Yields, Prices, Earnings and More

Yields and Prices Will March Higher

I believe the 10-year yield will push higher as real world prices remain elevated. Even when one considers the bogus Government measure of prices - CPI - the rate of change for prices accelerated in December as compared to November. This was true for Core CPI, Headline CPI as well as for Energy. I don’t see prices moving lower, at least not yet. Therefore, I expect yields to move higher.

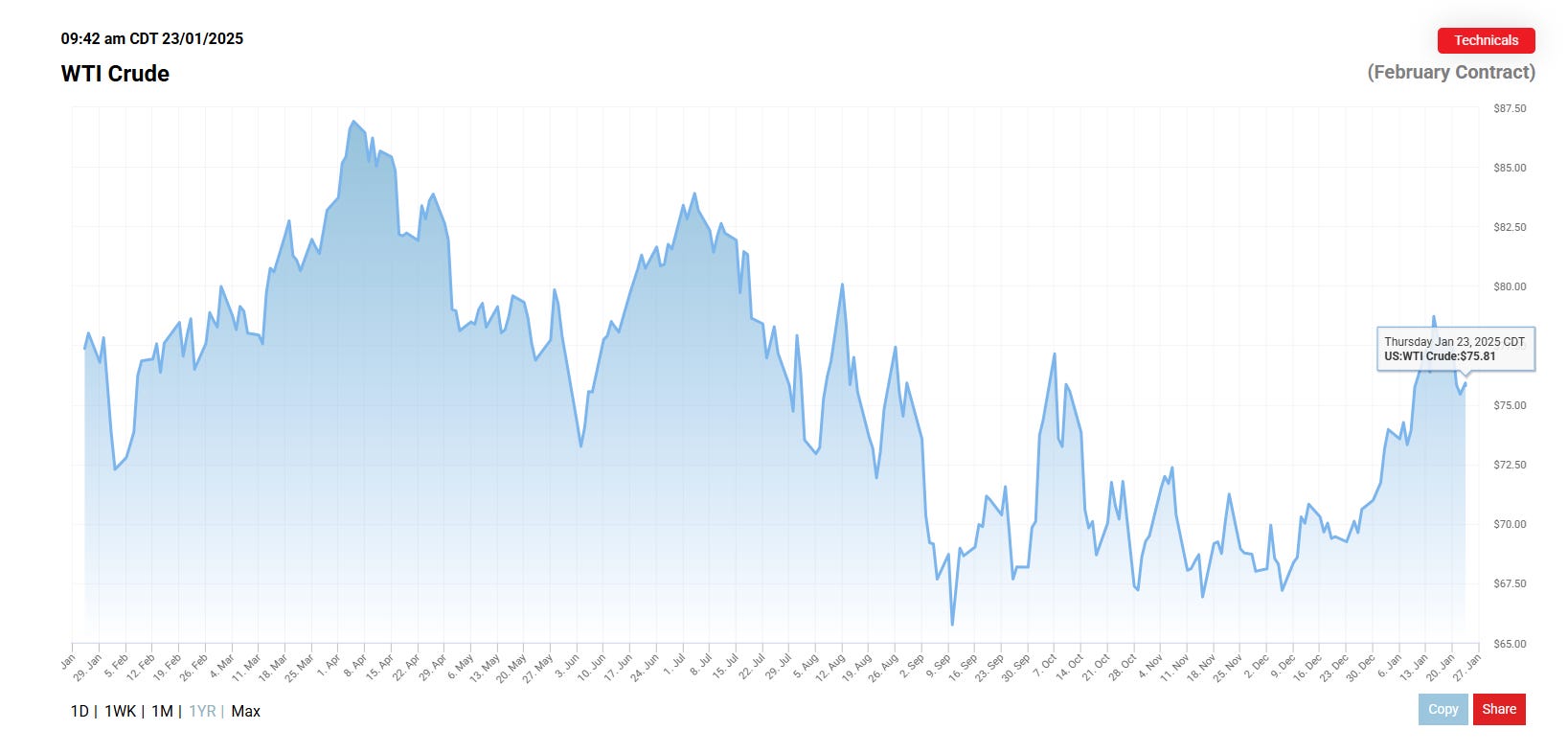

Oil prices are up over December. Speaking of Energy, oil prices remain elevated over December (chart below). Oil prices will goose Headline CPI for January. Additionally, prices for essentials such as Food and Health Services continue to march higher.

Yet, How Long Will Prices Remain Elevated?

