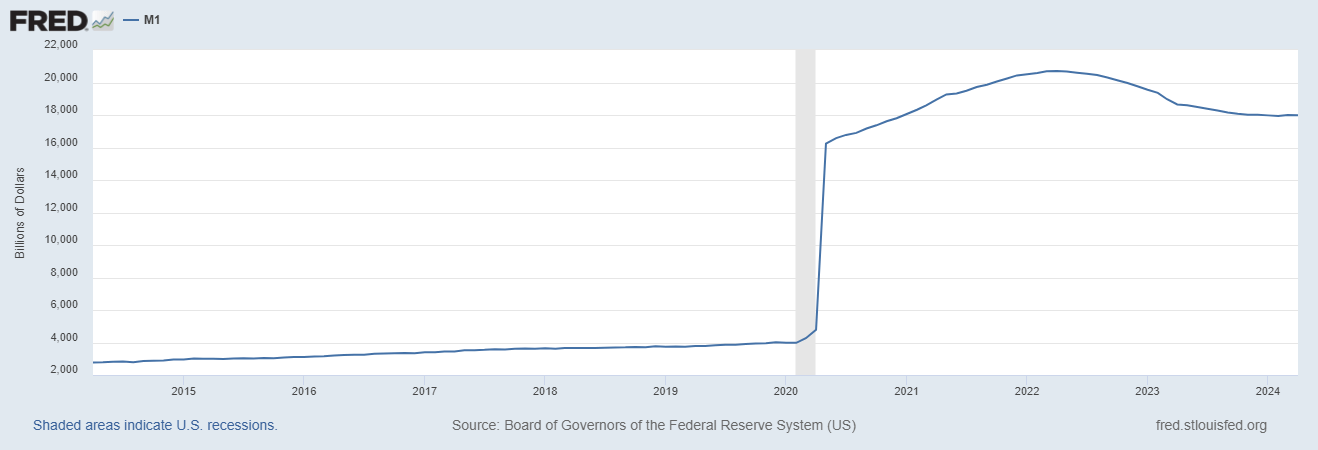

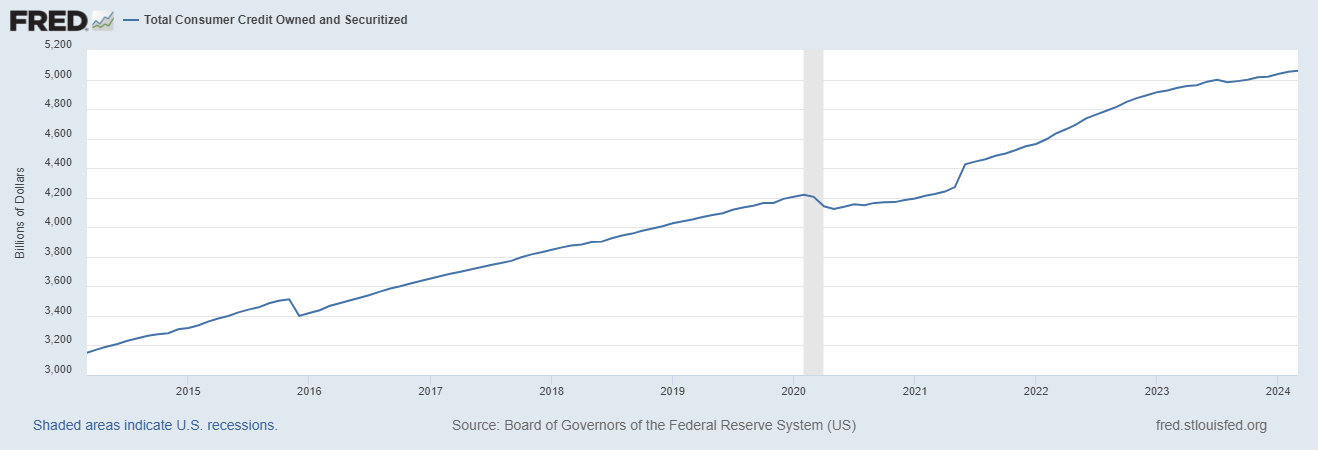

The consumer is at a breaking point and has made ends meet by increasing the use of credit. The credit game is fraying as auto repos and mortgage delinquencies increase.

See our recent note on the Consumer within the context of Bank of America’s business HERE.

Source: Federal Reserve More affluent consumers are trading down market (WMT commentary).

ABNB expects Q2 revenue growth to slow. I would guess there is a 70% probability that ABNB comes up light this summer versus revenue and bookings expectations based on what I have seen along the coast. Thus, discretionary spend is slowing.

Bankruptcies continue to increase as do business closures for companies that do not formally file for bankruptcy.

So what gives? Why hasn’t the market pulled back much - in particular the NASDAQ?

