Yields Are Too Low

I’m looking at the High Yield Index, 10-year Treasury yields, and the spread between the two. My view is that the High Yield Index is too low, the 10-Year is too low, and the spread between the two is too low. Default risk is underappreciated at the moment.

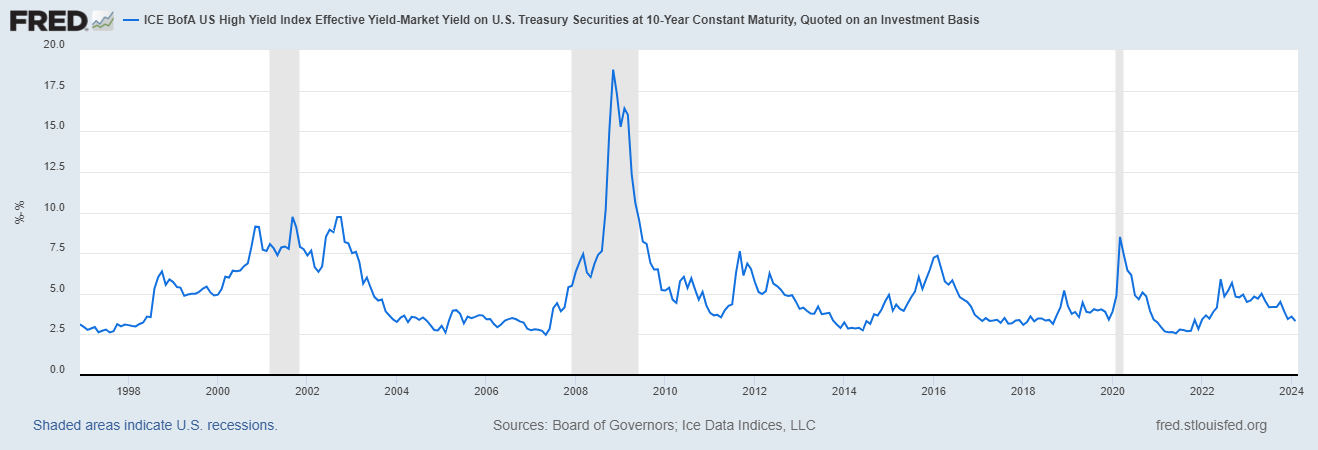

The first chart below plots the High Yield Index and the 10-year Treasury. The former is at 7.6%, the latter is at 4.3%.

Today the U.S. has record corporate defaults, yet the High Yield Index pales in comparison to 2008-2009 levels and 2001-2002 levels. Perception is reality it would seem because the current reality around corporate default risk is under the radar.

As for Treasury yields, never has the U.S. had such a Treasury debt burden ($34.3 Trillion), yet that risk seems to not be a factor in the yield equation. The U.S. is at a point where it needs to issue new debt in order to service the existing debt. That truth is not sustainable as the value of the Dollar will eventually erode to zero under such fiscal conditions. Perpetual fiscal deficit spending is why the Dollar has lost 98.5% of its value versus Gold since August 1971. If you think $5 for a dozen eggs is expensive, wait until a dozen eggs cost $15 Dollars in 7 years or $25 Dollars in 15 years should deficit spending persist.

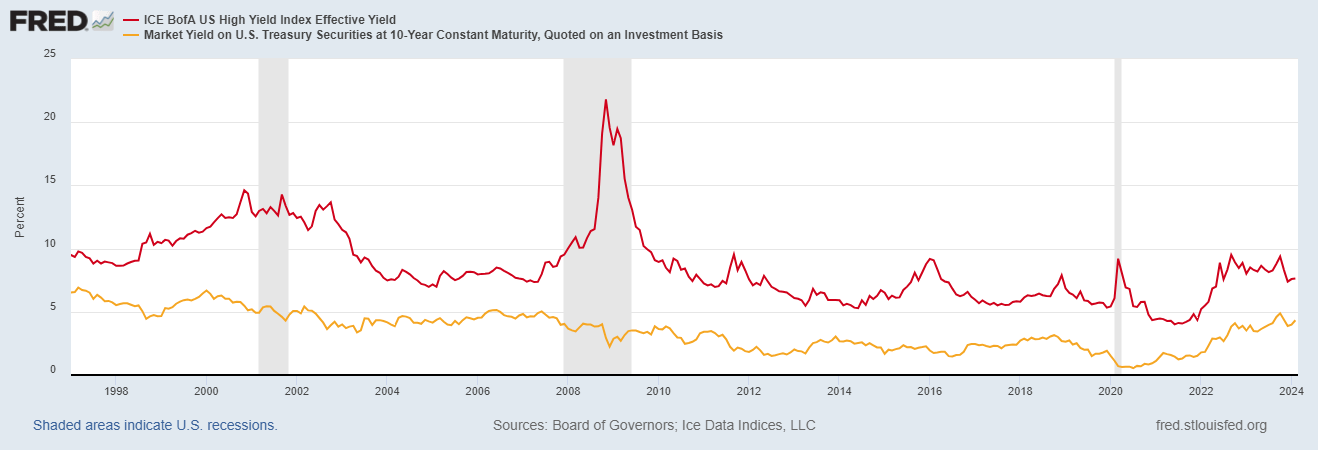

The second chart details the spread between the High Yield Index and the 10-year yield. I believe the spread should be wider as there is significant near-term corporate default risk that is not part of the default equation. For a company that has high-risk cash flows, it won’t matter if the Fed takes Fed Funds from present levels to 4%. That barely moves the needle for a High Yield credit.