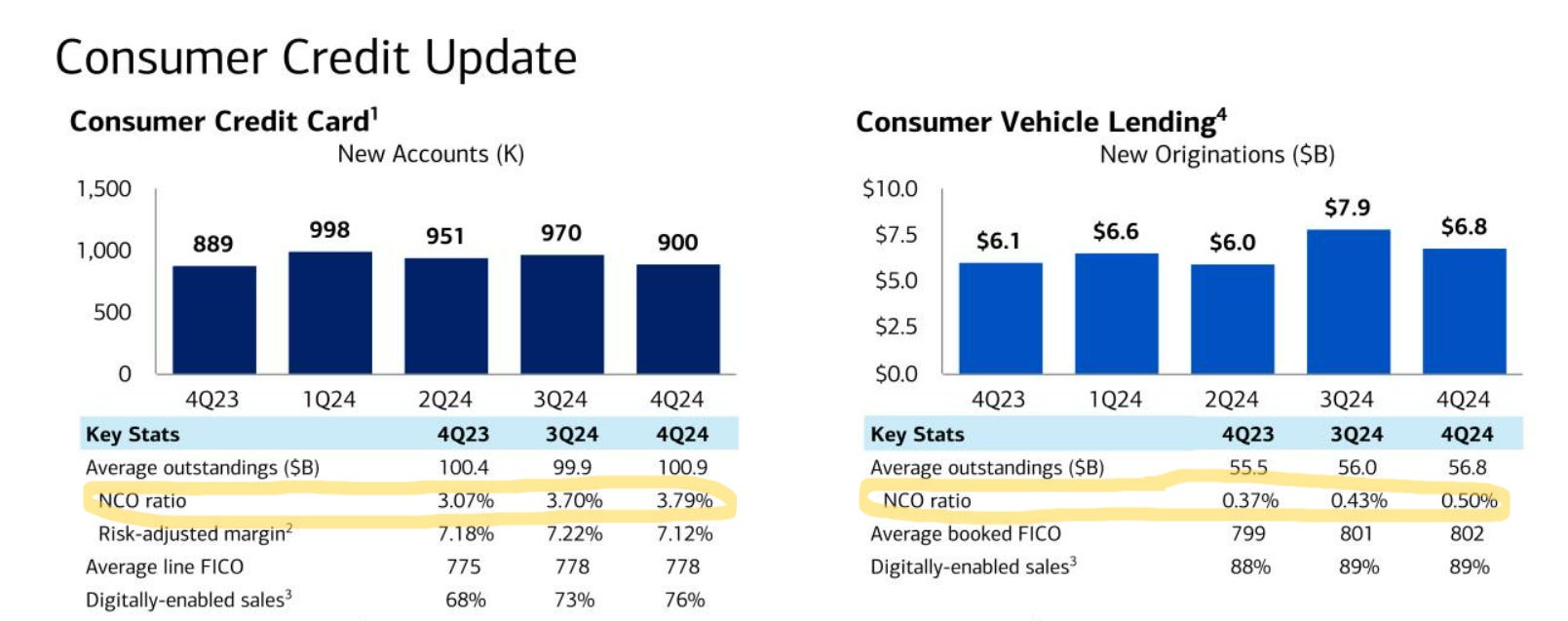

Consumer credit. When you consider consumer credit trends, they are headed in the wrong direction (see Bank of America December quarter table below). Net Charge-Off ratios for credit card and automobile lending continue to climb. The consumer is stretched.

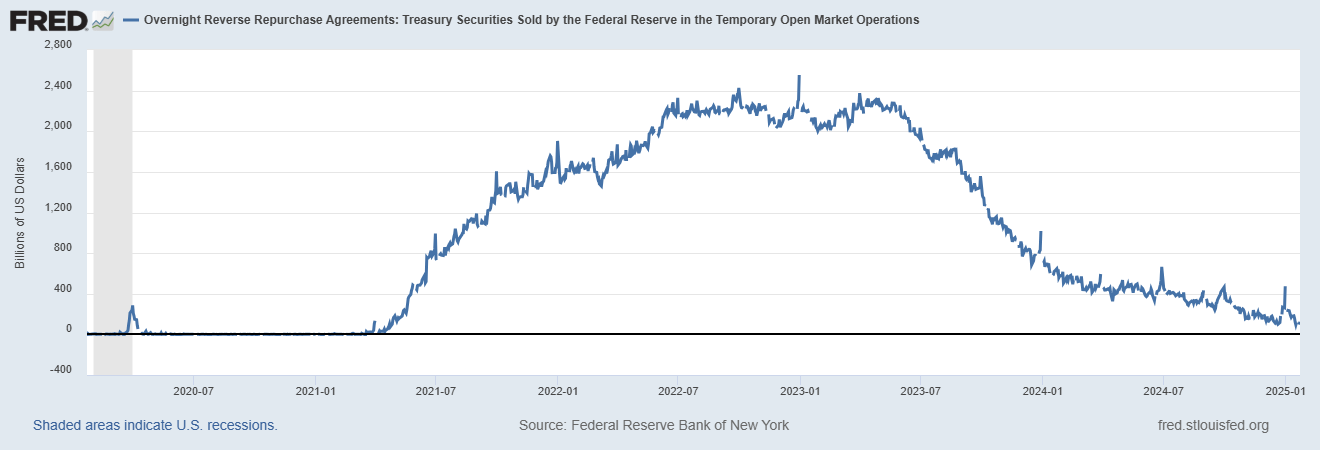

Less liquidity in the system. Most CARES Act benefits - including the Employee Retention Credit - lapsed 13-14 months ago. The BTFP bailout ended in March 2024. The Overnight Reverse Repo facility (Chart below) is winding down. The economic crutches offered by Treasury and the Fed are gone - for now.

Corporate debt maturities. These maturities will be fascinating to watch this year and next. Will companies roll debt over at higher rates, or, will they issue equity to pay down debt?

Corporate earnings. I don’t see 2025 as a great earnings year given the stretched consumer and the elevated 10-year. Headcount is flat in Software - this is not a function of AI - but rather a function of demand and higher input costs.

Leading companies continue to have pricing power. We saw Netflix (NFLX) a few days ago. Google (GOOG) has jacked prices for premium services. Microsoft (MSFT) raised 365 prices back in October. I expect conservative guidance for most Software companies on December quarter calls.