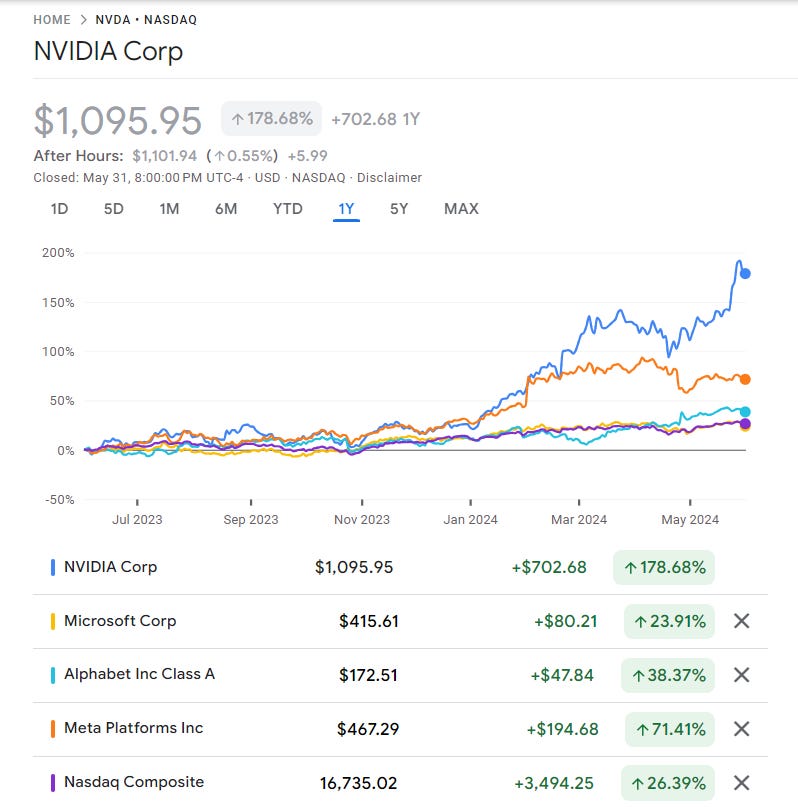

First, the largest companies continue to see their stocks move higher or remain flat. This includes NVDA, MSFT, GOOGL, META. Thus, it is difficult for an index to experience a correction when its largest components are growing in valuation.

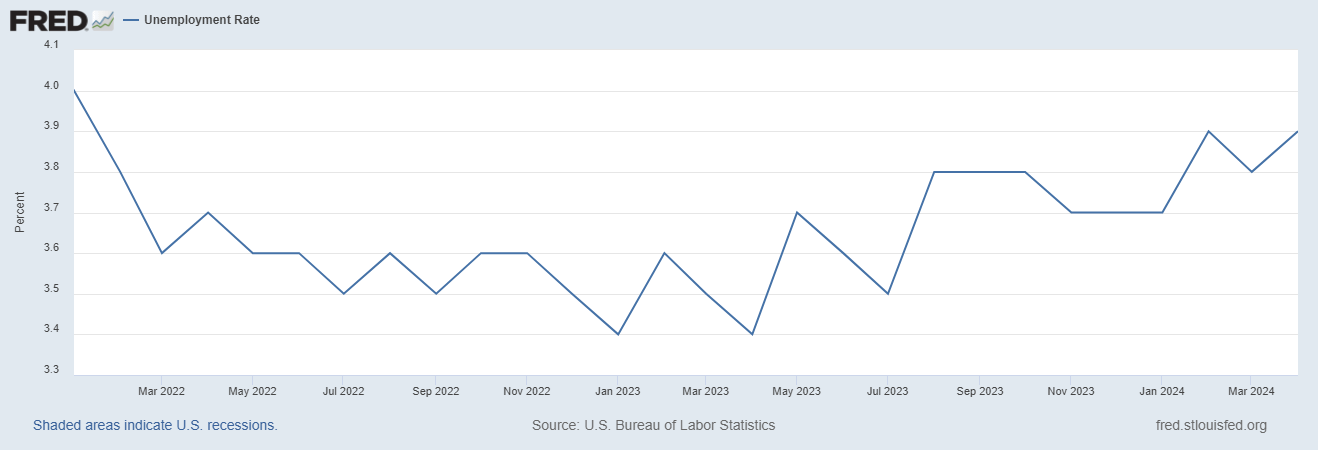

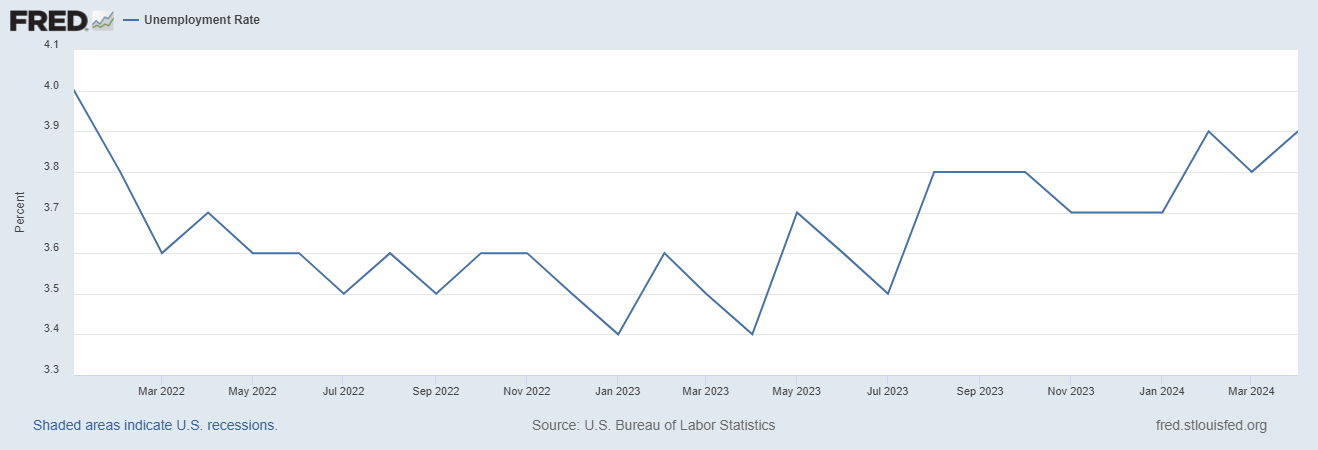

Second, unemployment has been steady. If unemployment moves into the high 4 percent range or the 5 percent range, people will start pulling capital out of the market. Until then, capital will be deployed in equities.

Side note: Venture firms have pulled back on funding and valuation multiples (other than AI company valuations) as have PE firms since interest rates started to move higher. It’s only the public markets that have defied valuation discipline as public company investors typically are the most unsophisticated investor class as it relates to assessing company-specific risk, particularly on the retail equity side.

I would expect the Fed to meaningfully lower rates should unemployment tick above 4.5%.

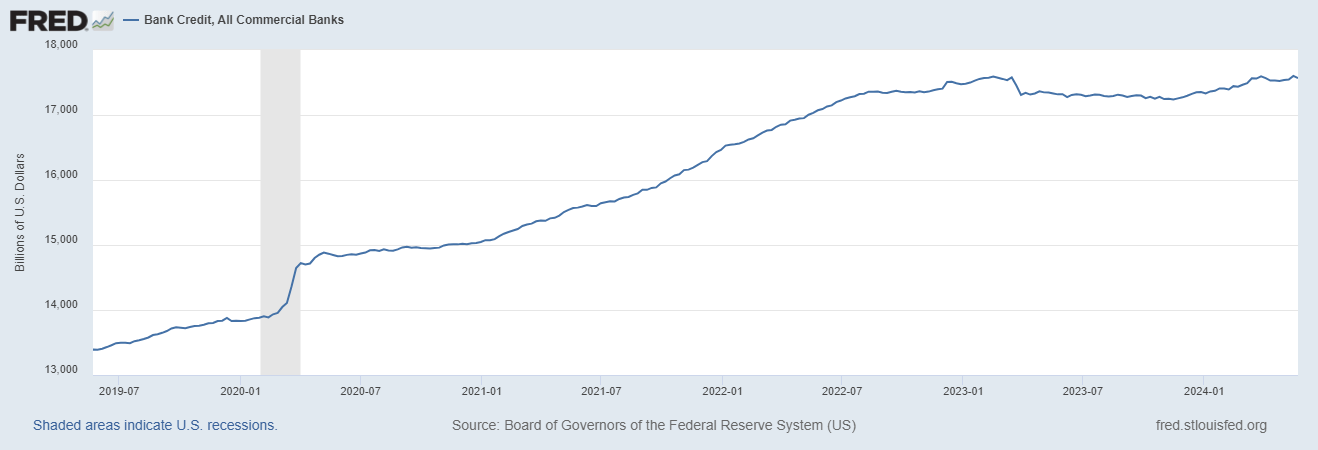

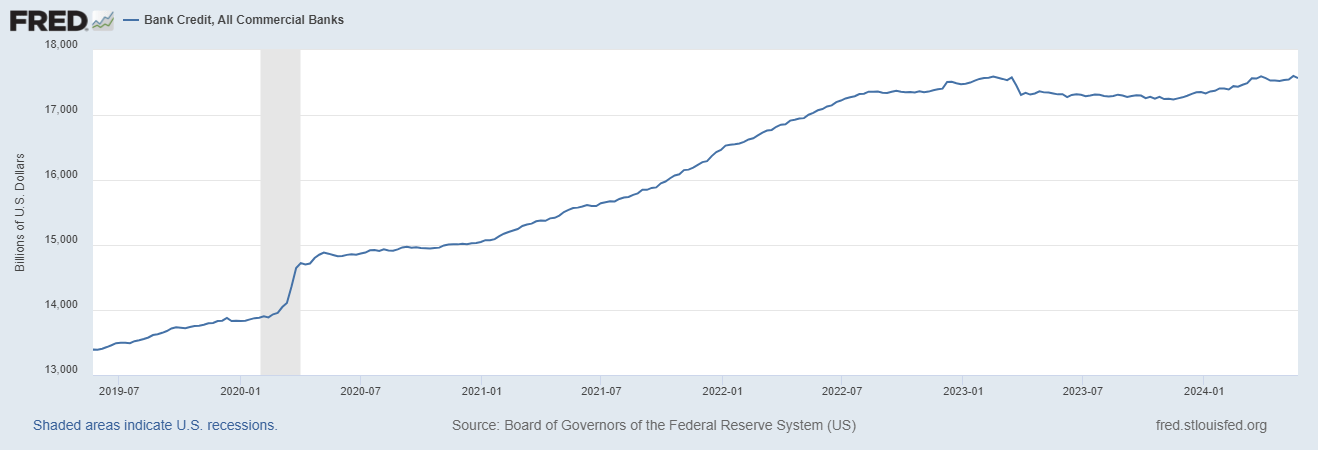

Source: Federal Reserve Third, bank credit has been fairly healthy. Banks were bailed out by the BTFP program which provided sufficient liquidity to guard against mounting unrealized losses, although that credit buffer will expire. The looming CRE defaults and refinancing wave will force some banks and non-bank FIs to fail. Should the banks pull back on credit, the U.S. will suffer a more pronounced recession and the equity markets will pull back.

In the meantime, bank credit has expanded in recent months.

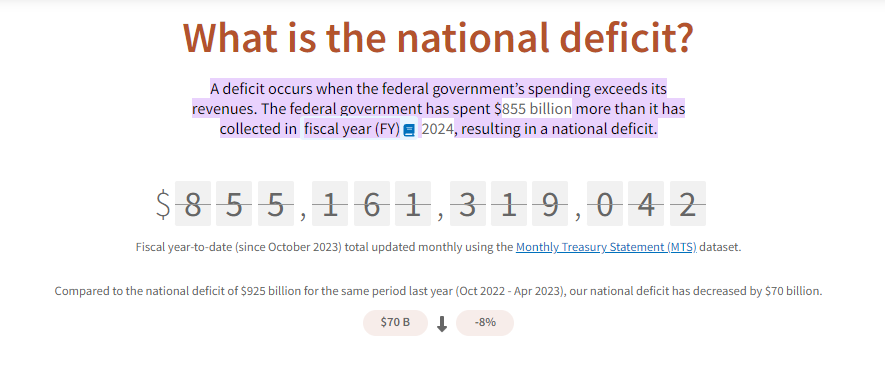

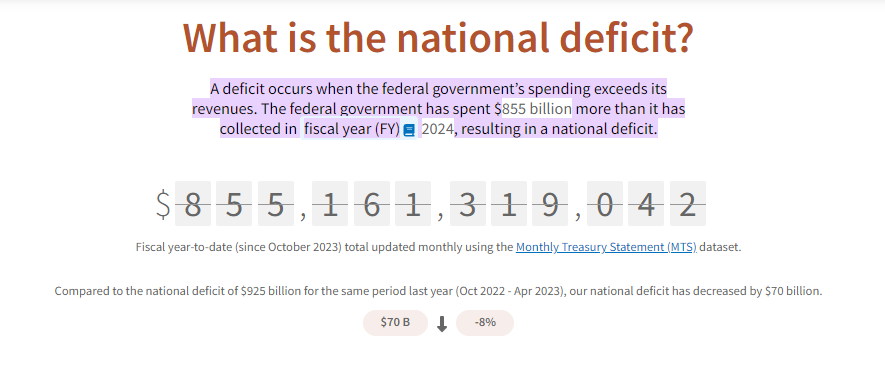

Source: Federal Reserve Finally, heavy fiscal spending artificially supports the U.S. Economy. This does not come without a price. Deficit spending increases the debt outstanding, which means a growing debt services burden (now at $1.1 Trillion). As the debt service expense grows, this will crowd out fiscal spending, which means the fiscal crutch will slowly disappear from the U.S. Economy. The fiscal deficit is $855 billion as of April 30th. The fiscal year ends on September 30th.